Washington Just Queued Up 702 Rules for the Chopping Block

The Spring 2026 Unified Agenda projects $1.5 trillion in FY2026 savings, and the single biggest line item is repealing the EPA's 2009 endangerment finding.

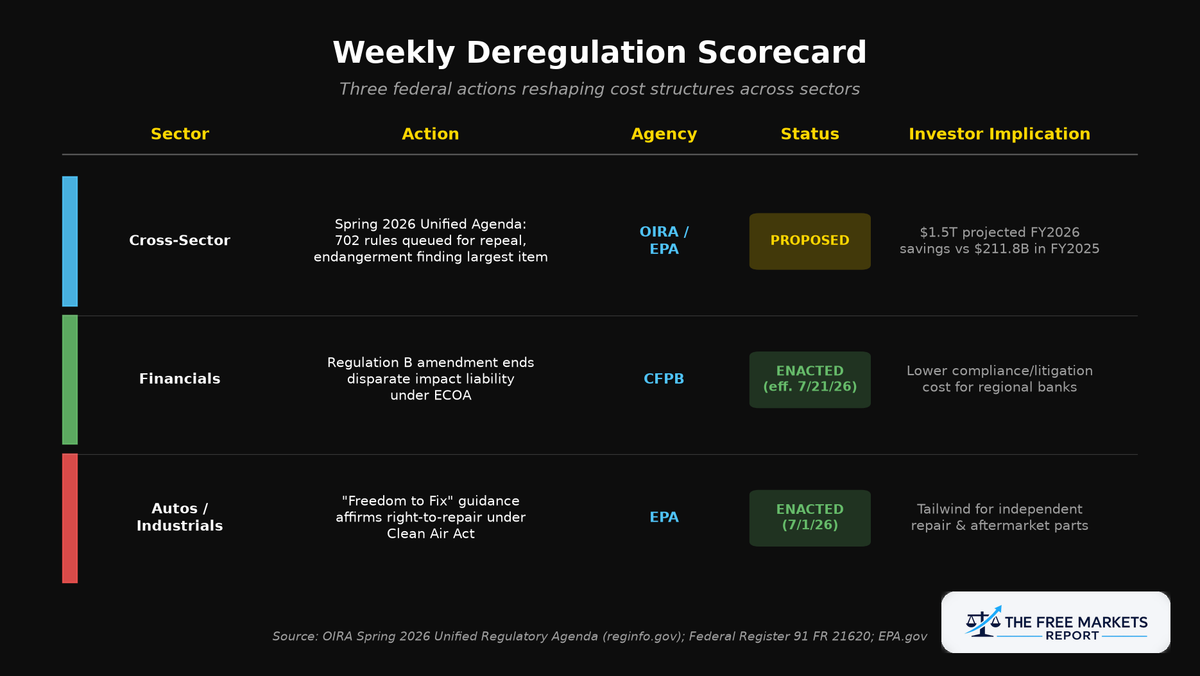

Key Highlights

- OIRA's Spring 2026 Unified Regulatory Agenda queues 702 deregulatory actions across 78 federal agencies, on top of 752 rollbacks already finalized since the fiscal year began on October 1, 2025 (The Star).

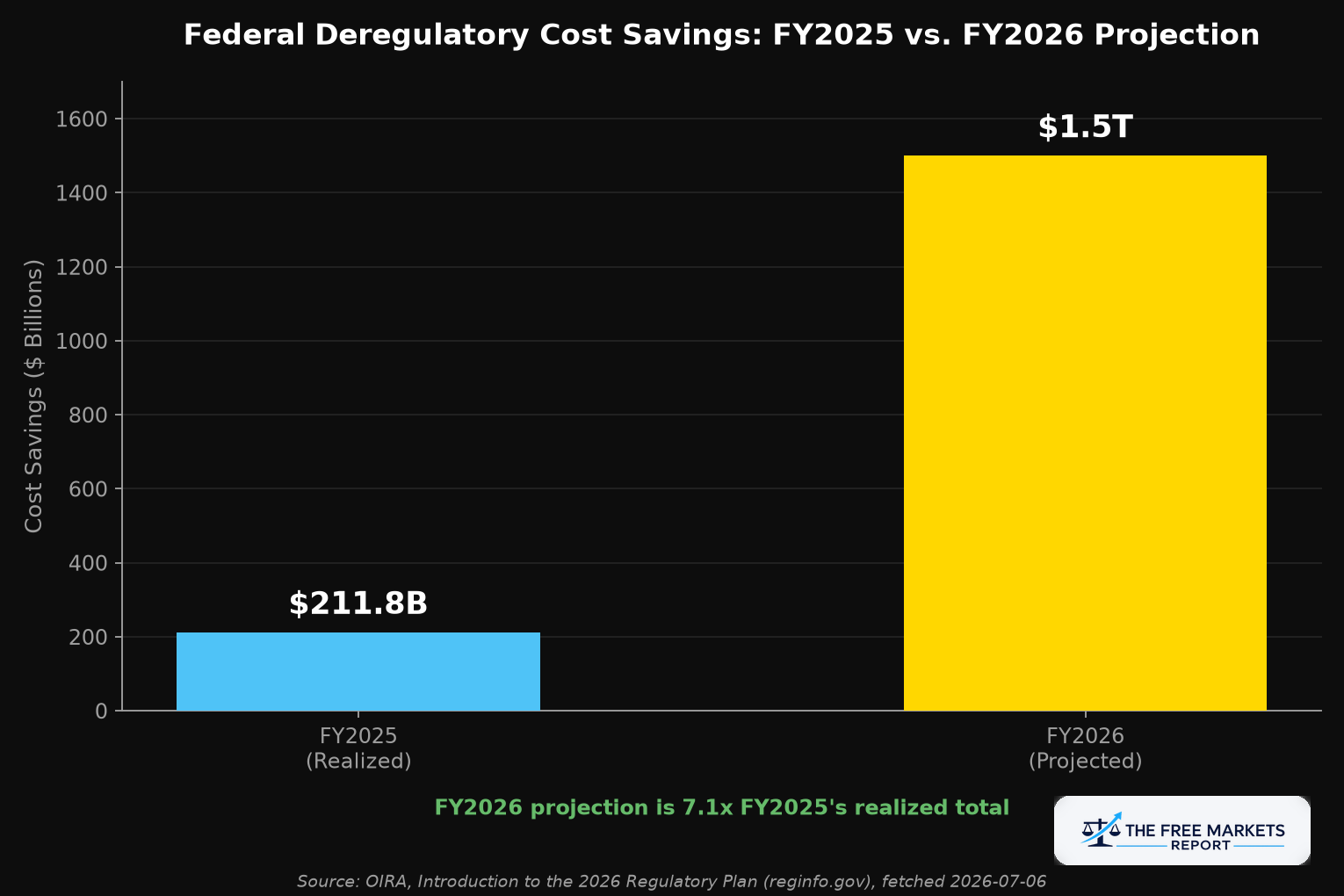

- The agenda projects $1.5 trillion in FY2026 cost savings, versus $211.8 billion realized in FY2025, a 7.1x jump (OIRA).

- The single largest item in the pipeline is repeal of the EPA's 2009 greenhouse gas endangerment finding, which the administration says has driven $1.3 trillion in downstream compliance costs (The Star).

- CFPB's Regulation B rule eliminating disparate impact liability under the Equal Credit Opportunity Act takes effect July 21, 2026 (Federal Register).

- EPA's July 1 "Freedom to Fix" guidance affirms a right-to-repair path for independent auto shops and aftermarket parts makers (EPA).

The Deregulation Pipeline Just Got Its Biggest Load Yet

The Office of Information and Regulatory Affairs released its Spring 2026 Unified Regulatory Agenda last week, and the number that jumps out is 702. That is how many existing federal rules the administration wants to eliminate, spread across 78 federal agencies (reginfo.gov, The Star). It builds on 752 rollbacks already finalized since the fiscal year began on October 1, 2025. The pipeline of deregulatory action in motion right now is roughly twice the scale seen at any point during the administration's first term (The Star).

The dollar figures are the real headline for investors. OIRA's own introduction to the plan states that deregulatory efforts yielded $211.8 billion in cost savings for Americans in fiscal 2025. Fiscal 2026 is projected to go far beyond that: a record $1.5 trillion in projected savings, more than seven times the prior year's realized total (OIRA).

The single largest line item driving that number is the planned repeal of the EPA's 2009 endangerment finding, the legal foundation underneath most federal greenhouse gas regulation. The administration attributes $1.3 trillion in cumulative cost to the emissions policies that finding enabled (The Star). Undoing a foundational finding is a multi-year legal process, not a single rule change, but the direction is now explicit at the top of the federal registry.

Two structural shifts make this pipeline harder to slow down than in the first term. The Supreme Court has ruled that the president can remove independent agency heads at will, and agencies must now coordinate their regulatory calendars through OIRA before acting (The Star). Mark Paoletta, acting as the administration's top regulator, coordinates that calendar. For investors, centralization matters because it reduces the odds of an individual agency slow-walking a directive, a recurring friction point from 2017 through 2020.

Banking's Disparate Impact Standard Just Went Away

Buried inside the broader deregulatory push is a narrower but consequential change for financials. The Consumer Financial Protection Bureau's final rule amending Regulation B, published in the Federal Register on April 22, 2026 under Docket No. CFPB-2025-0039, takes effect July 21, 2026 (Federal Register).

Legal analysis from Venable LLP finds the rule "effectively eliminates disparate impact as a theory of liability" under the Equal Credit Opportunity Act, while leaving disparate treatment claims, including facially neutral criteria used as proxies for prohibited characteristics, intact (Venable). Lenders can no longer be held liable simply because a lending pattern produces a statistically uneven outcome across protected groups; a plaintiff now must show intent or a proxy criterion.

For regional and community banks, that is a direct reduction in tail-risk litigation exposure and compliance overhead tied to fair-lending model audits, one of the more expensive corners of bank compliance since the 2010s.

The Right to Fix Your Own Truck

The third piece of this week's tracker sits at the intersection of transportation and industrials. On July 1, 2026, the EPA issued guidance affirming that the Clean Air Act supports Americans' "Freedom to Fix" their own vehicles and equipment, following a White House presidential memorandum dated June 29, 2026 (EPA).

The guidance restates an existing but underenforced requirement: manufacturers of light-duty vehicles, light-duty trucks, and heavy-duty commercial trucks must provide full emissions-related service information, training materials, onboard diagnostic data, passthrough reprogramming, and diagnostic tools to independent repair shops, not just franchised dealers (EPA). For nonroad diesel equipment, temporary disablement of emissions controls for repair purposes is confirmed allowed under existing law.

This is an enforcement posture shift, not a new statute. It makes it materially harder for manufacturers to lock diagnostic data behind proprietary dealer networks. The direct beneficiaries are independent repair chains and the aftermarket parts suppliers that serve them.

Weekly Deregulation Scorecard

The Math Behind the Number

Ideas to Watch

- iShares Russell 2000 ETF (IWM): broad small-cap exposure captures the compounding effect of compliance-cost relief across hundreds of smaller domestic companies that carry disproportionate regulatory burden relative to revenue. NAV was $297.55 with a 22.01% year-to-date total return and a 0.19% expense ratio, both as of early July 2026 (iShares).

- SPDR S&P Regional Banking ETF (KRE): the direct read-through on the Regulation B disparate impact rollback. Total net assets stood at $5.2 billion with a 0.35% gross expense ratio as of July 2, 2026 (SSGA). Lower fair-lending litigation exposure is a real, if modest, structural tailwind for regional bank compliance budgets.

- O'Reilly Automotive (ORLY): a direct beneficiary of the Freedom to Fix guidance, since independent repair shops depend on the same manufacturer diagnostic data the EPA guidance protects. Shares traded at $84.37 as of July 6, 2026 (Investing.com).

The Principle

The throughline across all three actions this week is the one that has defined this publication's coverage all year: when compliance costs fall, whether through repeal, a narrowed liability standard, or a reaffirmed right, capital finds its way to whoever previously bore that cost. The size of this week's agenda is unusual. The mechanism by which it becomes an investable thesis is not. Watch where the cost used to sit, and watch who no longer has to pay it.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.