A No-Action Letter Just Opened the World's Biggest Crypto Market to U.S. Traders

The CFTC's May 29, 2026 order lets Coinbase route American clients into global perpetual futures for the first time, but the relief is staff-level and already under legal attack.

Key Highlights

- On May 29, 2026, the CFTC issued Release 9241-26, an interpretive letter and no-action position letting Coinbase Financial Markets, Inc., a registered futures commission merchant, treat certain crypto perpetual contracts as "foreign futures" under CFTC Regulation 30.1.[1]

- The same day, the CFTC issued Release 9242-26, a policy statement on listing perpetual contracts, alongside an order permitting a Bitcoin-referenced perpetual contract to list as a self-certified futures contract.[2]

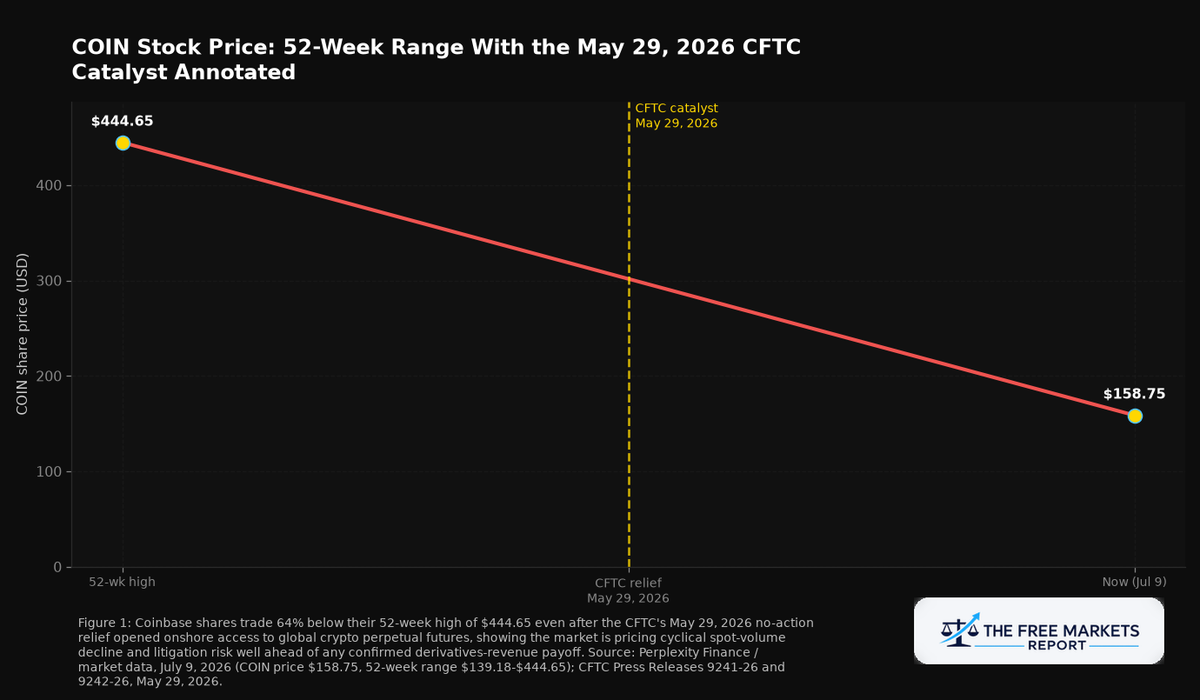

- Coinbase Global, Inc. (COIN) traded at $158.75 on July 9, 2026, market capitalization approximately $41.8 billion, roughly 64% below its 52-week high of $444.65.[3]

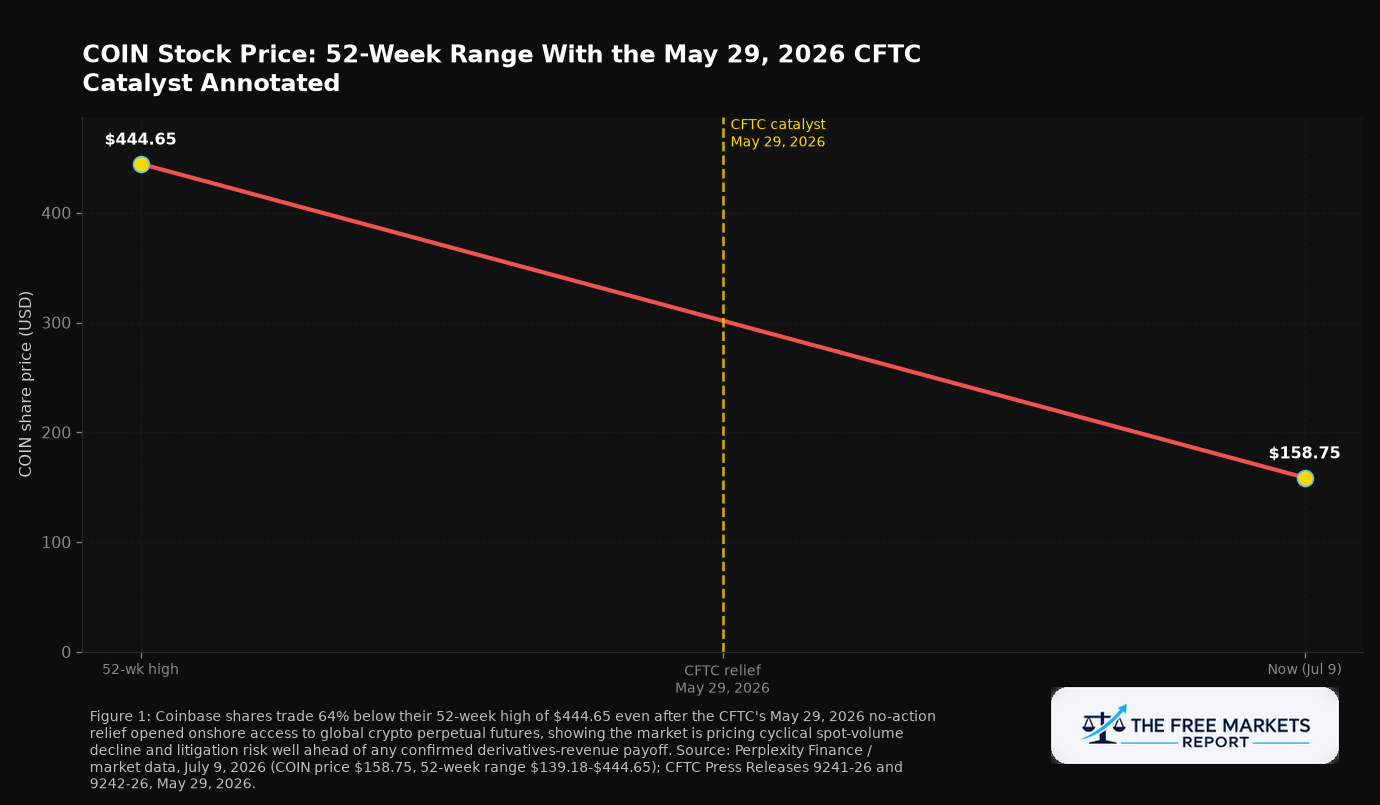

- Coinbase reported total revenue of $1.41 billion for Q1 2026 (transaction revenue $755.8 million, subscription and services $583.5 million) and a net loss of $394.1 million, per its Form 10-Q.[4]

- CME Group sued the CFTC in June 2026 arguing perpetuals are legally "swaps," not futures, under Dodd-Frank; the underlying no-action relief can itself be narrowed or withdrawn without notice-and-comment rulemaking.[5][6]

A staff letter most retail investors will never read just did something no act of Congress has managed in over a decade: it gave American traders a compliant, onshore door into the product that dominates global crypto trading volume. On May 29, 2026, the CFTC's Market Participants Division issued an interpretation and no-action position for Coinbase Financial Markets, Inc., confirming certain crypto perpetual contracts could be categorized as "foreign futures" under Regulation 30.1.[1] The same day, the Commission issued a policy statement on listing perpetual contracts and an order permitting a Bitcoin-referenced perpetual contract to self-certify as a futures product.[2] Perpetual futures, contracts with no expiration date that roll via funding payments, dominate global crypto derivatives volume, concentrated for years on offshore venues U.S. persons were not supposed to access. The question for investors: does turning that gray-market product into a regulated revenue line change the model enough to matter, and how much is already priced in.

The Product U.S. Regulators Had Kept Offshore

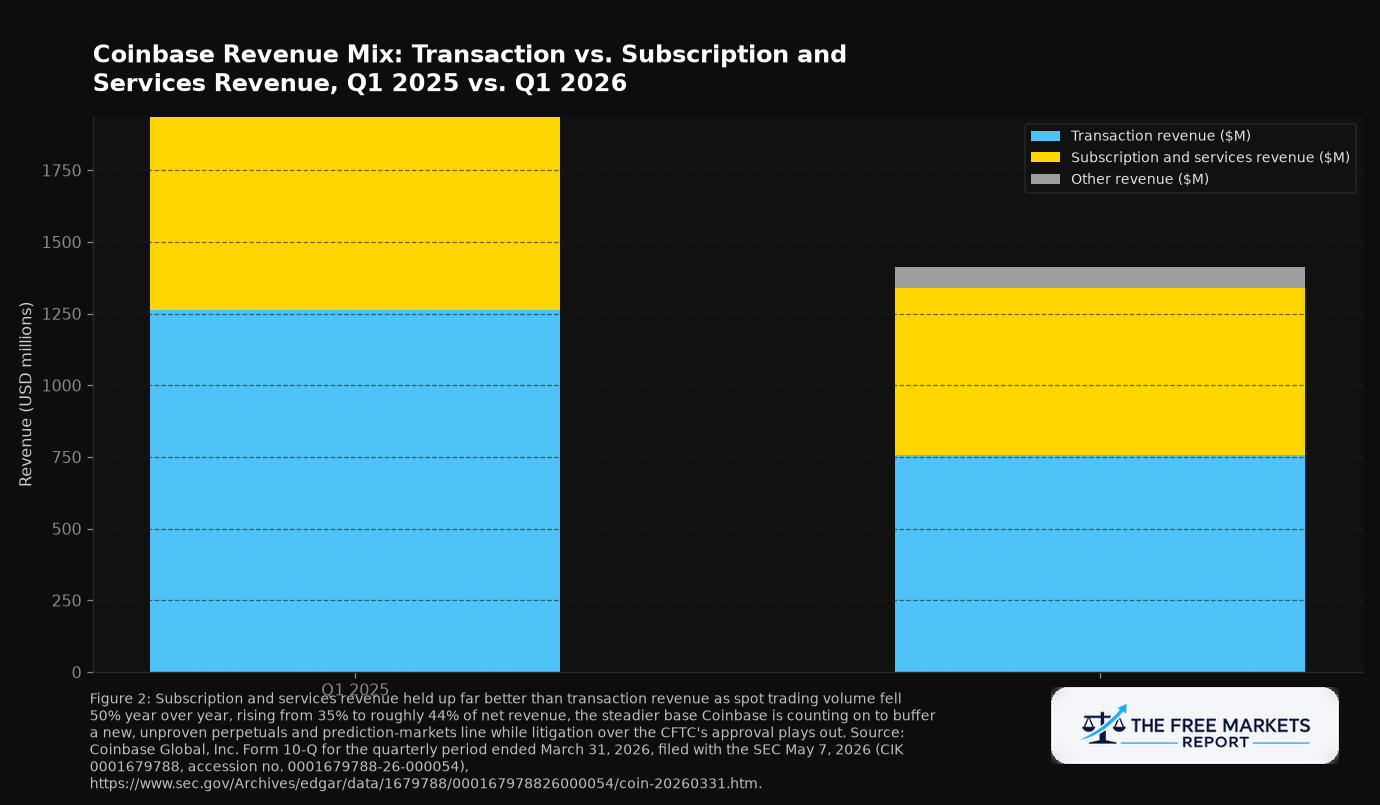

Before May 29, U.S. persons had no compliant, domestically regulated pathway into perpetual futures; access ran through offshore venues outside CFTC oversight.[7] The four-part May 29 package changed that not through notice-and-comment rulemaking, but through staff interpretive and no-action authority. The letter treats Coinbase Financial Markets' foreign-listed perpetuals as "foreign futures," and states staff will not recommend enforcement action against the firm for posting customer crypto and stablecoins with its foreign broker affiliate as margin.[1] The EU caps retail crypto CFD leverage at 2:1 under ESMA rules, and the UK's FCA has banned retail crypto derivatives outright since January 6, 2021.[8] The gap between the U.S. framework and those jurisdictions now favors U.S. market access rather than restricting it.

Coinbase Global (COIN): The Financial Mechanics

Coinbase Global, Inc. (COIN) is the direct, and so far sole named, beneficiary of the interpretive relief, and its underlying business is worth pricing honestly. For the three months ended March 31, 2026, Coinbase reported total revenue of $1.41 billion, down from $1.94 billion a year earlier, per its Form 10-Q filed with the SEC on May 7, 2026.[4] Transaction revenue came in at $755.8 million; subscription and services revenue, covering custody, staking, and Coinbase One, contributed $583.5 million, roughly 44% of net revenue.[4] Trading volume fell to $202 billion from $401 billion a year earlier, a 50% decline tracking the broader crypto pullback.[4] Coinbase posted a net loss of $394.1 million for the quarter, driven largely by unrealized mark-to-market losses on its crypto holdings, even as Adjusted EBITDA stayed positive at $303.3 million, its 13th consecutive positive quarter.[9] Management separately disclosed prediction markets reaching an annualized revenue run rate above $100 million within roughly two months of U.S. launch, and retail derivatives already annualizing above $200 million, both predating the fuller contribution of the May 29 relief.[9]

The Bull Case and the Bear Case

The bull case: derivatives and prediction markets carry different economics than spot trading, and Coinbase is now the only U.S.-listed, CFTC-registered FCM routing customers into the dominant global crypto derivatives category. A subscription base near half of net revenue buffers the ramp, and a 13th straight EBITDA-positive quarter suggests the core model can absorb it.[9][4]

The bear case is that the relief creating this thesis was never voted into a binding rule. No-action letters "can be narrowed or withdrawn without notice-and-comment rulemaking," per industry legal analysis of the May 29 action.[6] More acute: CME Group sued the CFTC in June 2026, arguing perpetuals are legally swaps under Dodd-Frank and that the Commission bypassed notice-and-comment procedure; the CFTC has called the suit "frivolous."[5] If CME prevails, perpetuals could be reclassified as swaps under a stricter margin and clearing regime, threatening the derivatives revenue Coinbase is counting on to offset declining spot volume. Falsification condition: a federal court ruling against the CFTC in CME Group v. CFTC, or a CFTC narrowing/withdrawal of the Coinbase relief before that litigation resolves, would invalidate the durable higher-margin thesis regardless of near-term derivatives revenue.

INVESTMENT IDEA: Coinbase Global, Inc. (COIN)

INVESTMENT IDEA: Coinbase Global, Inc. (COIN)

Thesis type: Primary beneficiary

Deregulatory catalyst: CFTC Release 9241-26 (interpretive letter/no-action, May 29, 2026) letting Coinbase Financial Markets route U.S. customers to crypto perpetual futures as "foreign futures" under Reg 30.1, alongside Release 9242-26.[^1][^2]

Current price: $158.75 (July 9, 2026, Perplexity Finance / market data); market cap ~$41.8B; TTM P/E -65.6; 52-week range $139.18-$444.65.[^3]

Key financial data: Total revenue $1.41B Q1 2026 (transaction revenue $755.8M, subscription/services $583.5M, ~44% of net revenue); net loss $394.1M; Adjusted EBITDA $303.3M, 13th consecutive positive quarter. Source: Form 10-Q filed May 7, 2026; Coinbase Q1 2026 IR release.[^4][^9]

Regulatory constraint removed: Before May 29, 2026, no CFTC-registered FCM could compliantly route U.S. customers into perpetual futures, the largest global crypto derivatives category.[^1][^7]

Bull case: A subscription base near half of net revenue buffers the ramp of a new, higher-margin derivatives/prediction-markets line; Coinbase is the only named U.S.-listed FCM with compliant access to offshore-dominant perpetuals liquidity.[^9]

Bear case: The relief is staff-level, not a rule, and can be narrowed or withdrawn without notice-and-comment rulemaking; CME Group's June 2026 suit argues perpetuals are swaps, not futures.[^5][^6]

What to watch: The docket and ruling in CME Group v. CFTC; any CFTC action narrowing/withdrawing the Coinbase relief; derivatives/prediction-markets revenue disclosed in the next 10-Q.

Time horizon: 6-18 monthsThe Principle

Regulatory access is not regulatory permanence. A no-action letter can open a market faster than a rule ever could, and it can close just as fast, without a vote. Coinbase trading well below its 52-week high while adding a higher-margin product line reflects a market pricing execution risk and now litigation risk into a growth avenue that rests on staff discretion, not statute. Watch the courtroom, not just the volume.

Footnotes

[1] CFTC, "Commission Staff Confirms the Categorization of Certain Crypto Asset Perpetuals as Foreign Futures and Issues No-Action Letter Regarding FCM Transfers of Customer Crypto Assets to Foreign Brokers as Margin," Release 9241-26, May 29, 2026. https://www.cftc.gov/PressRoom/PressReleases/9241-26

[2] CFTC, "CFTC Issues Policy Statement Concerning the Listing of Perpetual Contracts," Release 9242-26, May 29, 2026. https://www.cftc.gov/PressRoom/PressReleases/9242-26

[3] Perplexity Finance / market data, July 9, 2026 (live quotes).

[4] Coinbase Global, Inc., Form 10-Q for the quarterly period ended March 31, 2026, filed with the SEC May 7, 2026 (CIK 0001679788, accession no. 0001679788-26-000054). https://www.sec.gov/Archives/edgar/data/1679788/000167978826000054/coin-20260331.htm

[5] crypto.news, "The Offshore Giants Watching the CME-CFTC Fight Over Perpetual Futures," June 24, 2026. https://crypto.news/cme-cftc-lawsuit-perpetual-futures-swaps/

[6] The Industry Spread, "How the CFTC's Crypto-Perpetuals Opening Splits Four Markets," June 7, 2026. https://theindustryspread.com/cftc-crypto-perpetuals-opening-splits-four-markets/

[7] The Industry Spread, "How the CFTC's Crypto-Perpetuals Opening Splits Four Markets," June 7, 2026. https://theindustryspread.com/cftc-crypto-perpetuals-opening-splits-four-markets/

[8] The Industry Spread, "How the CFTC's Crypto-Perpetuals Opening Splits Four Markets," June 7, 2026, on EU MiFID II/ESMA 2:1 retail leverage cap and UK FCA PS20/10 retail ban effective January 6, 2021. https://theindustryspread.com/cftc-crypto-perpetuals-opening-splits-four-markets/

[9] Coinbase Global, Inc., "Coinbase Q1 Financial Results Show Resilient Financial Performance Driven by New All-Time High Crypto Trading Volume Market Share," investor relations release, May 7, 2026. https://investor.coinbase.com/news/news-details/2026/Coinbase-Q1-Financial-Results-Show-Resilient-Financial-Performance-Driven-by-New-All-Time-High-Crypto-Trading-Volume-Market-Share/default.aspx

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.