The NRC Just Rewrote the Reactor Rulebook. Uranium Is the Trade.

A 553-page NRC proposal to double license-renewal terms and streamline reactor siting turns uranium exposure from a story stock into a structural sector call.

Key Highlights

- On July 1, 2026, the NRC proposed "Modernizing Reactor Licensing, Safety Oversight, and Siting Practices" (Docket NRC-2025-0975; RIN 3150-AL44), a 553-page rule bundling 17 measures across the entire reactor lifecycle and implementing Executive Order 14300.[1]

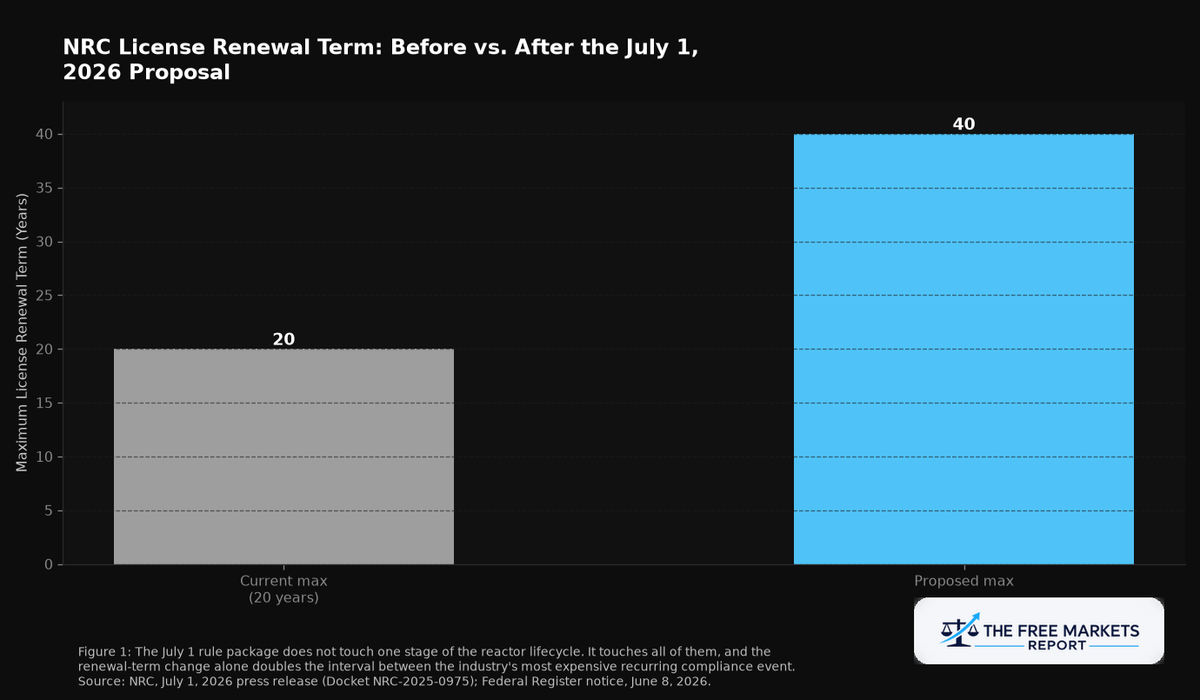

- The rule would extend the maximum reactor license-renewal term from 20 years to up to 40 years per renewal application, and lets early site work begin under a general license once an application is docketed.[1][4]

- Global X Uranium ETF (URA) trades at $42.33 as of July 9, 2026, up 1.61% on the day, with a Perplexity Finance-tracked market capitalization of approximately $4.23 billion; Global X's own factsheet has historically cited materially higher AUM figures, and other trackers put AUM anywhere from roughly $3.2 billion to $6.45 billion, so treat any single AUM figure as approximate.[7][8]

- The proposal is not final: it carries a 45-day comment window after Federal Register publication, and it faces two live legal fronts, Beyond Nuclear/Sierra Club's D.C. Circuit petition (No. 24-1318) and the Last Energy/Texas/Utah v. NRC suit in the Eastern District of Texas, either of which could reshape or delay parts of the framework.[5][6]

- Demand-side beneficiaries named alongside the supply-side uranium trade include Constellation Energy (CEG) and Vistra Corp. (VST), both up more than 2.6% intraday on July 9, 2026, reflecting the data-center power demand thesis that pairs with the licensing overhaul.[9]

This is the most sweeping rewrite of American reactor licensing in a generation, and it landed with less market attention than it deserves. On July 1, 2026, the NRC proposed a rule titled "Modernizing Reactor Licensing, Safety Oversight, and Siting Practices," a 553-page document spanning 10 CFR Parts 2, 50, 51, 52, 53, 54, 71, and 100, that bundles 17 separate modernization measures covering design approval, construction, operation, license renewal, fuel handling, and decommissioning.[1] It directly implements Sections 5(f), 5(h), and 5(i) of Executive Order 14300, signed May 23, 2025, which ordered a top-to-bottom reform of the NRC.[2] For a sector where regulatory friction has been the largest constraint on new capacity for four decades, the investor question is simple: does removing that friction change the economics enough to matter, and who captures the upside.

A Forty-Year License Where Twenty Used to Be the Ceiling

Start with the headline mechanic. The proposed rule would extend the maximum reactor license-renewal term from 20 years to up to 40 years per renewal application.[1] The NRC's own reasoning is notable: the agency has said the original 40-year total operating limit was set for "antitrust and financial reasons," not safety, and that licensees have already demonstrated the ability to manage aging issues over decades of operating history.[1] This is not a safety rollback story; it is a compliance-cycle story. Every relicensing round has historically meant a multi-year, multi-million-dollar regulatory review for the existing fleet. Stretching the interval between those reviews changes the cash-flow profile of every reactor whose license comes up for renewal in the coming decade.

The rule's other provisions target the front end of the pipeline just as much as the back end. It allows early site work under a general license once an application is docketed, removing a sequential-approval bottleneck that has stalled construction starts. It creates risk-informed alternatives to some prescriptive safety analyses, permits performance-based emergency planning zones tailored to a facility's actual design rather than a blanket 10-mile zone, and aligns U.S. quality-assurance requirements more closely with international standards, widening the supplier base for new-build components.[1] None of these changes are hypothetical. They build on a rulemaking sequence running more than a year: the NRC finalized its Part 53 licensing framework for advanced reactors on March 30, 2026, the first new reactor licensing framework since 1989, then issued a June 4, 2026 policy statement narrowing mandatory hearing requirements that had separately consumed roughly 1,500 hours of NRC staff preparation, cost applicants millions of dollars, and added roughly six months of average delay to licensing approvals.[3][4]

The Fee Schedule Tells the Same Story in Dollars

The NRC's own fee reform, finalized June 16, 2026 under EO 14300 Section 5(a), quantifies how much friction was priced into the system. The new standard professional hourly licensing fee is $337, up from roughly $318 in fiscal 2025, but the same reform introduced a reduced rate of $154 an hour specifically for advanced-reactor applicants and pre-applicants.[3] That is a rate cut of more than 50% for the exact class of projects, small modular reactors and advanced designs, the July 1 proposal is designed to accelerate. Take those figures together with the renewal-term extension and the early-site-work provision, and the pattern is consistent: a coordinated sequence, EO, licensing framework, fee structure, hearing process, siting rule, aimed at compressing the regulatory cost curve across the nuclear build-and-operate cycle.

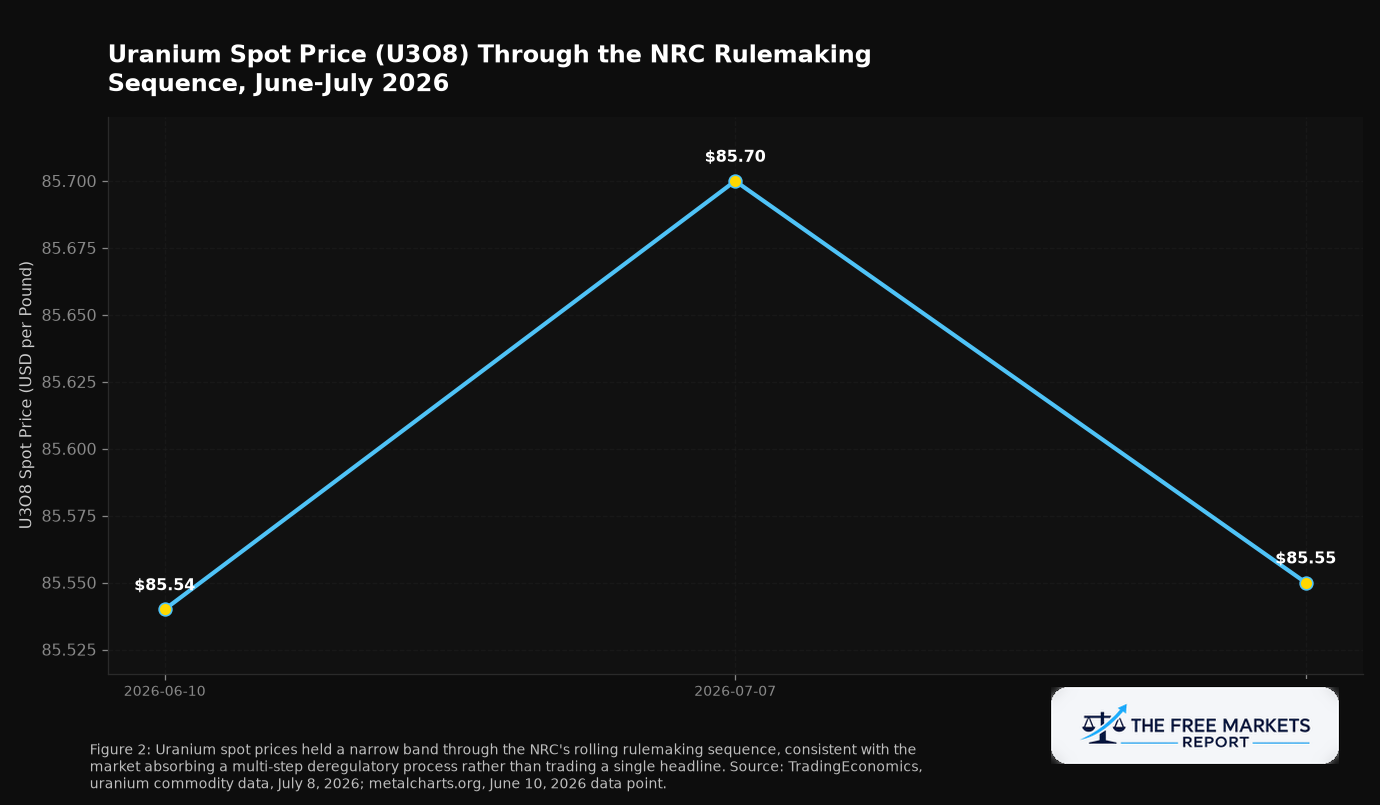

The uranium spot market has not been indifferent to this sequence. Spot U3O8 traded at $85.55 to $85.85 per pound as of July 7 to 8, 2026, a level that has held broadly steady through the rulemaking cadence of the past several weeks.[10] That stability, rather than a spike, is informative: it suggests the market has been pricing the deregulatory pipeline gradually as each rule landed, not reacting to one surprise announcement, consistent with a structural repricing rather than a speculative pop.

Companies on the Board: The Miners, the Utilities, and the Buyers of Power

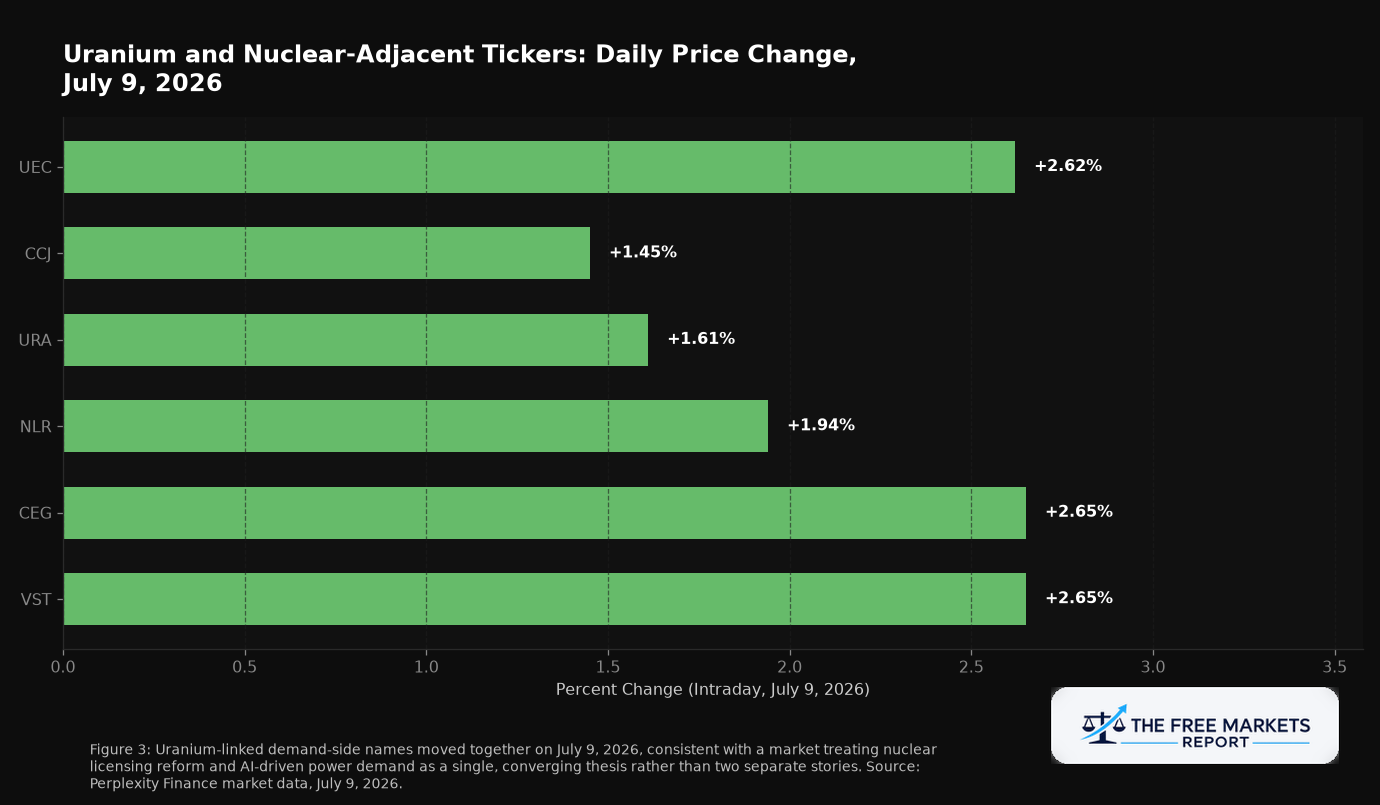

Uranium Energy Corp. (UEC) is the largest U.S.-listed uranium miner, most directly exposed to streamlined federal-land permitting; UEC traded at $10.19 on July 9, 2026, up 2.62%, with a market capitalization near $5.04 billion.[9] Cameco Corporation (CCJ), the largest publicly traded uranium producer globally, traded at $96.10, up 1.45%, with a market capitalization near $41.85 billion.[9] On the demand side, Constellation Energy Corporation (CEG) traded at $251.00, up 2.65%, market cap near $90.13 billion, and Vistra Corp. (VST) traded at $158.92, also up 2.65%, market cap near $53.59 billion.[9] CEG and VST sit at the intersection of two converging theses: nuclear is the only dispatchable, zero-carbon baseload source that scales for the data-center buildout, and the licensing regime governing that capacity is being rewritten to cut multi-year delays from both new construction and relicensing.

None of these moves happen in a vacuum from the regulatory sequence, and none are guaranteed to hold if the sequence stalls. That favors a sector thesis over a single-stock call: the catalyst is diffuse across miners, fuel-cycle companies, reactor operators, and utilities, a textbook case for an ETF rather than a bet concentrated in one balance sheet.

The Case for Skepticism, and Why It Matters for Investors

The consensus read on a reform this broad is that deregulation mechanically translates into faster builds and cheaper capital. But the NRC's own litigation history says the mechanism is contested, not settled. Two active legal fronts bear directly on this rule. First, Beyond Nuclear and the Sierra Club have a live petition before the D.C. Circuit (No. 24-1318) challenging the NRC's 2024 license-renewal environmental-review rule under 10 C.F.R. Section 51.53, a challenge the NRC's own staff answer acknowledges is a template for objections to the broader relicensing framework once the July 2026 package is finalized.[5] Second, and more structurally important, Last Energy, Texas, and Utah have sued the NRC in the Eastern District of Texas, arguing the agency's Atomic Energy Act authority does not extend to small modular and microreactors below a specific materiality threshold.[6] A plaintiff win would not just delay the rule; it could strip the NRC of licensing authority over the very small-reactor segment this reform is designed to accelerate, replacing a single federal framework with a fragmented state-by-state patchwork that could raise, not lower, compliance costs for multi-state SMR developers.

There is a second, separate risk that has nothing to do with courts. The rule announced July 1, 2026 is a proposal, not a final regulation. It carries a standard 45-day comment period following Federal Register publication, with the NRC targeting a Commission vote in late 2026 or early 2027.[1] A future Congress or Commission composition could slow-walk, narrow, or decline to finalize elements of the package during that window. Even a fully finalized rule only solves the supply side. The demand thesis, that data centers need nuclear baseload badly enough to absorb newly licensed capacity, depends on continued hyperscaler capital expenditure growth. A slowdown in AI infrastructure spending would leave newly de-risked reactor capacity chasing a smaller pool of contracted demand than the current setup assumes.

Falsification condition: if the D.C. Circuit vacates or remands material portions of the NRC's license-renewal environmental-review framework in Beyond Nuclear v. NRC (No. 24-1318), or if the Eastern District of Texas rules for the plaintiffs in Last Energy/Texas/Utah v. NRC before the Commission's targeted late-2026/early-2027 vote on the July 1 proposal, the licensing-acceleration thesis underlying this trade should be considered materially weakened, not merely delayed.

Investment Idea

SECTOR PLAY: Global X Uranium ETF (URA)

Underlying exposure: 54 holdings tracking the Solactive Global Uranium & Nuclear Components Total Return Index, spanning uranium miners, physical uranium holders, and nuclear-fuel-cycle and equipment companies; inception November 4, 2010.[^7]

AUM: Approximately $4.23 billion per Perplexity Finance market-cap tracking as of July 9, 2026; separate June 2026 tracker data put URA AUM as high as roughly $6.0-$6.45 billion, so treat any single AUM figure as approximate and prefer an issuer factsheet as the Tier 1 reference point when available.[^7][^8]

Expense ratio: 0.69%, per Global X's fund page.[^7]

Deregulatory catalyst: NRC's July 1, 2026 proposed rule (Docket NRC-2025-0975) extending license-renewal terms to up to 40 years and streamlining construction/siting, layered on the March 30, 2026 Part 53 advanced-reactor framework and the June 16, 2026 fee reform.[^1][^3][^4]

Performance since catalyst: uranium spot has held an $85.54-$85.70/lb range from June 10 through July 7-8, 2026, spanning the rulemaking sequence; a direct URA-vs-SPY return series since the specific July 1, 2026 rule date was not independently verified in this research cycle and is not asserted here.[^10]

Why the ETF rather than individual stocks: the catalyst is diffuse across mining, fuel-cycle, and reactor-adjacent equipment companies, and individual miner economics vary by jurisdiction and project stage, exactly the single-company execution risk a sector vehicle diversifies away.

Key holdings benefiting: the fund's mandate concentrates on uranium mining, physical uranium, and nuclear fuel-cycle and equipment names most directly exposed to the July 1 proposal's licensing and siting provisions.[^7]

Alternate vehicle: VanEck Uranium and Nuclear ETF (NLR) offers a lower expense ratio of 0.52% and reported AUM of $4.03 billion as of July 7, 2026 per VanEck's fund page, tracking the MVIS Global Uranium & Nuclear Energy Index; a useful comparison point given its more consistent Tier 1-sourced figures.[^8]

Bear case: the Beyond Nuclear/Sierra Club D.C. Circuit petition (No. 24-1318) and the Last Energy/Texas/Utah v. NRC suit both target the legal foundations this thesis depends on; a plaintiff win in either could delay or fragment implementation. The rule also remains a proposal subject to a 45-day comment period, and the demand side depends on data-center capex growth that is not guaranteed to persist.[^5][^6]

What to watch: the D.C. Circuit's review in Beyond Nuclear v. NRC (No. 24-1318), the Eastern District of Texas ruling in Last Energy/Texas/Utah v. NRC, and the NRC's targeted late-2026/early-2027 Commission vote finalizing Docket NRC-2025-0975.

The Principle

Deregulation does not create demand. It removes the friction that keeps supply from meeting demand that already exists. The NRC's July 1 proposal is a bet that four decades of licensing friction, not physics or economics, has been the binding constraint on American nuclear capacity. The data-center power buildout supplies the demand side of that bet independent of any rule change. What the rule changes is how fast, and how cheaply, the supply side can respond. That is a sector thesis, not a single-company story, and it will be tested in federal court before it is tested by construction crews.

Footnotes

[1] U.S. Nuclear Regulatory Commission, press release announcing proposed rule "Modernizing Reactor Licensing, Safety Oversight, and Siting Practices," Docket ID NRC-2025-0975, RIN 3150-AL44, July 1, 2026. https://www.nrc.gov/sites/default/files/cdn/doc-collection-news/2026/26-071.pdf

[2] The White House, Executive Order 14300, "Ordering the Reform of the Nuclear Regulatory Commission," signed May 23, 2025. https://www.whitehouse.gov/presidential-actions/2025/05/ordering-the-reform-of-the-nuclear-regulatory-commission/

[3] American Nuclear Society, "NRC News: FY 2026 Fees Finalized, Facility Licensing Reviews Launched," June 25, 2026. https://www.ans.org/news/article-8148/nrc-news-fy-2026-fees-finalized-facility-licensing-reviews-launched/

[4] Federal Register, NRC Policy Statement on Mandatory Hearings for Reactor Licensing, June 8, 2026 (published), referencing June 4, 2026 policy statement. https://www.govinfo.gov/content/pkg/FR-2026-06-08/pdf/2026-11451.pdf

[5] U.S. Nuclear Regulatory Commission, NRC Staff Answer opposing Beyond Nuclear/Sierra Club hearing request, referencing D.C. Circuit case No. 24-1318 challenging the 2024 license-renewal rule and GEIS. https://www.nrc.gov/docs/ML2523/ML25234A079.pdf; corroborated by NRC's Annual Report on Court Litigation (Calendar Year 2025). https://www.nrc.gov/docs/ML2602/ML26028A093.pdf

[6] E&E News, "NRC lawsuit could hand states power over advanced reactors," reporting on Last Energy/Texas/Utah v. NRC, filed December 30, 2024, U.S. District Court for the Eastern District of Texas. https://www.eenews.net/articles/nrc-lawsuit-could-hand-states-power-over-advanced-reactors/

[7] Global X ETFs, Global X Uranium ETF (URA) fund page, expense ratio and fund structure. https://www.globalxetfs.com/funds/ura/

[8] VanEck, Uranium and Nuclear ETF (NLR) fund page, AUM as of July 7, 2026 and expense ratio. https://www.vaneck.com/us/en/investments/uranium-nuclear-energy-etf-nlr/

[9] Perplexity Finance market data (live quotes), July 9, 2026, for URA, NLR, UEC, CCJ, CEG, and VST.

[10] TradingEconomics, uranium commodity spot price data, July 7-8, 2026. https://tradingeconomics.com/commodity/uranium

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.