The EEOC Just Tore Up a 46-Year Rule, and the Data Says Not So Fast

The EEOC just rescinded its 1979 affirmative action guidelines. The 2025 revocation of EO 11246 already showed what comes next, and it isn't what the headlines suggest.

Key Highlights

- On July 6, 2026, the EEOC's final interpretive rule rescinding 29 CFR 1608, the 1979 "Guidelines on Affirmative Action Appropriate Under Title VII," took effect under RIN 3046-AB39, published at 91 FR 40879 (Federal Register via GovInfo).

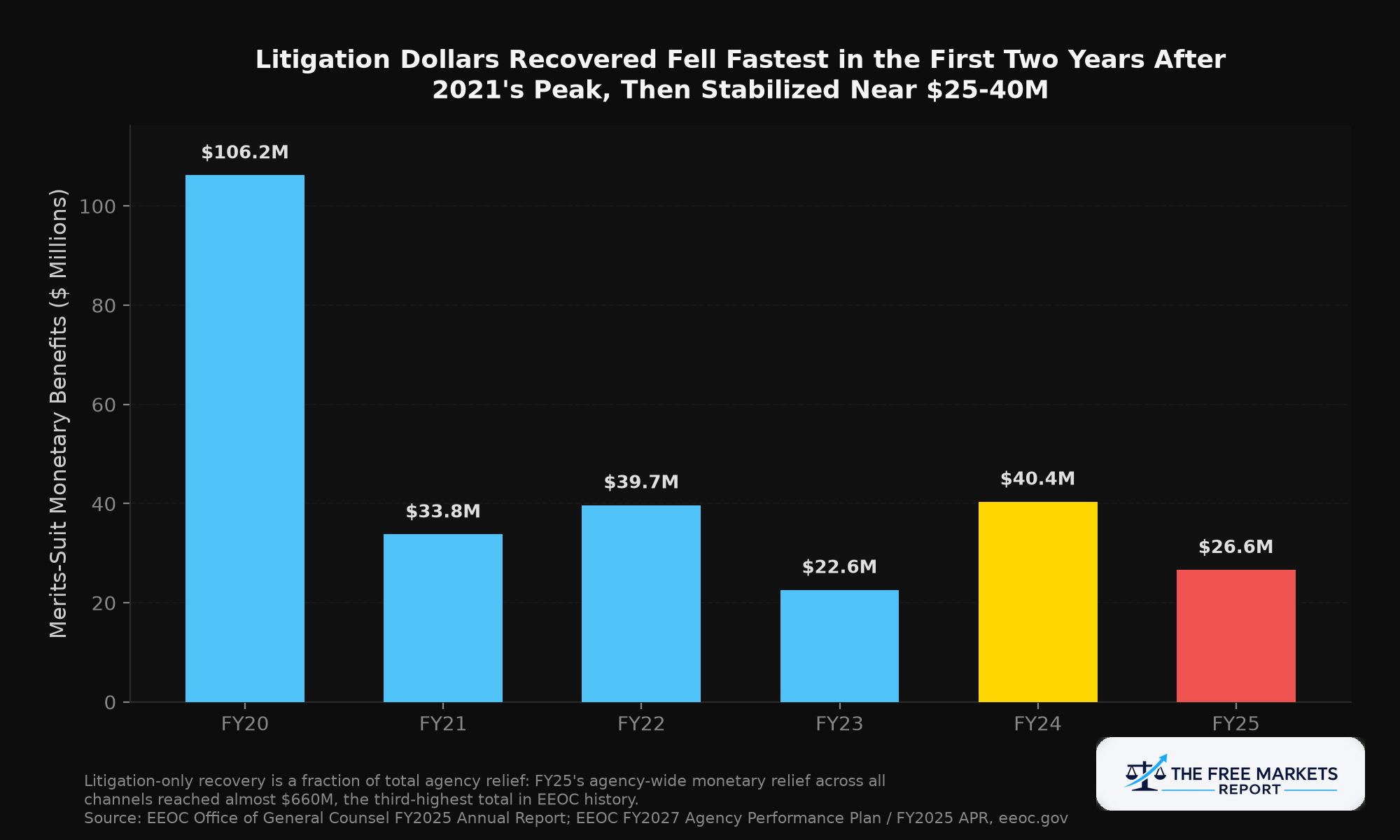

- This is the first of ten items on the EEOC's broader regulatory agenda to reach publication, including a proposal to rescind EEO-1 demographic reporting itself, a $273.1 million annual employer cost the agency's own paperwork burden estimate quantifies (Reginfo.gov; Ogletree Deakins).

- The last comparable purge, the January 2025 revocation of Executive Order 11246 by Executive Order 14173, did not translate into a collapse in EEOC enforcement dollars: agency-wide monetary relief hit almost $660 million in FY2025, the third-highest total in the agency's history (EEOC FY2027 Agency Performance Plan).

- Employers that built affirmative action plans around the now-rescinded guidance lose the Section 713(b) good-faith defense tied to it, even though the underlying Supreme Court precedents allowing voluntary affirmative action remain good law (HRWatchdog, Cal Chamber).

- The compliance-cost relief and litigation-risk reshuffling this creates has a real, if partial, read-through to publicly traded HR compliance software: Paycom Software (PAYC) discloses government-contractor affirmative action obligations and compliance-reporting applications as explicit line items in its own risk factors (Paycom 10-K digest, Stock Titan).

Washington just tore up a rulebook that survived four decades and eight presidential administrations, and the market's instinct is to assume this means less enforcement, less litigation, and less compliance spending. The last time the government ran this exact play, that instinct was wrong on two of three counts.

The Historical Episode: EO 11246's Revocation, One Year Later

On January 21, 2025, President Trump signed Executive Order 14173, revoking Executive Order 11246, the 1965 mandate requiring federal contractors to maintain written affirmative action plans under OFCCP enforcement authority (The White House). The comparison to today's rescission has a real limit: EO 11246 governed federal contractors through OFCCP, while the July 2026 rescission governs Title VII guidance applying to all covered employers through the EEOC. Related mechanisms, not identical ones.

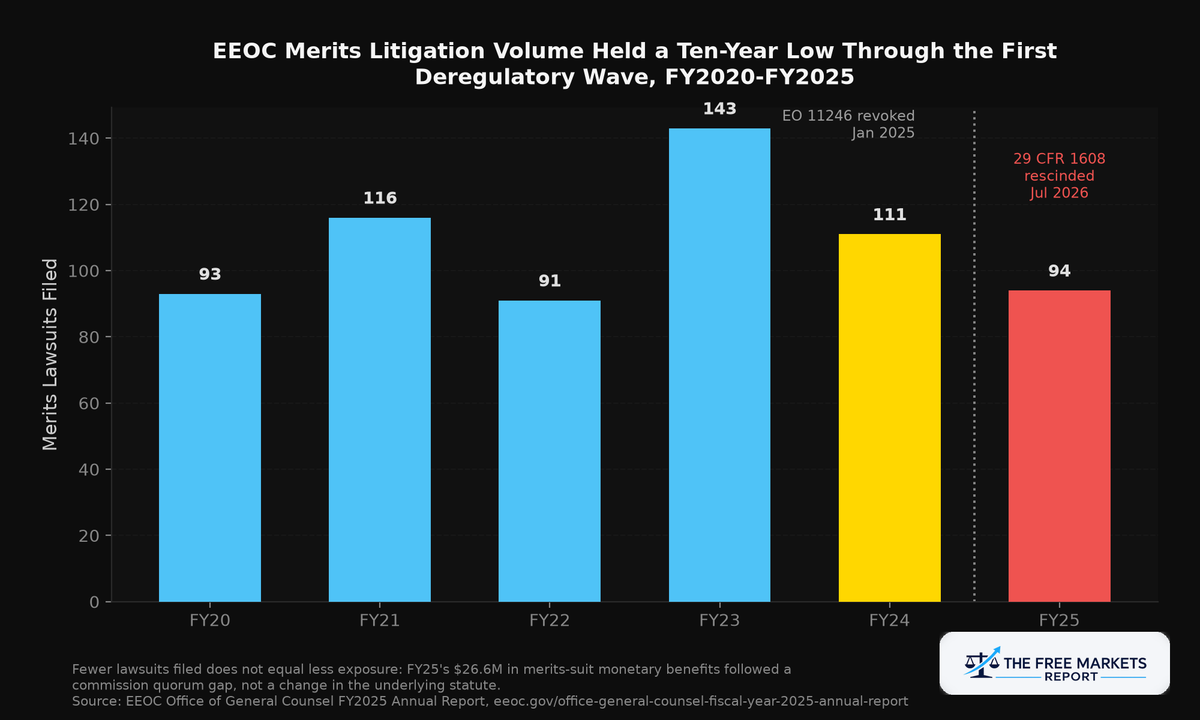

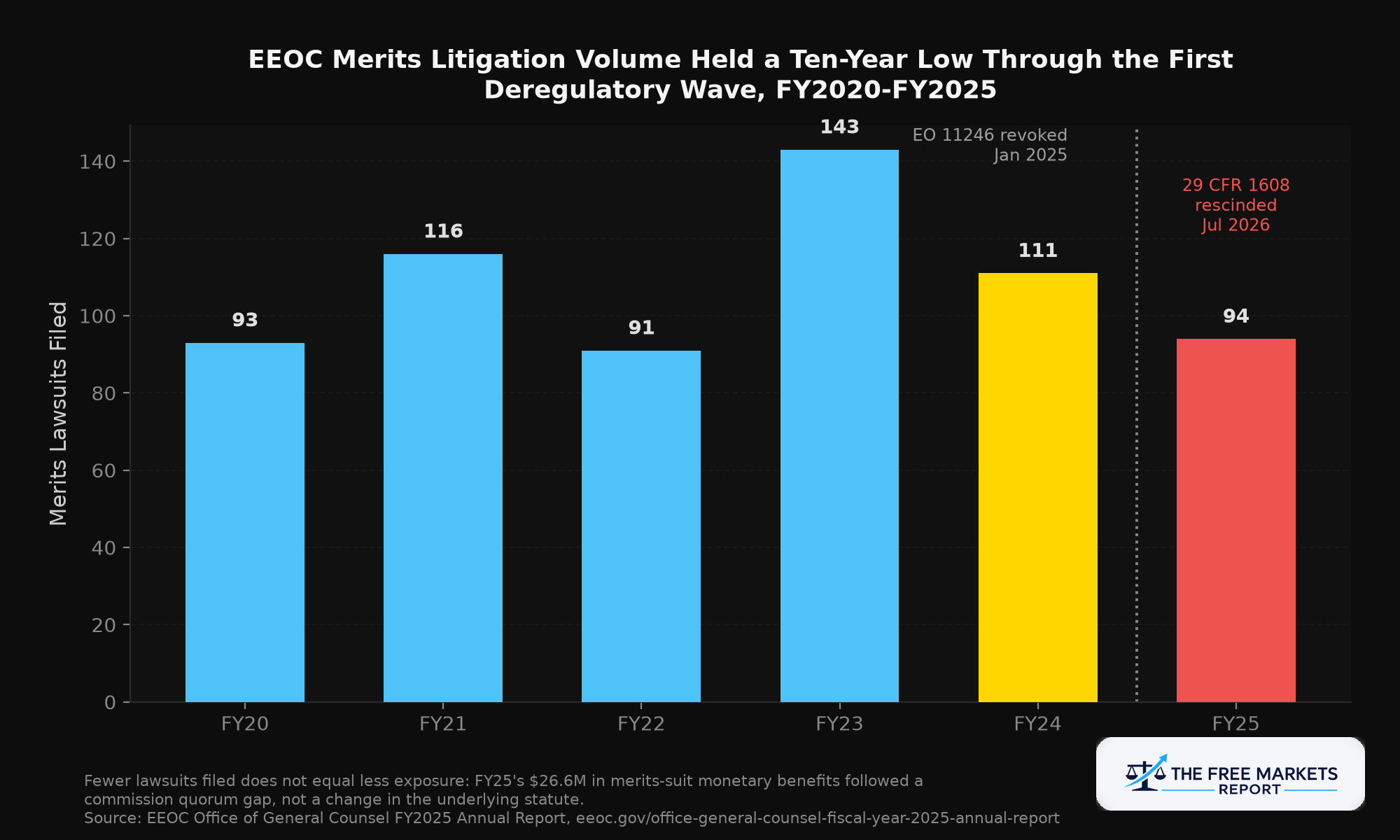

Start with what the EEOC's own litigation data shows happened after that first purge. The agency's Office of General Counsel filed 111 merits lawsuits in fiscal year 2024 and 94 in fiscal year 2025, a ten-year low. That looks like confirmation of the "less enforcement" thesis. But the dollars tell a different story. FY2025 agency-wide monetary relief, combining litigation, conciliation, mediation, and administrative resolutions, reached almost $660 million, the third-highest total in the EEOC's 60-year history, against a $455 million annual budget. Pre-litigation relief alone hit $528 million, a 12.4% increase over FY2024 and the agency's highest such figure on record (EEOC FY2027 Agency Performance Plan).

Fewer lawsuits filed does not equal less exposure: FY25's $26.6M in merits-suit monetary benefits followed a commission quorum gap, not a change in the underlying statute. Source: EEOC Office of General Counsel FY2025 Annual Report.

The mechanical explanation matters too. The EEOC lost commission quorum for much of fiscal year 2025 after two commissioners were terminated, constraining new systemic lawsuit filings independent of the guidance rescissions themselves. Quorum has since been restored. The FY2025 lawsuit drop measures an administrative capacity gap as much as any shift in enforcement appetite.

The Current Parallel: A Ten-Item Agenda, and 1608 Is Only the First to Land

The July 6, 2026 rescission of 29 CFR 1608 is the first of ten items on the EEOC's broader regulatory agenda to reach publication. The agency's stated rationale echoes the EO 11246 logic: the 1979 guidelines are, in the EEOC's words, inconsistent with the statutory language, unsupported by Supreme Court precedent even when issued, obsolete, and silent on four decades of subsequent case law (Federal Register, 91 FR 40879).

The other nine items are where the larger investment story sits. A proposal to rescind the Uniform Guidelines on Employee Selection Procedures interpretive language (RIN 3046-AB43) targets a final rule for November 2026 and would remove the employer validation safe harbor for hiring tests, leaving the statutory disparate-impact framework intact. A separate proposal (RIN 3046-AB37) targets EEO-1 demographic reporting itself, the annual filing required of employers with 100 or more workers and contractors with 50 or more, since 1966, with an NPRM expected in July 2026 and comments open through September (Ogletree Deakins; Reginfo.gov).

That EEO-1 proposal carries an unusually precise cost estimate: the EEOC's own Paperwork Reduction Act notice puts the reporting regime's annual burden at 5,238,467 hours and $273,137,678.30 in direct employer costs. A completed rescission would remove that entire figure from covered employers' books.

Litigation-only recovery is a fraction of total agency relief: FY25's agency-wide monetary relief across all channels reached almost $660M, the third-highest total in EEOC history. Source: EEOC Office of General Counsel FY2025 Annual Report; EEOC FY2027 Agency Performance Plan.

One legal wrinkle narrows this wave's real scope. Rescinding the 1979 guidelines does not amend Title VII, and it does not overrule the Supreme Court decisions that remain controlling law on voluntary affirmative action: United Steelworkers v. Weber (1979) and Johnson v. Transportation Agency of Santa Clara County (1987). Both remain good law. What changes is narrower: employers that built affirmative action plans relying on the rescinded guidance lose the Section 713(b) good-faith statutory defense tied to that reliance, going forward (HRWatchdog, Cal Chamber; Sullivan & Cromwell). A liability-shield removal, not a change to what Title VII prohibits.

The Forward Signal

The base rate this article tests: guidance rescissions that eliminate a specific compliance safe harbor tend to produce a near-term drop in formal enforcement volume, driven partly by administrative capacity constraints rather than the rescission's substance, while dollar-denominated employer exposure, direct compliance costs removed plus residual litigation risk retained, moves independently of that lawsuit count. The 2025 EO 11246 episode showed exactly that: fewer new lawsuits, record dollars recovered through non-litigation channels.

If the EEOC finalizes the EEO-1 rescission, the mechanical effect is a direct compliance-cost reduction worth $273.1 million annually across the 100+ employee employer population, a real tailwind for the broader employer base. It is a more complicated signal for compliance-software vendors whose recurring revenue is partly built on helping employers manage that exact reporting burden.

EEO-1 hours/cost figures are the EEOC's own PRA burden estimate for the reporting regime now proposed for rescission; Paycom revenue is not EEO-1-specific but illustrates the scale of the compliance-software base exposed to any material change in employer reporting mandates. Source: Reginfo.gov OMB Unified Agenda (RIN 3046-AB37); Paycom Software Q4/FY2025 earnings release, SEC EDGAR.

Paycom Software's Form 10-K risk factors are explicit on this point: the company discloses that its government-contractor status subjects it to affirmative action plan obligations, that its Enhanced ACA application exists to generate compliance filings for clients, and that regulatory changes decreasing demand for compliance-related applications could decrease its revenues and net income (Paycom 10-K digest, Stock Titan). Paycom does not break out compliance-application revenue separately, so this is a risk-factor category, not a quantified exposure. The base it sits on is not small: Paycom's total revenue grew from $1,694 million in fiscal 2023 to $2,051.7 million in fiscal 2025 (Paycom Q4/FY2025 earnings release, SEC EDGAR).

Investment Idea: Paycom Software (PAYC)

Thesis type: Second-order, contrarian reversal watch

Deregulatory catalyst: The July 6, 2026 rescission of 29 CFR 1608, and the pending RIN 3046-AB37 proposal to rescind EEO-1 demographic reporting, both reduce the compliance-reporting burden HR software vendors have historically monetized as a recurring-revenue feature.

Current price: Not independently re-verified against a live market quote in this session; the financial data below is anchored to Paycom's SEC-filed FY2025 results rather than a same-day quote.

Key financial data: Full-year 2025 total revenue of $2,051.7 million (up 9.0% year over year), recurring and other revenue of $1,938.7 million (94.5% of total revenue), GAAP net income of $453.4 million, per Paycom's SEC-filed fourth quarter and full-year 2025 earnings release (SEC EDGAR).

Regulatory constraint removed: None yet, directly, for Paycom's own compliance modules. What has been removed so far is a liability-shield change, not a reporting-mandate change. EEO-1 filing, the mandate most relevant to compliance software revenue, remains only at the proposal stage (RIN 3046-AB37, NPRM expected July 2026).

Bull case: Paycom's recurring revenue has compounded at high single to low double digits for three straight fiscal years on a broadening applications suite, of which compliance tools are one feature among many, alongside talent acquisition, time and labor management, and payroll. A full EEO-1 rescission would remove one line item within one category, not a structural pillar of the recurring-revenue base, and it has no published effective date yet.

Bear case: This is a documented risk-factor line, not a hypothetical one. Paycom's own 10-K states that regulatory changes decreasing demand for compliance-related applications could decrease its revenues and net income. If the EEOC's ten-item agenda continues removing reporting mandates over the next 12 to 18 months, that is a real, likely modest, headwind to a discrete slice of Paycom's stack, one the company has not sized in dollar terms. The uncertainty itself is the risk.

What to watch: The EEOC's EEO-1 NPRM (RIN 3046-AB37), expected July 2026 with comments through September 2026, and whether any final rule sets an effective date, a phase-out period, or preserves a narrower reporting requirement.

Time horizon: 12 to 24 months, tied to the EEO-1 rulemaking timeline rather than the July 6 guidance rescission itself.

The Principle Close

The pattern that matters isn't whether one guidance document survives. Guidance rescissions and reporting-mandate rescissions are not the same event, even from the same agency in the same year. The 1979 guidelines rescission changes a liability defense. The EEO-1 proposal, if finalized, changes a cost structure. Investors pricing "deregulation" as one undifferentiated signal risk missing which mechanism is actually moving, and for whom. The EO 11246 episode already showed headline enforcement volume and actual dollar exposure moving in opposite directions in the same twelve months. That is the base rate this rescission wave should be measured against, not the assumption that fewer guidance documents automatically means less compliance spending across the board.

Footnotes

- Federal Register, "Guidelines on Affirmative Action Appropriate Under Title VII of the Civil Rights Act of 1964," RIN 3046-AB39, 91 FR 40879, effective July 6, 2026: govinfo.gov

- Ogletree Deakins, "The EEOC's Regulatory Agenda: 10 Signs of Intent": ogletree.com

- Reginfo.gov, OMB/OIRA Unified Agenda entry for RIN 3046-AB37 (EEO-1 reporting rescission proposal): reginfo.gov

- The White House, Executive Order 14173, "Ending Illegal Discrimination and Restoring Merit-Based Opportunity," January 21, 2025: whitehouse.gov

- EEOC Office of General Counsel, Fiscal Year 2025 Annual Report: eeoc.gov

- EEOC, FY 2027 Agency Performance Plan and FY 2025 Agency Performance Report: eeoc.gov

- HRWatchdog, California Chamber of Commerce, "EEOC Removes Decades-Old Affirmative Action Guidance": hrwatchdog.calchamber.com

- Sullivan & Cromwell, "EEOC Rescinds Long-standing Affirmative Action Guidance": sullcrom.com

- Paycom Software, Inc., Fourth Quarter and Full Year 2025 Results, SEC EDGAR Exhibit 99.1: sec.gov

- Paycom Software, Inc., Form 10-K for fiscal year 2025, filed February 19, 2026, summarized via Stock Titan SEC filing digest: stocktitan.net

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.