Washington Chose Talks Over Tariffs on Jets. RTX Still Booked the Cost.

Commerce found aerospace imports risk national security, then Trump chose negotiation over tariffs, with a 180-day clock and tariff authority explicitly reserved.

Key Highlights

- On July 9, 2026, President Trump signed a Section 232 proclamation on commercial aircraft, jet engines, and parts, directing Commerce and USTR to negotiate with trading partners rather than impose immediate tariffs (White House proclamation).

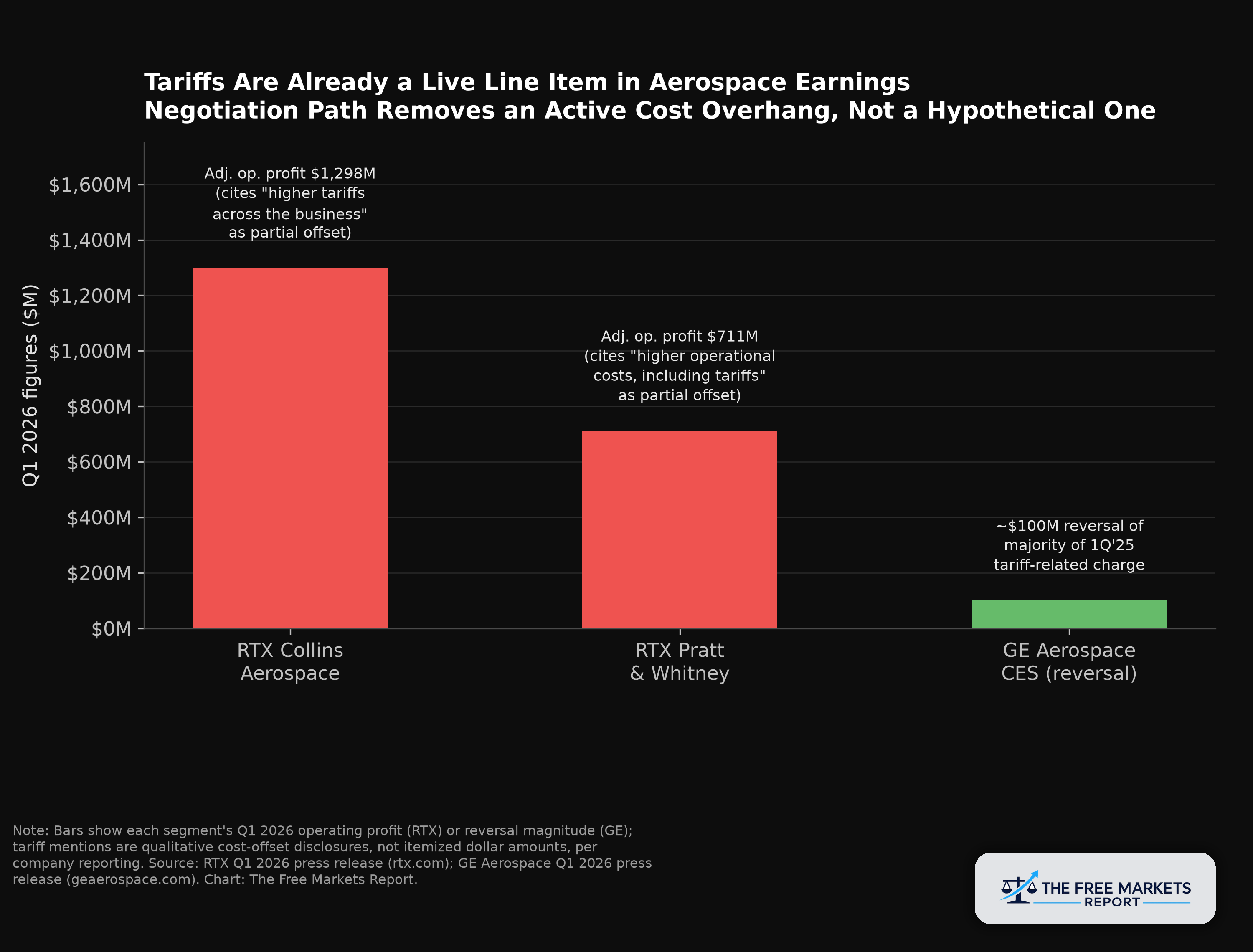

- The underlying Section 232 investigation opened May 1, 2025, and Commerce's completed report found the U.S. aircraft industry "too reliant on foreign supply chains," raising national security concerns, even as it recommended against new tariffs (Reuters; Federal Register).

- The proclamation gives negotiators 180 days, until roughly January 5, 2027, to report progress, and explicitly reserves the president's authority to impose tariffs later if talks stall (White House proclamation).

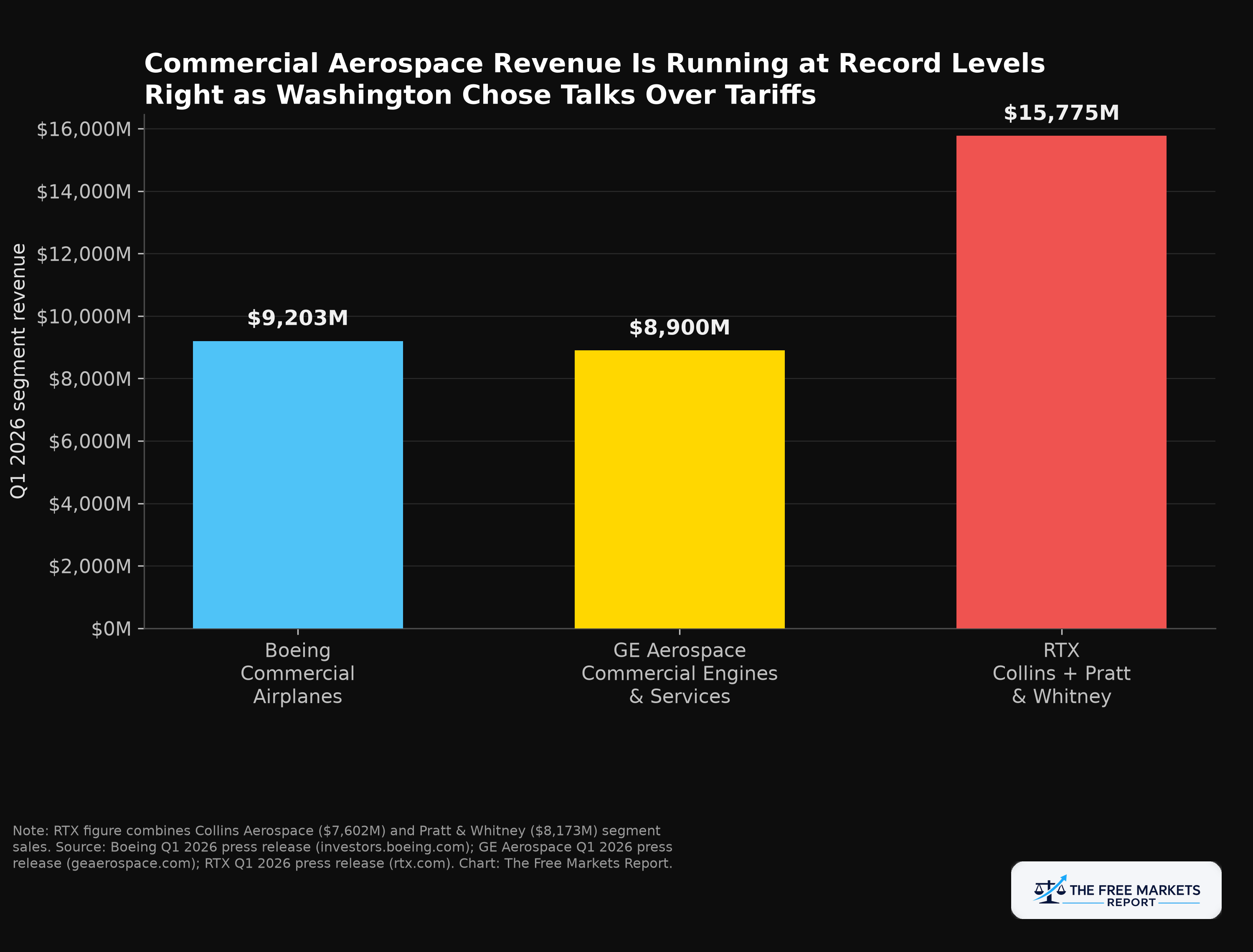

- RTX (RTX) already disclosed "higher tariffs across the business" as a partial profit offset at Collins Aerospace and "higher operational costs, including tariffs" at Pratt & Whitney in its Q1 2026 results, proof the cost is live, not hypothetical (RTX Q1 2026 press release).

- The tariff-free regime under the 1979 Civil Aircraft Agreement has underwritten a roughly $75 billion annual U.S. aerospace trade surplus, the exact surplus this proclamation is aimed at protecting rather than disrupting (Reuters; Aerospace Industries Association).

On July 9, the Commerce Department finished a year-long national security investigation into imported aircraft, jet engines, and parts, and then recommended the government do almost nothing about it. No new tariffs. No import quotas. Just an instruction to keep talking, with a deadline attached.¹ It is a government that found a real problem, chose not to use its biggest tool to fix it yet, and told the industry exactly how long that restraint will last.

A Wartime Statute, a Negotiated Truce

Section 232 of the Trade Expansion Act of 1962 lets the president restrict imports that threaten national security. Commerce opened its investigation into aircraft, jet engines, and parts on May 1, 2025, under docket BIS-2025-0027.² Its finished report concluded the U.S. aircraft industry "is facing challenges to adequately meet economic and national security demands," citing foreign competitive practices and overreliance on foreign imports.³

Commerce found a real constraint and then chose not to act on it immediately. Secretary of Commerce Howard Lutnick recommended no immediate tariffs. Instead, President Trump directed Commerce and USTR to jointly negotiate with foreign trading partners and report back within 180 days, a deadline around January 5, 2027.⁴ The proclamation preserves the president's authority under 19 U.S.C. § 1862(c)(3)(A) to impose tariffs later "depending on the status or outcome" of negotiations.⁵

This is the second time in a year aerospace tariffs have been threatened, then pulled back. The sector briefly saw tariffs imposed in 2025 before a September 25, 2025 Federal Register notice retroactively exempted aircraft and parts, effective September 1, 2025, after heavy aviation-sector lobbying.⁶ The pattern is now two-for-two: threaten, then negotiate an exemption. A skeptical reader should ask whether the third time breaks that pattern, and that is exactly what the 180-day clock now measures.

Why This Wasn't a Free Pass

The reason Commerce pulled back is the same reason the investigation happened at all: the U.S. aerospace industry runs one of the country's best trade numbers, and nobody wants to be the one who broke it. Airplanes and parts have operated tariff-free since the 1979 Civil Aircraft Agreement, a framework the Aerospace Industries Association credits with a nearly $75 billion trade surplus and 2,100%-plus export growth over 45 years.⁷ Delta Air Lines (DAL) and Airbus Americas both warned in 2025 that aircraft tariffs would raise ticket prices and threaten U.S. planemaking.⁸ Barnes, Richardson & Colburn's trade-law analysis was blunt: the administration reserved the right to act later if talks fail, but for now importers "let out a final sigh of relief."⁹

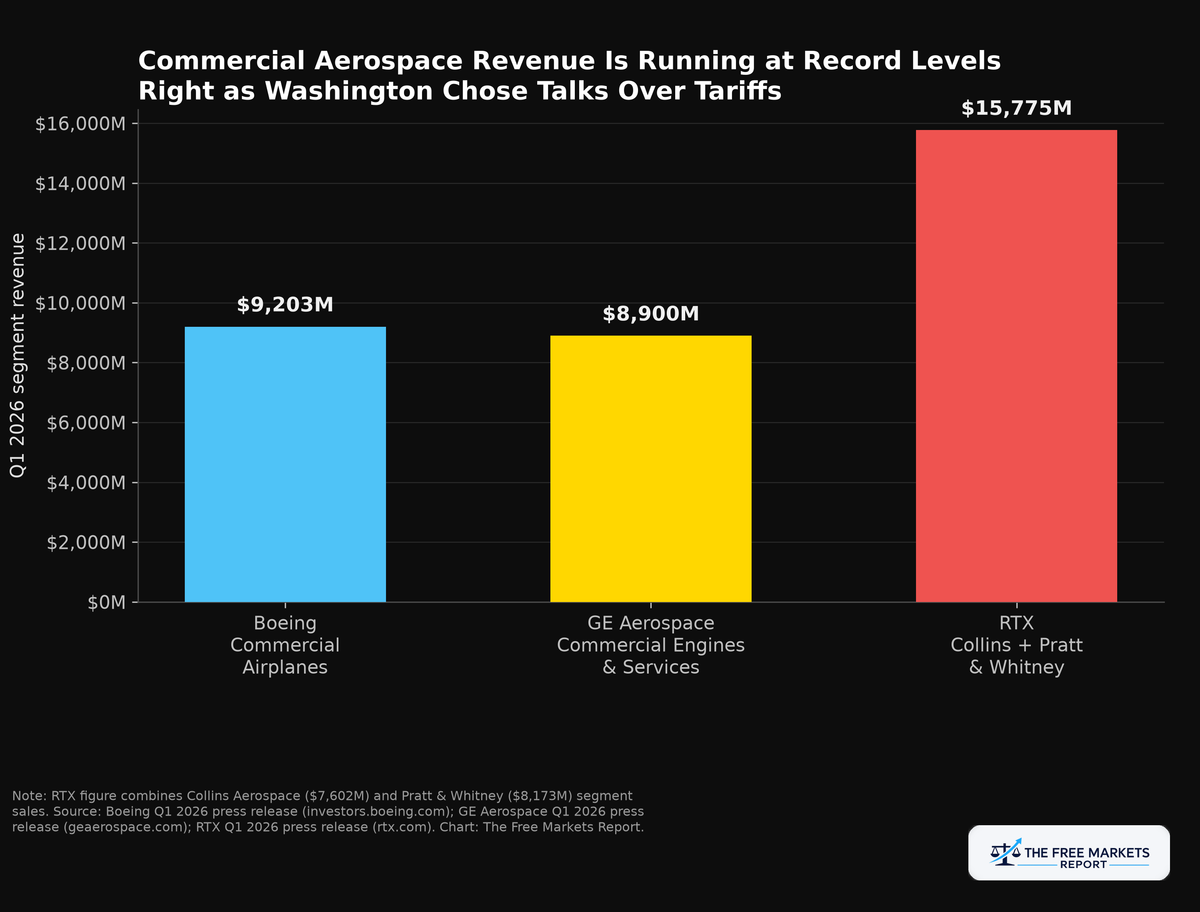

The negotiation path is not the same as no cost. Boeing (BA), GE Aerospace (GE), and RTX (RTX) already operate inside a partially tariffed environment, and their Q1 2026 disclosures show it. Boeing's Commercial Airplanes segment generated $9,203 million in revenue, up 13%, against a record $695 billion backlog including over $576 billion in commercial aircraft.¹⁰ GE Aerospace's Commercial Engines & Services segment posted $8,900 million, up 34%, against a $170 billion services backlog.¹¹ RTX reported $22.1 billion in total sales, up 9%, with a $271 billion combined backlog.¹² So what does that add up to: a sector at record order volume, with a live tariff overhang still sitting on top of it.

GE Aerospace's Q1 2026 reversal of roughly $100 million in prior tariff charges is the single most concrete data point in this story.¹³ It is a real cost already unwinding as the tariff picture eased over the past year, before this proclamation even existed, and the same accounting mechanism is available to RTX if negotiations succeed.

The Bear Case

The strongest argument against this thesis is that the proclamation changes nothing that wasn't already true. Aircraft and parts have operated under a negotiated, largely tariff-free arrangement with the EU, UK, and other partners since 2025, and this proclamation mostly formalizes that status quo.¹⁴ On that reading, RTX, Boeing, and GE Aerospace were already pricing in the negotiated outcome, with limited incremental catalyst beyond a bad outcome being avoided.

The second, more serious risk is the reserved authority itself. This is a 180-day probationary period, not permanent relief, and the same statute is currently imposing duties of up to 50% on imported steel, aluminum, and copper under a separate June 1, 2026 proclamation, tariffs that remain in effect through at least 2027.¹⁵ Aerospace's long switching costs and multi-year certification cycles mean a stalled negotiation could reintroduce cost uncertainty suppliers cannot hedge quickly. Commerce's own finding, that foreign-supply dependence is a national security concern, does not disappear just because tariffs did not follow immediately.¹⁶

Falsification condition: if the 180-day update due around January 5, 2027 results in no substantive agreement, or if the administration invokes tariff authority under 19 U.S.C. § 1862(c)(3)(A) before that date, the negotiation-path thesis for aerospace suppliers is wrong, and the tariff-cost drag visible in RTX's Q1 2026 segment disclosures should be expected to reappear and widen rather than fade.

Investment Idea

INVESTMENT IDEA: RTX Corporation (RTX)

- Thesis type: Second-order beneficiary

- Regulatory catalyst: July 9, 2026 Section 232 proclamation directing negotiation over aerospace tariffs, with a 180-day update deadline and reserved future tariff authority

- Key financial data: Q1 2026 sales of $22.1 billion (up 9%); Collins Aerospace adjusted operating profit of $1,298 million (up 6%) and Pratt & Whitney adjusted operating profit of $711 million (up 21%); $271 billion combined backlog; FY26 guidance of $92.5-93.5 billion adjusted sales and $6.70-6.90 adjusted EPS

- Regulatory constraint removed: Both Collins Aerospace and Pratt & Whitney explicitly cited tariffs as a partial offset to Q1 2026 profit growth; a negotiated outcome removes a documented, currently active drag on segment margins rather than a theoretical one

- Bull case: If the 180-day window produces durable agreements like the 2025 EU and UK frameworks, RTX's disclosed tariff offsets have room to shrink further, the same mechanism GE Aerospace already showed with its roughly $100 million charge reversal

- Bear case: This is a 180-day probationary period, not permanent relief; the administration explicitly reserved tariff authority if talks stall, and RTX's aftermarket-heavy mix means renewed tariff action would hit a business already carrying elevated backlog-driven capital needs

- What to watch: Commerce and USTR's mandated update, due around January 5, 2027, and RTX's quarterly language on tariffs as a profit offset, which should shrink if talks succeed and widen if they do not

- Time horizon: Event-driven, 6-18 months

What to Watch Next

The next concrete checkpoint is not a market event. It is a government deadline: Commerce and USTR's mandated report on negotiation progress, due within 180 days of the July 9 proclamation. Until then, the highest-signal data keeps coming from the companies themselves. Every RTX and GE Aerospace quarterly release includes explicit language on whether tariffs are a growing or shrinking offset to profit, a real-time gauge of the negotiation path running months ahead of Washington's own update.

The lesson here is not that aerospace escaped tariffs. It is that aerospace is currently paying a measurable, disclosed tariff cost while the government negotiates a better outcome on a clock. A negotiated truce is not a resolved dispute, and the gap between the two is exactly what this trade will close or widen over the next six months.

Footnotes

- White House, "Adjusting Imports of Commercial Aircraft, Jet Engines, and Aircraft and Engine Parts Into the United States," July 9, 2026. https://www.whitehouse.gov/presidential-actions/2026/07/adjusting-imports-of-commercial-aircraft-jet-engines-and-aircraft-and-engine-parts-into-the-united-states/

- Federal Register, Bureau of Industry and Security notice, Docket No. 250509-0082, May 13, 2025. https://www.federalregister.gov/documents/full_text/xml/2025/05/13/2025-08500.xml

- Barnes, Richardson & Colburn, "White House Declines Section 232 Tariff on Aerospace Articles," July 10, 2026. https://www.barnesrichardson.com/white-house-declines-section-232-tariff-on-aerospace-articles

- White House proclamation, July 9, 2026 (see note 1), paragraphs 9 and 11.

- White House proclamation, July 9, 2026 (see note 1), paragraphs 11-12.

- Greenberg Traurig LLP, "US-EU Trade Deal Restores Zero Tariffs on Aircraft and Aircraft Parts," October 10, 2025. https://www.gtlaw.com/en/insights/2025/10/us-eu-trade-deal-restores-zero-tariffs-on-aircraft-and-aircraft-parts

- Reuters, "US ends probe into imported airplanes, parts without seeking new tariffs," July 9, 2026. https://www.reuters.com/business/aerospace-defense/us-ends-probe-into-imported-airplanes-parts-without-seeking-new-tariffs-2026-07-09/; Aerospace Industries Association, "AIA Releases White Paper Highlighting American Leadership in Aerospace Trade," May 1, 2025. https://www.aia-aerospace.org/news/aia-releases-white-paper-highlighting-american-leadership-in-aerospace-trade-thanks-to-agreement-on-trade-in-civil-aircraft/

- Reuters, July 9, 2026 (see note 7).

- Barnes, Richardson & Colburn, July 10, 2026 (see note 3).

- The Boeing Company, "Boeing Reports First Quarter Results," April 22, 2026. https://investors.boeing.com/investors/news/press-release-details/2026/Boeing-Reports-First-Quarter-Results/default.aspx

- GE Aerospace, "GE Aerospace Announces First Quarter 2026 Results," April 21, 2026. https://www.geaerospace.com/news/press-releases/ge-aerospace-announces-first-quarter-2026-results

- RTX Corporation, "RTX Reports Q1 2026 Results," April 21, 2026. https://www.rtx.com/news/news-center/2026/04/21/rtx-reports-q1-2026-results-

- GE Aerospace, April 21, 2026 (see note 11).

- Greenberg Traurig LLP, October 10, 2025 (see note 6).

- The White House, "Further Adjusting the Tariff Regimes for Imports of Aluminum, Steel, and Copper Into the United States," June 1, 2026. https://www.whitehouse.gov/presidential-actions/2026/06/further-adjusting-the-tariff-regimes-for-imports-of-aluminum-steel-and-copper-into-the-united-states/

- White House proclamation, July 9, 2026 (see note 1), paragraph 6; Reuters, July 9, 2026 (see note 7).

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.