The SEC Wants to Make IPOs Great Again. Here's Who Cashes the Check.

Chairman Atkins' 2026 regulatory agenda and Monday's IPO roundtable target the 50 percent collapse in U.S. public companies. The listing venues stand to benefit first.

Chairman Atkins' 2026 regulatory agenda and Monday's IPO roundtable target the 50 percent collapse in U.S. public companies. The listing venues stand to benefit first.

Key Highlights

- SEC Chairman Paul Atkins released his Statement on the 2026 Regulatory Agenda on July 7, 2026, prioritizing reduced disclosure burdens and reversing "the decline of public companies" under his self-described "Make IPOs Great Again" mission.[1]

- The SEC's Office of the Advocate for Small Business Capital Formation and Division of Corporation Finance will co-host a livestreamed roundtable on Monday, July 13, 2026 at 2:00 p.m. ET, scheduled to re-examine the IPO process and public-market access framework.[2]

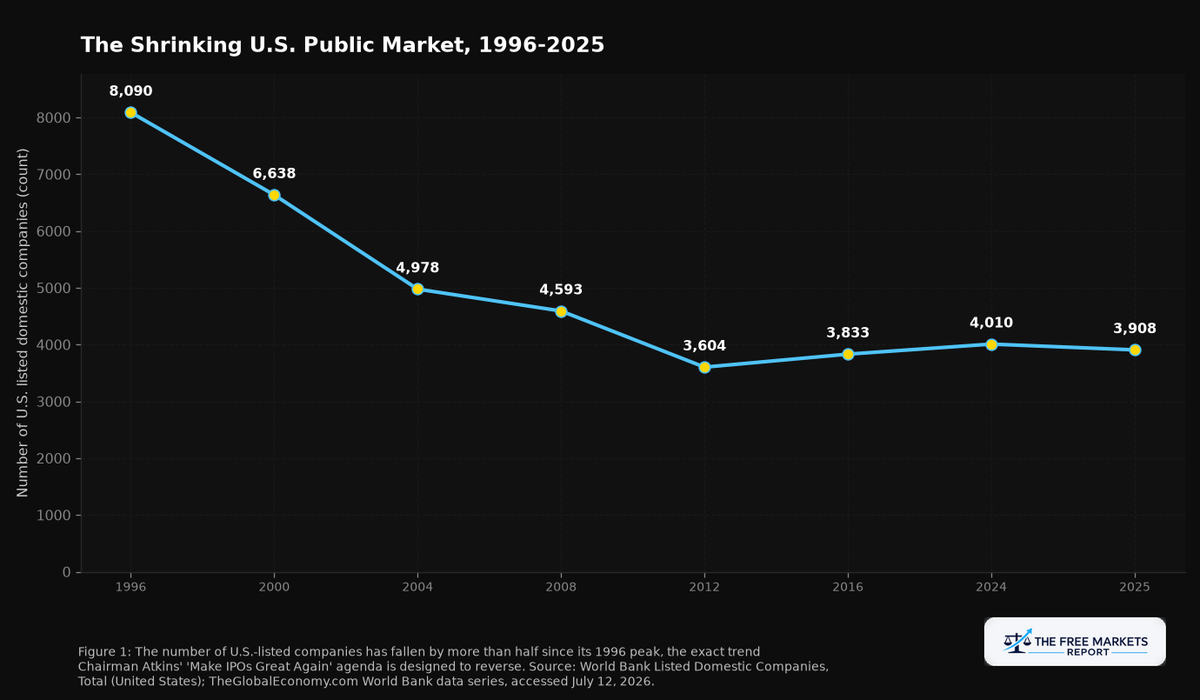

- The number of U.S.-listed domestic companies has fallen from a peak of roughly 8,090 in 1996 to 3,908 in 2025, a decline of more than 50 percent.[3]

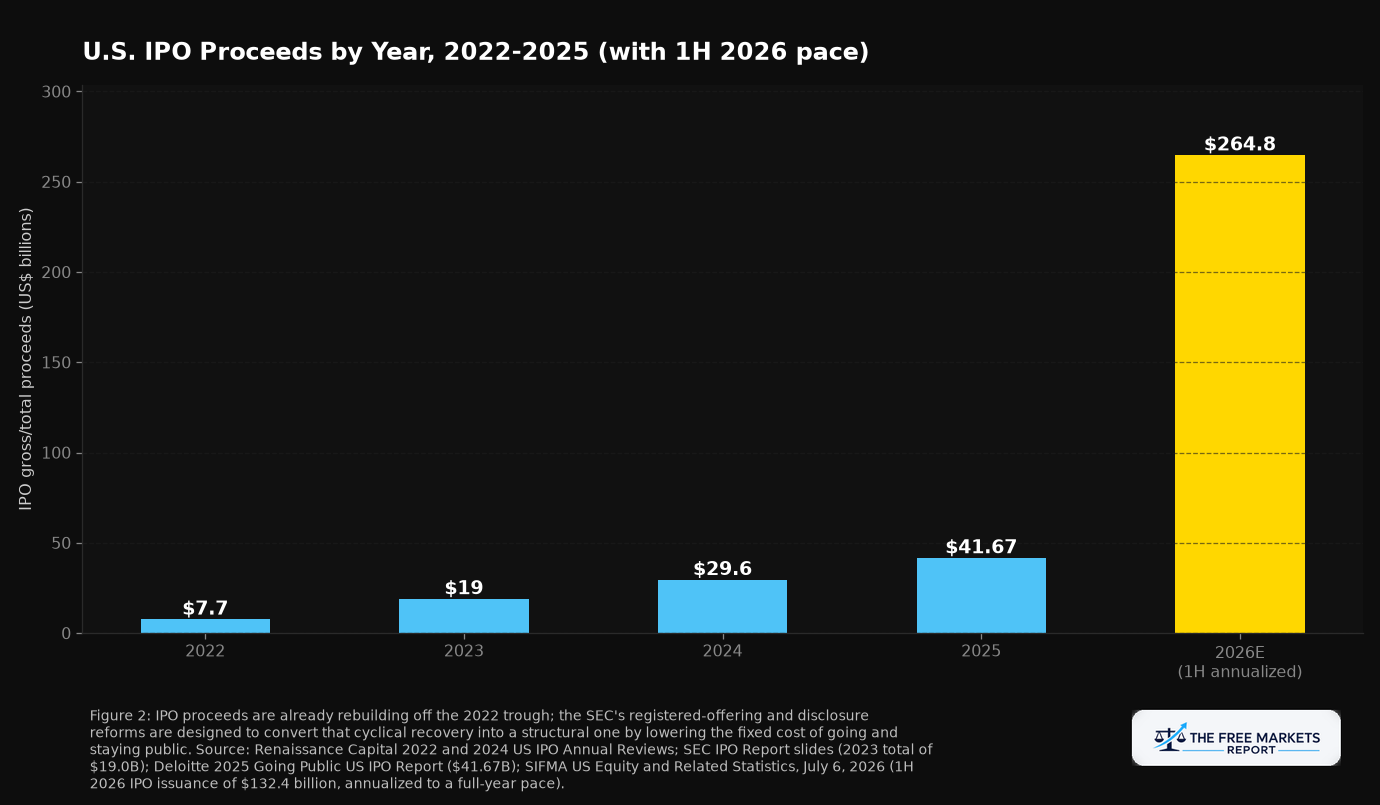

- Intercontinental Exchange (ICE), owner of the New York Stock Exchange, reported Q1 2026 Exchanges segment revenue of $2.47 billion, its largest and fastest-growing segment, and total company revenue of $3.666 billion for the quarter ended March 31, 2026.[4]

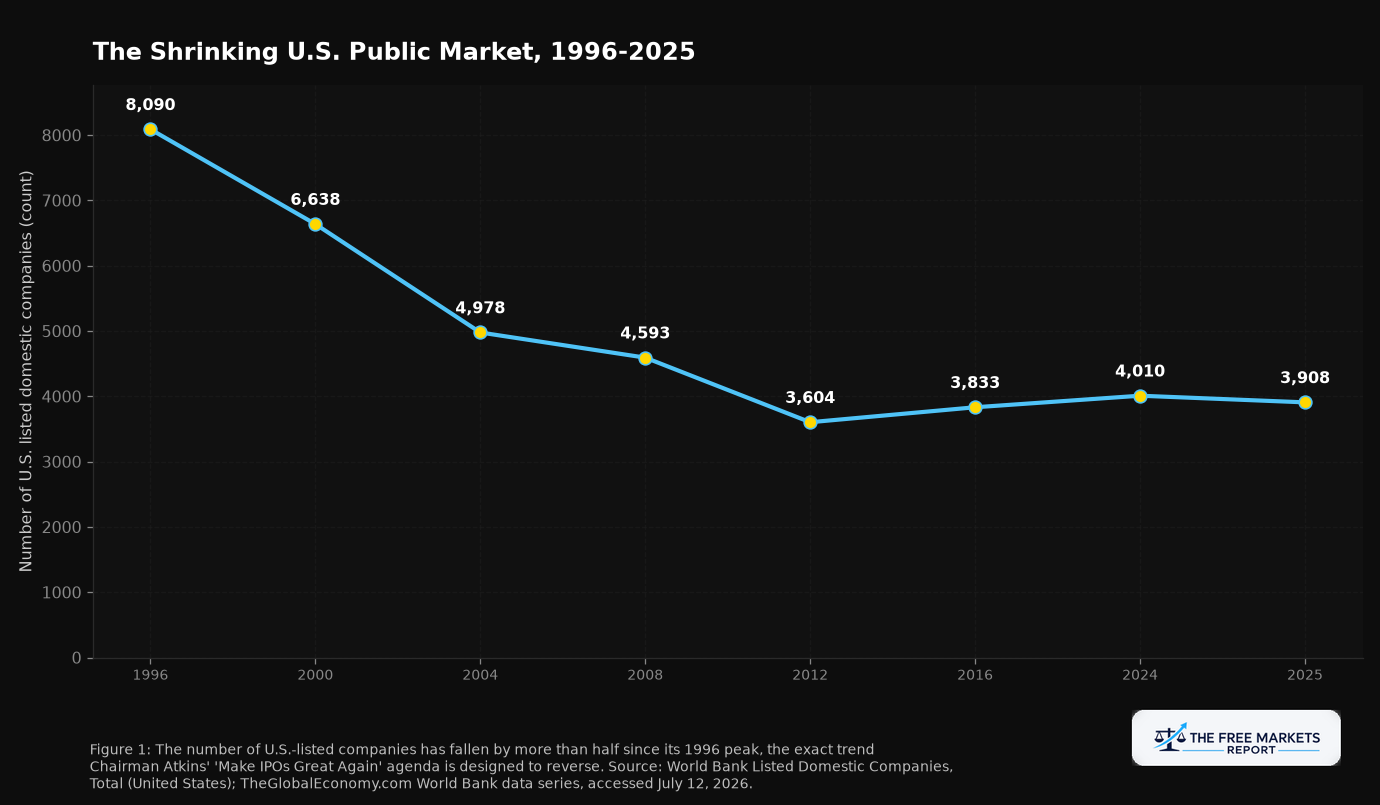

- U.S. IPO proceeds have already rebuilt from a 2022 trough of $7.7 billion to $41.67 billion in 2025, with 1H 2026 IPO issuance of $132.4 billion signaling further acceleration before any of the SEC's proposed reforms are finalized.[5][6]

The U.S. public market has been shrinking for three decades, and the SEC's chairman just put a number on his ambition to reverse it: "reversing the decline of public companies and revitalizing our public markets to Make IPOs Great Again." That is the stated organizing purpose of the SEC's entire 2026 rulemaking agenda, published July 7, and it is about to get a public workshop. On Monday, July 13, the SEC's Office of the Advocate for Small Business Capital Formation and the Division of Corporation Finance are scheduled to co-host a livestreamed roundtable to reassess how companies of every size actually get onto an exchange and stay there.[1][2] Neither event has happened yet as of this writing; both are dated actions on the regulatory calendar, not history. Together they describe a coordinated attempt to lower the cost of being public at exactly the moment the IPO market is showing signs of a cyclical rebound. The question for investors is not whether that policy direction is good or bad in the abstract. It is who owns the toll booth if it works.

Half the Public Companies, Same Country

The number of domestic companies listed on U.S. exchanges peaked at approximately 8,090 in 1996 and had fallen to 3,908 by the end of 2025, according to World Bank data compiled by TheGlobalEconomy.com, a decline of more than 50 percent even as the U.S. economy roughly tripled in nominal size over the same period.[3] Chairman Atkins made the connection to real people explicit in his statement: "Every IPO is an invitation to workers and savers to participate in the prosperity of the next generation of American enterprise. When fewer companies go public, fewer investors receive that invitation."[1] The core argument of the 2026 agenda is that the compliance burden of being a public company, not a shortage of good private companies, is what emptied out the public market.

That diagnosis is not new to July. The SEC's May 19, 2026 proposal, Registered Offering Reform under Release No. 33-11418, is described by the agency itself as the foundation for the chairman's agenda to "Make IPOs Great Again."[7] It would eliminate Form S-3's 12-month seasoning requirement and $75 million public-float threshold, raise the large-accelerated-filer threshold from $700 million to $2 billion in market cap, and extend scaled disclosure accommodations to roughly 81 percent of current public companies for a minimum of five years after IPO.[7] July 7's agenda statement folds that proposal into a broader mission. July 13's roundtable is where practitioners test it in public before any of it becomes a final rule.

The Mechanism: Lower the Fixed Cost, Widen the Funnel

A company's decision to go public is, in large part, a comparison of the fixed annual cost of being public against the capital-access benefit of a listed equity currency. When disclosure and internal-control attestation requirements calibrated for the largest companies get applied nearly uniformly down the market-cap scale, the fixed-cost side of that ledger gets heavier every year, disproportionately for smaller issuers. The May 2026 proposal's filer-status overhaul targets that directly: non-accelerated filers would be exempt from the auditor attestation requirement on internal controls, and small non-accelerated filers would get an additional 30 days to file 10-Ks and five days to file 10-Qs.[7]

U.S. IPO proceeds bottomed at $7.7 billion in 2022, the slowest year by proceeds in more than three decades of Renaissance Capital's tracking, then rebuilt to roughly $19.0 billion in 2023, $29.6 billion in 2024, and $41.67 billion in 2025.[5][8][9] That recovery was already underway before Atkins' agenda existed in its current form. SIFMA separately reports 1H 2026 IPO issuance reached $132.4 billion, up 685.6 percent year over year, a figure driven heavily by a handful of large deals but directionally consistent with a market reopening on its own cyclical timeline.[6] The SEC's deregulatory push is not creating a rebound from nothing; it is attempting to convert an existing cyclical recovery into a structural one that survives the next rate cycle.

Who Collects the Toll Regardless of Which Company Lists

A reopening IPO market has an obvious set of second-order beneficiaries that don't require picking the next winning listing: the exchanges themselves. Every new listing, and every existing company that stays public longer under a lighter compliance load, generates recurring listing fees, data fees, and trading volume for whichever exchange group hosts it. Intercontinental Exchange (ICE), the parent of the New York Stock Exchange, sits at the center of that toll structure almost regardless of which specific company benefits from the SEC's reforms.

ICE reported total consolidated revenue of $3.666 billion and consolidated net income of $1.432 billion for the fiscal quarter ended March 31, 2026, with operating profit of $1.665 billion.[4] Broken out by segment, ICE's Exchanges business, which houses NYSE listings alongside its energy, financial, and agricultural futures franchises, generated $2.47 billion of that quarter's revenue, more than the Fixed Income and Data Services ($657 million) and Mortgage Technology ($539 million) segments combined, with Exchanges segment operating income of $1.403 billion.[10] ICE shares traded at $135.26 as of the July 10, 2026 close, giving the company a market capitalization of approximately $76.5 billion and a trailing price-to-earnings ratio near 17.8.[11] The Exchanges segment is not a side business at ICE. It is the largest, highest-margin engine in the company, and the one most directly exposed to more companies choosing to list and stay listed.

Reading the SEC's Own Track Record Honestly

The textbook expectation is that a deregulatory push aimed at "reversing the decline of public companies" should be a straightforward tailwind for exchange operators. But the SEC's own history complicates that clean story. The agency has pursued variations of this fix for over a decade: the JOBS Act's original IPO on-ramp dates to 2012, and the number of listed companies kept falling anyway, from roughly 5,216 in 2003 to 3,604 by 2012, well after that reform was in place.[3] Rulemaking that reduces disclosure friction does not automatically reverse a structural shift toward private capital and M&A-driven consolidation, forces arguably more powerful than any single compliance-cost line item.

The May 2026 proposal's comment period does not close until late July 2026, and outside counsel broadly expect final rules, if adopted at all, no earlier than 2027 and potentially altered from the current draft.[7] The July 13 roundtable is explicitly a listening session, not a rulemaking vote.[2] ICE's own Q1 2026 growth was driven primarily by higher futures and options trading volumes tied to macro and geopolitical volatility, not by a surge in new listings.[4][10] Attributing that quarter's strength to the deregulatory agenda would overstate a connection the data does not yet support; ICE's listings franchise stands to benefit if the pipeline materializes at scale, not because it already has.

Bear Case

The explicit falsification condition: if full-year 2026 and 2027 U.S. IPO proceeds and listing counts fail to sustain the acceleration implied by the $132.4 billion first-half 2026 pace once trading-driven volatility normalizes, or if the SEC's Registered Offering Reform and companion filer-status proposals are withdrawn, substantially narrowed, or stayed by litigation before taking effect, the structural case for exchange operators as IPO-reform beneficiaries would be materially weakened.[6][7] The 2012 JOBS Act on-ramp is a documented instance of a structurally similar deregulatory thesis underdelivering: the listed-company count kept falling for years afterward.[3] A sustained higher-rate environment that keeps private capital competitive with public listings would blunt the mechanism regardless of what the SEC does on disclosure.

Investment Idea

INVESTMENT IDEA: Intercontinental Exchange (ICE)

Thesis type: Second-order beneficiary

Deregulatory catalyst: SEC Chairman Atkins' July 7, 2026 Statement on the 2026 Regulatory Agenda and the "Make IPOs Great Again" reform package, plus the July 13, 2026 SEC roundtable on modernizing the IPO process.[1][2][7]

Current price: $135.26 as of the July 10, 2026 close; market capitalization approximately $76.5 billion; trailing price-to-earnings ratio near 17.8.[11]

Key financial data: Q1 2026 total revenue of $3.666 billion and net income of $1.432 billion; Exchanges segment revenue of $2.47 billion, the largest of ICE's three reporting segments.[4][10]

Regulatory constraint removed: The SEC's proposed elimination of Form S-3's seasoning and float requirements, the proposed increase in the large-accelerated-filer threshold from $700 million to $2 billion, and the proposed exemption of most non-accelerated filers from internal-control auditor attestation.[7]

Bull case: If the reforms and the ongoing cyclical IPO recovery combine to sustainably increase both new listings and how long companies stay public, exchange operators like ICE capture the resulting fees and trading volume with minimal incremental cost, given the Exchanges segment's already-high operating margin.

Bear case: The IPO recovery predates and is largely independent of the 2026 agenda. Final SEC rules are unlikely before 2027 and may be narrowed or challenged, and a sustained higher-rate environment could keep private capital competitive with public listings regardless of disclosure relief.[6][7]

What to watch: Full-year 2026 IPO proceeds against the $132.4 billion first-half pace, and whether Release No. 33-11418 advances to final adoption after the July 27, 2026 comment deadline.[6][7]

Time horizon: 18 to 36 months

The Financial Mechanics, Not a Forecast

None of this is a case for buying anything. It is a case for watching a specific, dated catalyst. Chairman Atkins has stated, on the record, that reversing the 30-year decline in public companies is a named priority of his agency, and the July 13 roundtable is the next scheduled step in turning that priority into rule text.[1][2] The financial mechanics, sourced to ICE's own SEC filings, show a listings-and-data franchise that is already the largest segment in the company and structurally positioned to capture more of the toll if the pipeline widens.[4][10] The deregulatory catalyst creates a structural tailwind for exchange economics. Whether that tailwind is large enough to matter against three decades of consolidation pressure is what the next several quarters of IPO data, not this week's roundtable, will show.

The decline in U.S. public companies was thirty years in the making. The SEC's stated fix will be measured in quarters, not headlines. Watch the proceeds data, not the press release.

Footnotes

[1] Paul S. Atkins, "Statement on the 2026 Regulatory Agenda," U.S. Securities and Exchange Commission, July 7, 2026. https://www.sec.gov/newsroom/speeches-statements/atkins-statement-2026-regulatory-agenda-070726

[2] "SEC to Host Virtual Roundtable on Modernizing IPOs and Expanding Access to Public Markets," U.S. Securities and Exchange Commission, Press Release 2026-65, July 8, 2026. https://www.sec.gov/newsroom/press-releases/2026-65-sec-host-virtual-roundtable-modernizing-ipos-expanding-access-public-markets

[3] "USA Listed companies," TheGlobalEconomy.com, World Bank data series, accessed July 12, 2026 (1996 peak of 8,090; 2025 value of 3,908; 2003 value of 5,216; 2012 value of 3,604). https://www.theglobaleconomy.com/USA/Listed_companies/

[4] Intercontinental Exchange, Inc., quarterly income statement data for the fiscal quarter ended March 31, 2026, U.S. Securities and Exchange Commission EDGAR, CIK 0001571949, filed April 30, 2026. https://www.sec.gov/edgar/browse/index.html?cik=1571949

[5] "US IPO Market: 2024 Annual Review," Renaissance Capital, 2024 ($29.6 billion in 2024 IPO proceeds). https://www.renaissancecapital.com/review/2024USReview_Public.pdf

[6] "US Equity and Related Statistics," SIFMA, July 6, 2026 (YTD 2026 IPO issuance of $132.4 billion, up 685.6 percent year over year). https://www.sifma.org/research/statistics/us-equity-and-related-securities-statistics

[7] "SEC Proposes Transformative Reforms to Help Public Companies Conduct Registered Offerings and Simplify Reporting Requirements," U.S. Securities and Exchange Commission, Press Release 2026-46, May 19, 2026. https://www.sec.gov/newsroom/press-releases/2026-46-sec-proposes-transformative-reforms-help-public-companies-conduct-registered-offerings-simplify

[8] "US IPO Market: 2022 Annual Review," Renaissance Capital, 2022 ($7.7 billion in 2022 IPO proceeds, the slowest year by proceeds in over three decades). https://www.renaissancecapital.com/review/2022USReview_Press.pdf

[9] "IPO Report" slides, U.S. Securities and Exchange Commission (2023 total gross IPO proceeds of $19.0 billion, up 144 percent from $7.8 billion in 2022). https://www.sec.gov/files/ipo-report-slides-022024-bjohnson.pdf

[10] Intercontinental Exchange, Inc., segment revenue and operating income data for the fiscal quarter ended March 31, 2026 (Exchanges: $2.47 billion revenue, $1.403 billion operating income; Fixed Income and Data Services: $657 million revenue; Mortgage Technology: $539 million revenue), U.S. Securities and Exchange Commission EDGAR, CIK 0001571949, filed April 30, 2026. https://www.sec.gov/edgar/browse/index.html?cik=1571949

[11] Intercontinental Exchange, Inc. (ICE) quote data, July 10, 2026 close ($135.26; market capitalization approximately $76.49 billion; trailing price-to-earnings ratio 17.84), Perplexity Finance real-time market data, accessed July 12, 2026.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.