Florida Just Wrote the Stablecoin Rulebook Washington Hasn't Finished

Tallahassee's new payment stablecoin law is built for issuers smaller than the market leaders, and that gap is the trade

Key Highlights

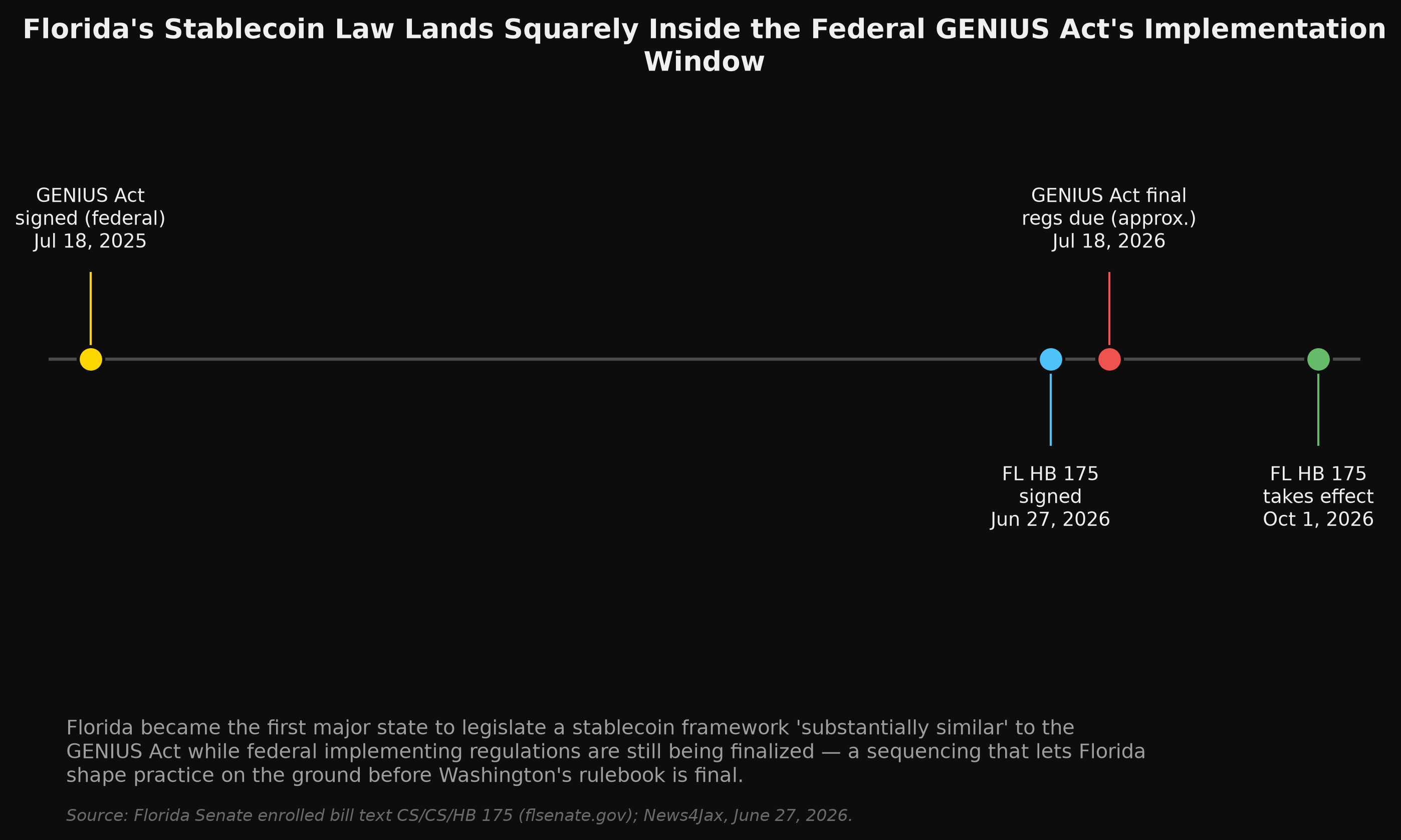

- Gov. Ron DeSantis signed CS/CS/HB 175 on June 27, 2026, creating Florida's first regulatory framework for payment stablecoin issuers, built to be "substantially similar" to the federal GENIUS Act.

- The law's core licensing and prudential provisions don't take effect until October 1, 2026, Florida gave itself a runway to build out certification before enforcement starts.

- Any qualified issuer whose consolidated stablecoin issuance hits $10 billion must, absent a federal waiver, transition to joint OFR/OCC oversight within 360 days or stop issuing new coins, a ceiling both of the two largest stablecoins already blow past.

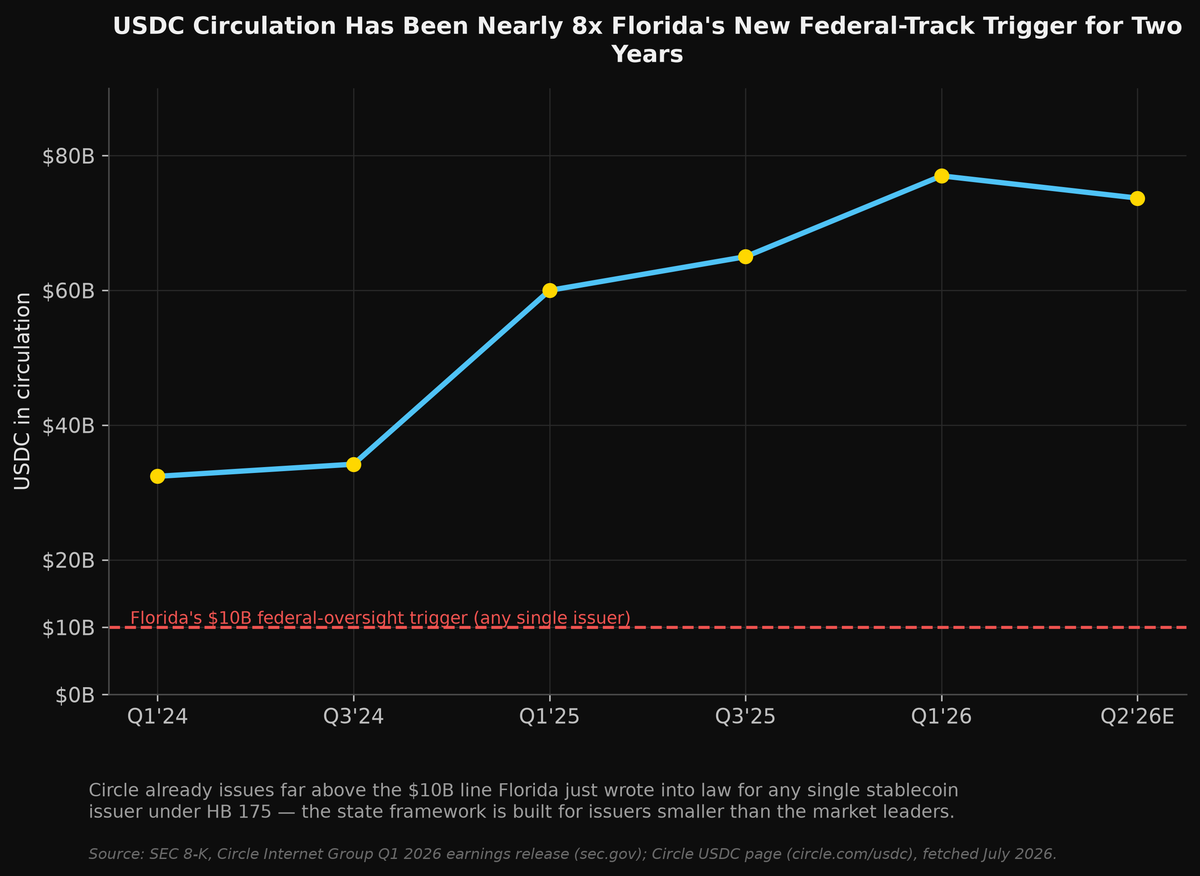

- Circle Internet Group (CRCL), issuer of USDC, reported $77.0 billion in circulation at the end of Q1 2026, nearly eight times Florida's new trigger point.

- The bear case: Florida's framework governs issuers who choose the state track: the giants that already operate under federal money-transmission and securities scrutiny have little reason to opt in at all.

Florida became the first state this year to legislate a payment stablecoin framework explicitly modeled on federal law before that federal law has finished being implemented. On June 27, 2026, Governor Ron DeSantis signed CS/CS/HB 175, Payment Stablecoin, creating a new category of licensed money services business for companies that issue dollar-pegged digital tokens, and giving the state's Office of Financial Regulation supervisory authority modeled directly on the 2025 federal GENIUS Act (Florida Senate Banking and Insurance Committee summary; News4Jax). The bill passed the Florida House 102-2 and the Senate 37-0 (Florida Senate committee summary), the kind of bipartisan margin that regulatory frameworks rarely get once an industry has genuine political opposition.

Start with what the law actually does, because "stablecoin regulation" gets used loosely enough to obscure the mechanics. HB 175 creates "qualified payment stablecoin issuer" as a distinct category under Florida's Money Services Business code, separate from ordinary money transmitters (Florida Senate committee summary). A company can get there two ways: obtain an MSB license from the OFR, or, if it's already a trust company, get a certificate of approval for limited issuer activities, issuing, redeeming, and managing reserves, and nothing much beyond that (Florida Senate, House Amendment to CS/CS/HB 175). Issuers have to back their coins 1:1 with reserves, publish monthly reserve composition reports, and give clear public disclosure of redemption fees and procedures (Florida Senate, House Amendment to CS/CS/HB 175). Stablecoins that meet the bill's requirements are explicitly carved out from Florida's securities law, a classification question that has consumed years of federal-level argument gets resolved at the state level in a single sentence (Florida Senate committee summary).

Here's the detail that matters more than the headline signing date: most of this doesn't take effect for three months. The enrolled bill text creates Section 560.501 of the Florida Statutes, the licensing requirement, the prudential standards, the activity limitations, effective October 1, 2026, not upon signing (Florida Senate, enrolled CS/CS/HB 175 bill text). The OFR needs that runway to stand up certification procedures and coordinate AML reporting with Treasury for an asset class it has never regulated before. Multiple secondary accounts conflated the signing date with the operative date, worth being precise about before anyone prices in enforcement that isn't live yet.

The mechanism that makes this genuinely interesting for markets sits inside the transition-to-federal-oversight clause. Once a qualified issuer's consolidated total outstanding stablecoin issuance reaches $10 billion, the law forces a choice: absent a federal waiver, the issuer has 360 days to transition to a regulatory framework jointly administered by Florida's OFR and the federal Office of the Comptroller of the Currency, or it has to stop issuing new coins entirely until circulation falls back under the threshold (Florida Senate, enrolled bill text, Section 5). That's not a soft guideline. It's a hard statutory switch that converts a state-chartered stablecoin business into a jointly-supervised federal one, or freezes its growth, the moment it gets big enough to matter systemically.

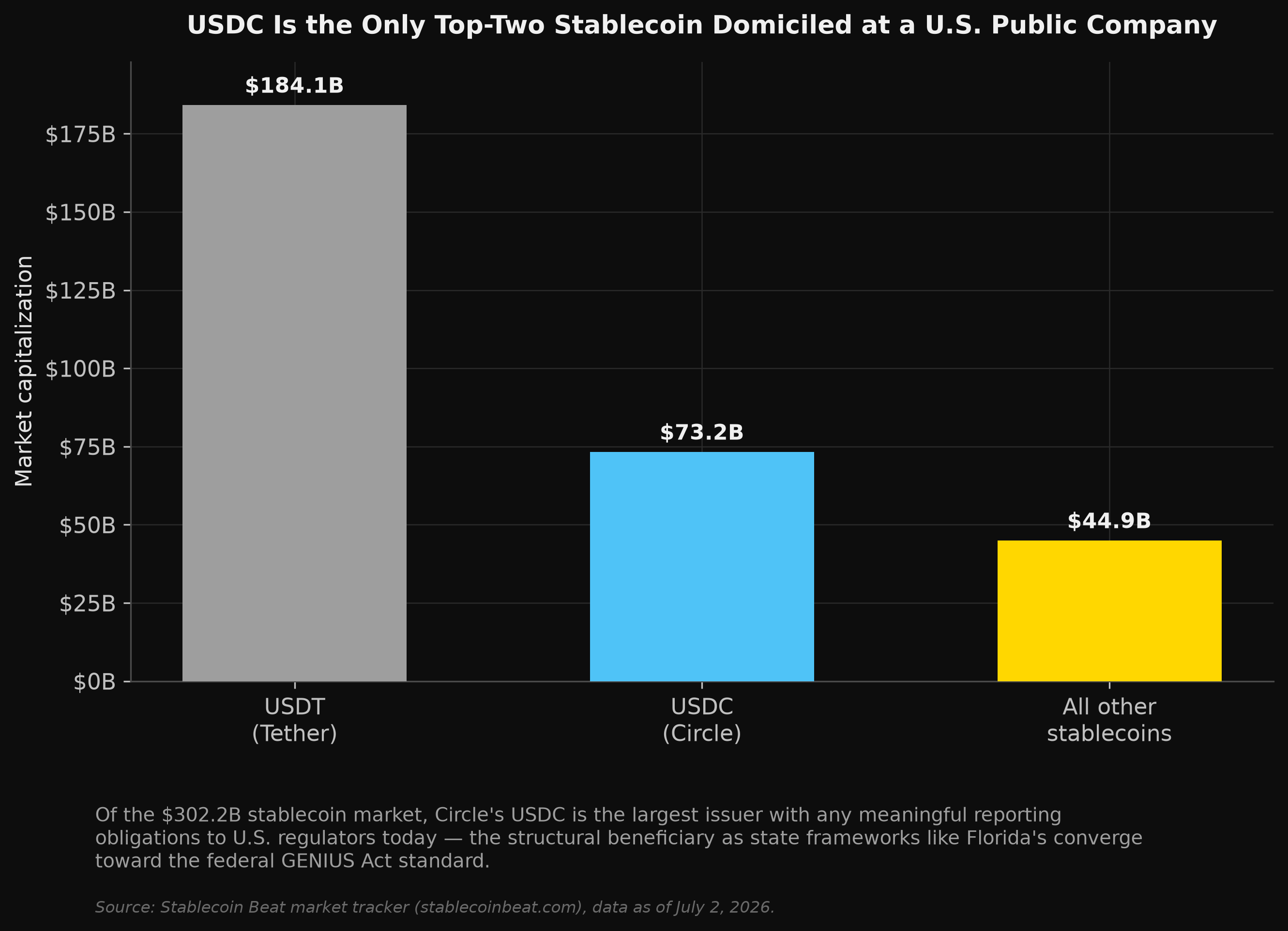

DeSantis signed HB 175 alongside seven other bills that Friday, including a companion measure creating the Florida Stablecoin Pilot Program, which lets the state's Department of Financial Services accept stablecoins for government fee payments (Alachua Chronicle). Take that $10 billion number and look at who it would actually bind. It wouldn't bind either of the two companies that dominate the stablecoin market today. As of July 2, 2026, total stablecoin market capitalization stood at $302.2 billion. Tether's USDT held 60.9% of that at $184.1 billion. Circle's USDC held 24.2% at $73.2 billion (Stablecoin Beat market tracker). Both figures are roughly seven to eighteen times Florida's trigger point. So what is HB 175 actually built for? Issuers smaller than the market leaders, regional banks experimenting with tokenized deposits, fintech challengers, or a future entrant that wants Florida's stamp of legitimacy without immediately courting federal-level scrutiny. The law's real function may be less about regulating the giants and more about giving mid-sized players a credible on-ramp that stops well short of the systemic-risk threshold that triggers Washington's attention.

Circle already issues far above the $10B line Florida just wrote into law for any single stablecoin issuer under HB 175, the state framework is built for issuers smaller than the market leaders. Source: SEC 8-K, Circle Internet Group Q1 2026 earnings release (sec.gov); Circle USDC page (circle.com/usdc), fetched July 2026.

Circle Internet Group is the clearest lens for that dynamic because it is the only top-two stablecoin issuer that reports financials publicly as a U.S. company. Circle's Q1 2026 earnings, filed with the SEC in May, show USDC circulation of $77.0 billion at quarter-end, up 28% year-over-year, alongside total revenue and reserve income of $694 million, up 20% year-over-year (SEC 8-K, Circle Internet Group Q1 2026 earnings release). Reserve income, the interest Circle earns holding the Treasury bills and cash backing every dollar of USDC, made up 94% of that revenue at $653 million (SEC 8-K). Net income from continuing operations came in lower, at $55 million, down 15% year-over-year, even as Adjusted EBITDA rose 24% to $151 million, a gap that reflects Circle's growing non-reserve cost base (compliance, engineering, business development) scaling faster than the bottom line for now. Circle's own investor-facing figure put USDC circulation at $73.7 billion as of June 29, 2026 (Circle USDC page), broadly consistent with the third-party tracker and confirming this isn't a stale number.

Of the $302.2B stablecoin market, Circle's USDC is the largest issuer with any meaningful reporting obligations to U.S. regulators today, the structural beneficiary as state frameworks like Florida's converge toward the federal GENIUS Act standard. Source: Stablecoin Beat market tracker (stablecoinbeat.com), data as of July 2, 2026.

So what actually gets built by frameworks like Florida's, even for issuers that never come close to the trigger threshold, is legal clarity around the plumbing everyone downstream already depends on. USDC onchain transaction volume hit $21.5 trillion in Q1 2026 alone, up 263% year-over-year (SEC 8-K). That volume runs through payment processors and merchants that want state-level regulatory sign-off as a due-diligence checkbox, independent of whether the issuer itself is state- or federally supervised. A framework that formally recognizes stablecoins as non-securities and harmonizes with the federal GENIUS Act reduces legal ambiguity for every bank and payment company integrating stablecoin rails in Florida, that's the addressable effect, even though the marquee issuers sit outside the trigger's reach.

Florida became the first major state to legislate a stablecoin framework 'substantially similar' to the GENIUS Act while federal implementing regulations are still being finalized, a sequencing that lets Florida shape practice on the ground before Washington's rulebook is final. Source: Florida Senate enrolled bill text CS/CS/HB 175 (flsenate.gov); News4Jax, June 27, 2026.

Bear Case. The obvious objection to any stablecoin-regulation-as-catalyst thesis is that it solves a problem the biggest players don't have and doesn't touch the risk that actually matters. Circle and Tether already operate under federal money-transmission licensing, existing state money-services frameworks, and, in Circle's case, SEC reporting obligations as a public company; a new Florida MSB category doesn't materially lower Circle's cost of capital or open a market it couldn't already serve. Second, Florida's framework is state law, and USDC or USDT flow across all fifty states and internationally; a Florida-specific certification does nothing to harmonize the genuinely fragmented patchwork of other state approaches, some of which (New York's BitLicense regime, for instance) remain considerably more restrictive. Third, the $10 billion trigger and 360-day transition clause has never been tested, no issuer has yet crossed that threshold under this exact statute, so the "cease issuing" fallback provision is unproven in practice and could produce unpredictable market effects if an issuer nears the line and has to choose between halting growth and accepting federal supervision on short notice. Finally, this is legislative sequencing risk as much as market opportunity: the federal GENIUS Act's own implementing regulations are still being finalized roughly a year after signing, and a state law that leans on "substantially similar to GENIUS Act" language is exposed if federal rulemaking ultimately diverges from what states assumed when they wrote their own statutes.

Investment Idea: Circle Internet Group (CRCL)

Circle Internet Group (CRCL)

Thesis type: Second-order beneficiary

Deregulatory catalyst: Florida CS/CS/HB 175 (Payment Stablecoin), signed June 27, 2026, establishing a state framework harmonized with the federal GENIUS Act

Current price: See live quote, not independently re-verified for this note; use current market data before acting

Key financial data: Q1 2026 total revenue and reserve income $694M (+20% YoY); USDC in circulation $77.0B (+28% YoY); Adjusted EBITDA $151M (+24% YoY, 53% margin), all per Circle's SEC 8-K (sec.gov)

Regulatory constraint removed: State-level legal ambiguity around stablecoin securities classification and reserve/disclosure standards in Florida, one of the largest state economies and a growing fintech/payments hub

Bull case: As more states pass GENIUS Act-aligned frameworks, USDC's existing federal-adjacent compliance posture becomes a competitive moat against smaller entrants who must build state-by-state licensing from scratch; more state-level legitimacy for stablecoins broadly expands the addressable payment-rail market Circle already leads in transaction volume.

Bear case: Circle sits nearly 8x above Florida's $10 billion trigger already and derives no direct exemption or cost relief from this specific law; reserve income (94% of revenue) remains fully exposed to interest-rate declines, a risk entirely independent of state regulatory action.

What to watch: Whether other large states (New York, Texas, California) pass GENIUS Act-aligned frameworks in the next two legislative sessions, and whether Circle's Q3 2026 filing shows reserve income holding up as the Fed's rate path evolves.

Time horizon: 18–36 months

The pattern to watch is less about Florida specifically than about sequencing. Florida moved before Washington finished its own rulebook, HB 175 was ordered enrolled back in March 2026 and DeSantis signed it in late June, while the GENIUS Act's own final implementing regulations are still pending roughly a year after the federal law itself was signed on July 18, 2025 (Florida Senate, enrolled bill text). States willing to legislate ahead of federal finality get to shape market practice on the ground first. If more large states follow Florida's template before the OCC and Treasury finish federal rulemaking, the *de facto* national standard for stablecoin issuance may end up being assembled from state statutes stitched together, rather than handed down whole from Washington. That is the structural tailwind worth tracking, not because any single state's $10 billion threshold binds the market leaders today, but because the race to define "substantially similar to GENIUS" state-by-state is where the next real compliance moat gets built.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.