Delaware Just Extended Its Corporate Monopoly Into Digital Assets

The state that already owns two-thirds of Fortune 500 charters wrote a stablecoin and custody law aimed at owning crypto's back office too

Key Highlights

- Governor Matt Meyer signed SB 16, SB 18, and SB 19 on July 7, 2026, which Delaware's own press release calls the state's biggest financial regulatory update in more than 40 years (Delaware.gov).

- SB 16 declares digital assets "personal property" under the Delaware Banking Code and adds a deemed-approval mechanism that fast-tracks out-of-state trust companies converting to a Delaware charter (Lowenstein Sandler).

- SB 19 mirrors the federal GENIUS Act's $10 billion issuance threshold, letting smaller stablecoin issuers operate under state, not federal, supervision, with a transition path once they cross that line (Orrick InfoBytes).

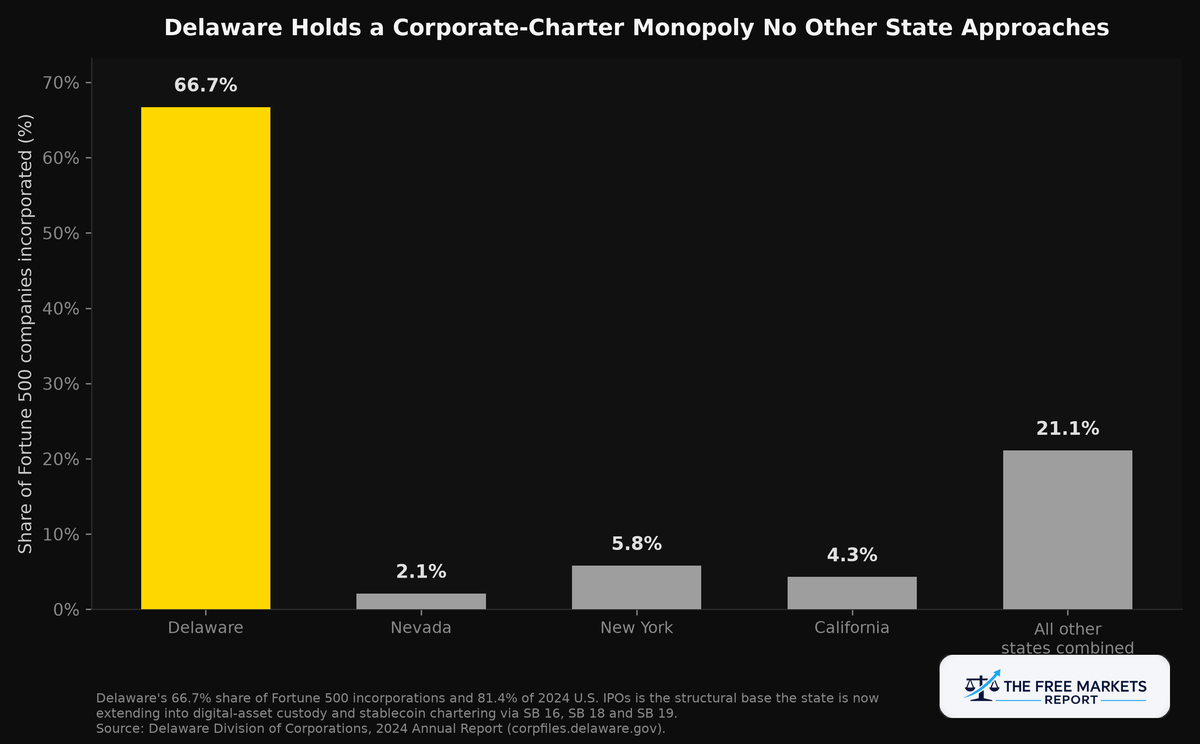

- Delaware already holds 66.7% of Fortune 500 incorporations and 81.4% of 2024 U.S. IPOs, the structural base the new bills are trying to extend into custody and stablecoin infrastructure (Delaware Division of Corporations).

- An Indiana University finance professor quoted by Delaware Public Media is skeptical the state sees a revenue windfall, noting large stablecoins are unlikely to relocate and the fiscal upside is uncertain (Delaware Public Media).

Delaware did not build its economy on tourism, ports, or natural resources. It built it on being the place where corporate charters live. Now the First State wants digital asset custody and stablecoin issuance to live there too.

A 40-Year-Old Playbook, Applied to Crypto

On July 7, 2026, Governor Matt Meyer signed three companion bills, SB 16, SB 18, and SB 19, at the Carvel State Office Building, flanked by the Delaware Bankers Association, the Delaware Credit Union Association, and the American Fintech Council. The state's own framing was blunt: this is the most significant update to Delaware's financial regulatory code "in more than 40 years" (Delaware.gov). Meyer put it plainly at the signing: Delaware "set the national standard for banking innovation" decades ago, and the new package is designed to do it again for financial technology.

The mechanics matter more than the ceremony. SB 16, the Delaware Banking Modernization Act, amends the state banking code to define "digital asset" and "virtual currency" and, critically, confirms that digital assets are personal property under Delaware law. That single definitional change gives Delaware-chartered banks and trust companies clear statutory footing to hold and administer crypto in a fiduciary capacity, something that was legally ambiguous before (Lowenstein Sandler). The bill also lets the State Bank Commissioner tailor chartering requirements by institutional risk profile and eases restrictions on limited-purpose trust companies, the entity type most custody businesses actually use.

The part that should catch an investor's eye is narrower and more mechanical: SB 16 streamlines the conversion of out-of-state trust companies into Delaware charters and adds a deemed-approval clock, meaning if the Commissioner does not act within a set window, the conversion is approved by default (Delaware General Assembly, SB 16). That is a direct incentive for custody-heavy financial firms chartered elsewhere to move their trust entity to Delaware, the same regulatory-arbitrage logic that has driven corporate reincorporation into the state for a century.

SB 18, the Money Transmission and Virtual Currency Modernization Act, repeals Delaware's old money-transmitter chapter and replaces it with a modern licensing and consumer-protection regime, with standardized definitions and exemptions for FDIC-insured banks, government entities, and broker-dealers (Orrick InfoBytes). It is the plumbing bill: less exciting, but it is what lets virtual-currency businesses actually operate legally in the state at scale.

SB 19, the Delaware Payment Stablecoins Act, is the one drawing outside attention. It is explicitly modeled on the federal GENIUS Act and requires 1:1 reserve backing in cash, short-dated Treasury bills maturing in 93 days or less, and certain repo instruments, with no rehypothecation except in narrow cases. Redemption must happen within two business days, or seven calendar days if redemption demands exceed 10% of outstanding issuance in a single 24-hour window. De novo issuers need $5 million in minimum capital, and monthly reserve reports must be examined by a registered public accounting firm (Delaware General Assembly, SB 19 full text). Crucially, SB 19 carries the same $10 billion outstanding-issuance threshold the GENIUS Act uses to decide when a state-qualified issuer must transition to federal OCC oversight, which keeps Delaware's regime interoperable with the national framework rather than competing against it (Orrick InfoBytes; Arnold & Porter).

Why Charter Geography Still Matters in a Digital Business

Skeptics will point out, correctly, that a blockchain does not care what state a trust company is chartered in. But custody businesses are not blockchains. They are regulated fiduciaries with boards, capital requirements, audit obligations, and legal liability, and those live in a specific jurisdiction's courts and case law. That is exactly the reason Delaware built its corporate-law dominance in the first place, and the reason 66.7% of Fortune 500 companies and 81.4% of 2024 IPOs chose Delaware as their legal home despite having zero physical operations there (Delaware Division of Corporations, 2024 Annual Report).

Delaware's Chancery Court has more than a century of case law resolving fiduciary duty disputes, board authority questions, and creditor priority fights. When SB 16 makes digital assets personal property under a banking code backed by that court system, it is offering custody businesses the same legal predictability that has made Delaware the default choice for corporate charters generally. That predictability has commercial value that shows up nowhere on a balance sheet until a dispute happens, and then it is the only thing that matters.

The Investment Angle: Coinbase and the Custody Infrastructure Layer

Ticker: COIN (Coinbase Global, Inc.), NASDAQ

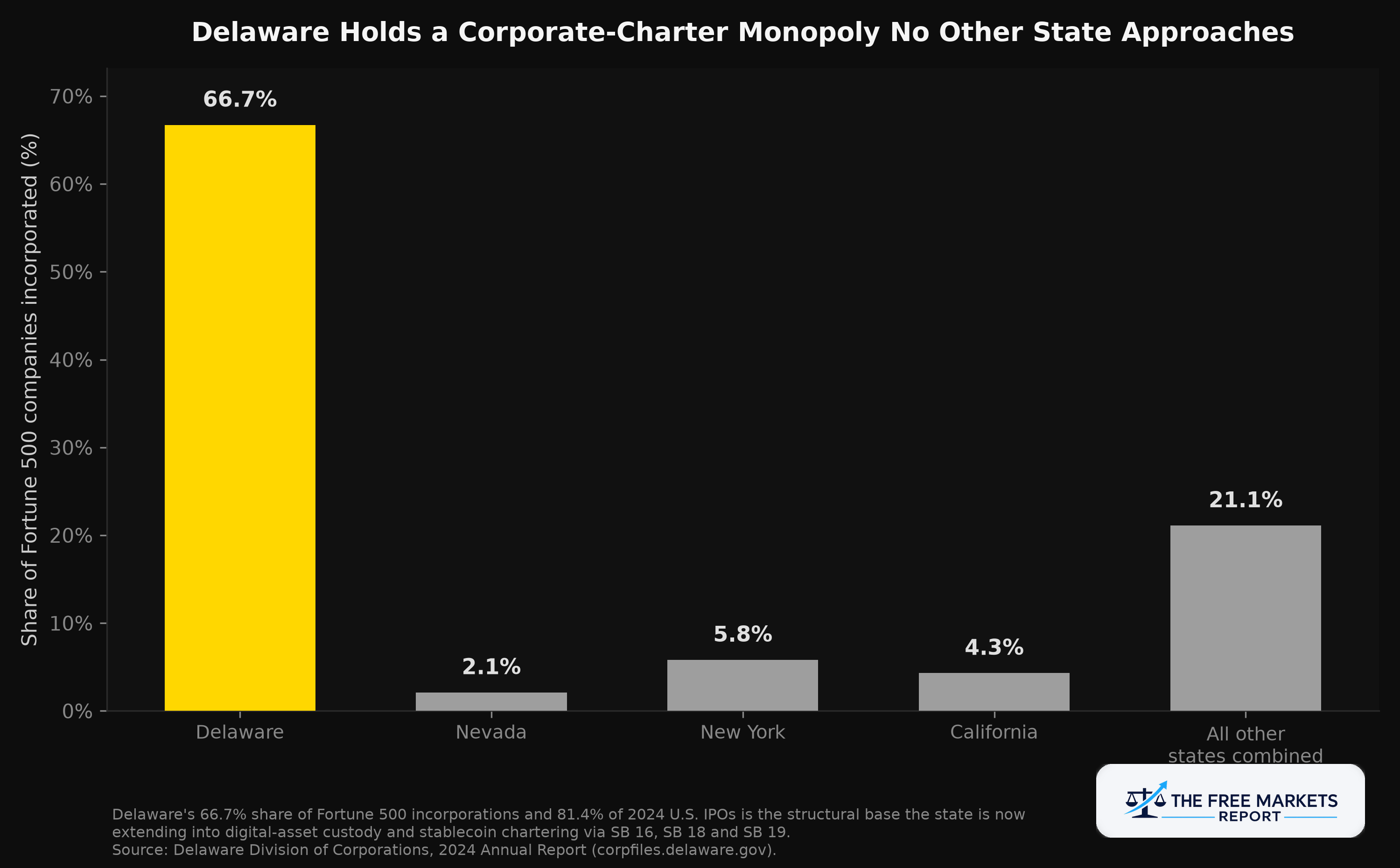

Coinbase remains the largest crypto custodian in the world by assets, holding $294 billion in Assets on Platform at the end of Q1 2026, down from an all-time high of $516 billion in Q3 2025 as crypto prices fell, not because custody clients withdrew (Coinbase Q1 2026 Shareholder Letter; MarketBeat earnings transcript). The company posted its 12th consecutive quarter of net native unit inflows in Q1 2026, meaning clients kept adding assets even as market values dropped (MarketBeat).

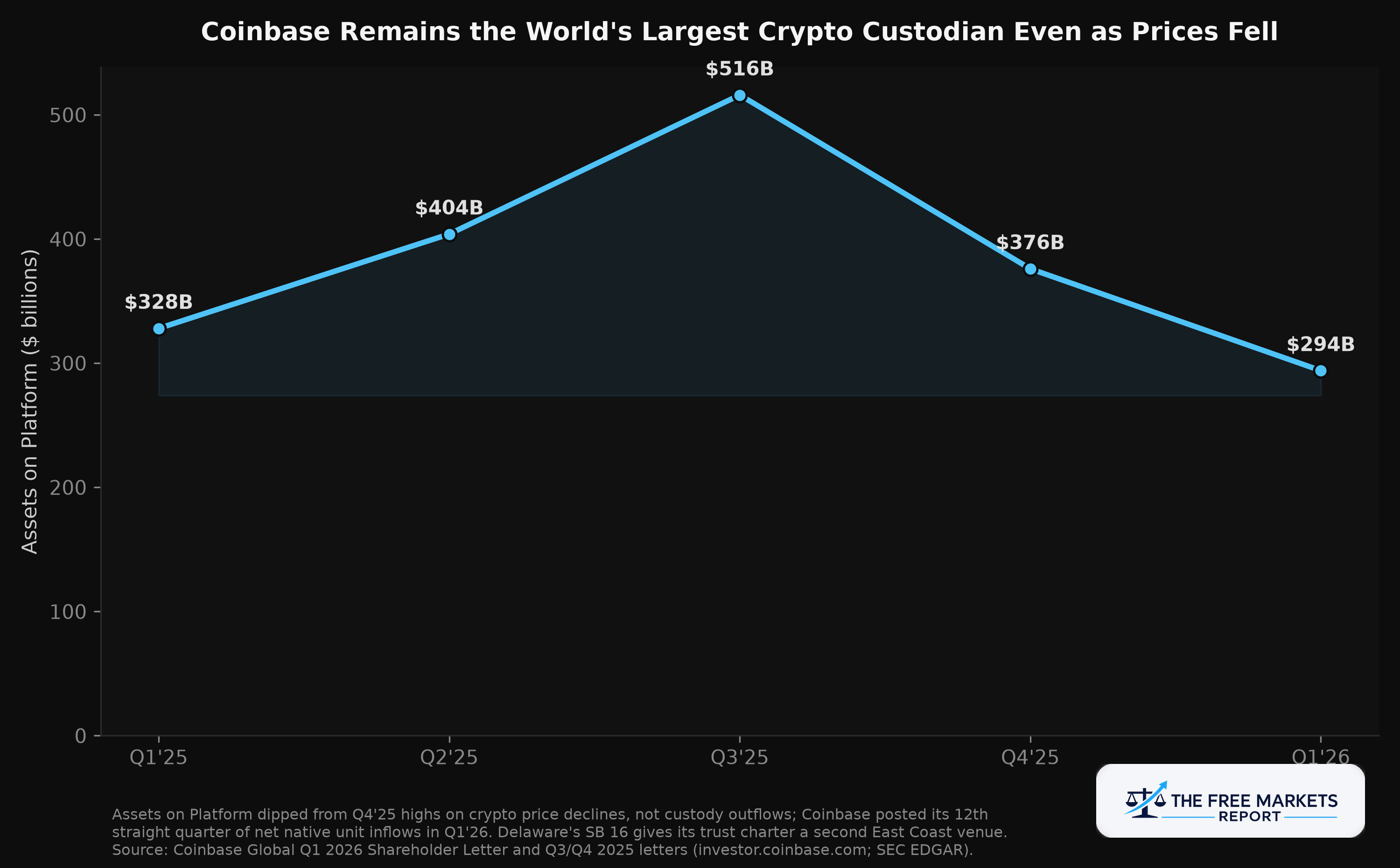

Coinbase's Q1 2026 revenue mix shows exactly the diversification Delaware's framework is built to reinforce. Total revenue was $1.41 billion, with $305 million from stablecoin revenue and $179 million from custody and other subscription revenue, together outpacing the $136 million in institutional transaction revenue (Coinbase Q1 2026 earnings materials). More than 25% of all circulating USDC now sits in Coinbase products, and the company's 10-K describes Coinbase Prime as custodian for several Bitcoin and Ethereum ETF issuers (Coinbase FY2025 10-K). This is a business whose core value proposition is being the trusted custody counterparty for institutional crypto, precisely the category SB 16 is engineered to attract.

The nuance matters here. Coinbase's primary custody trust entity is chartered in New York, not Delaware, per its OCC digital asset filings (OCC filing), so this is not a story where Coinbase needs Delaware to exist. The mechanism for COIN shareholders runs through the deemed-approval conversion pathway in SB 16: a competitive second East Coast trust-chartering venue with the personal-property statutory clarity Coinbase already relies on in principle. It lowers the switching cost and increases the optionality for custody-heavy crypto firms broadly, of which Coinbase is the largest and most liquid public proxy, creating a structural tailwind for the custody infrastructure category that Coinbase currently leads by scale, rather than a company-specific regulatory catalyst unique to COIN alone.

Bull Case

Delaware's deemed-approval charter-conversion mechanism lowers the cost and legal risk of establishing or relocating trust-company infrastructure, at the exact moment stablecoin issuance and crypto custody are both scaling nationally under the GENIUS Act's framework. Coinbase, as the largest crypto custodian globally with $294 billion in assets and a stablecoin revenue line already at $305 million a quarter, is the most exposed public entity to any expansion in the addressable custody and stablecoin market that a more hospitable chartering environment, in Delaware or elsewhere, helps create. The historical base rate favors this: Delaware's century of corporate-charter dominance shows that legal predictability compounds market share over time, and the state is applying the identical playbook to digital-asset fiduciary law now.

Bear Case

Kristoph Kleiner, an associate finance professor at Indiana University's Kelley School of Business, told Delaware Public Media that while SB 19 could be the most consequential of the three bills, its revenue impact for Delaware is "probably the most uncertain," and he does not expect large, well-known stablecoins to relocate to the state or a meaningful fiscal windfall to materialize (Delaware Public Media). That skepticism applies with equal force to the investment thesis: Coinbase's dominant custody position was built under a New York trust charter, not a Delaware one, which means the company has no urgent operational need to use SB 16's conversion pathway at all. If custody demand simply continues flowing through existing New York and federal OCC-chartered structures, Delaware's new framework becomes a redundant option rather than a real switching catalyst, and the thesis compresses to a generic bet on crypto custody growth that has nothing to do with Delaware specifically.

What to Watch

Track two things. First, any announced trust-company charter conversions or new Delaware trust applications from custody or stablecoin firms in the twelve months following the July 7 signing, which would validate the deemed-approval mechanism is actually being used. Second, Coinbase's quarterly custody and stablecoin revenue lines relative to transaction revenue: continued convergence toward the $300 million-plus quarterly stablecoin run rate would confirm the diversification thesis independent of the Delaware angle specifically.

The Principle

Regulatory competition between states is not an abstraction. It is the reason a state with under one-third of one percent of the U.S. population houses the legal domicile of two-thirds of the country's largest public companies. Delaware is not waiting to see whether digital assets are a durable financial category before writing the rules; it is applying the same charter-arbitrage model that built its corporate dominance to crypto custody and stablecoins now, while the market is still being defined. Whether that produces a fiscal windfall for the state is genuinely uncertain, as Kleiner notes. Whether it reinforces the market position of the custody businesses already positioned to benefit from lower legal friction is a separate and more answerable question.

Footnotes

- Delaware.gov, "Gov. Meyer Signs Banking Modernization Package to Strengthen Delaware's Leadership in Financial Services," July 7, 2026. https://news.delaware.gov/2026/07/07/gov-meyer-signs-banking-modernization-package-to-strengthen-delawares-leadership-in-financial-services/

- Delaware General Assembly, SB 16 (Delaware Banking Modernization Act of 2026), Bill Detail. https://legis.delaware.gov/BillDetail/142987

- Delaware General Assembly, SB 19 (Delaware Payment Stablecoins Act), full text. https://legis.delaware.gov/json/BillDetail/GeneratePdfDocument?legislationId=142988&legislationTypeId=1&docTypeId=2&legislationName=SB19

- Lowenstein Sandler, "Delaware's Bid for the Stablecoin Market: What SB 16 and SB 19 Mean for Digital Asset Firms," May 11, 2026. https://www.lowenstein.com/news-insights/publications/client-alerts/delaware-s-bid-for-the-stablecoin-market-what-sb-16-and-sb-19-mean-for-digital-asset-firms-sec-lit-fctm

- Orrick InfoBytes, "Delaware Enacts Financial Services Modernization Package," July 10, 2026. https://infobytes.orrick.com/2026-07-10/delaware-enacts-financial-services-modernization-package/

- Delaware Public Media, "Fintech growing, but financial expert says windfall from First State's new digital banking rules uncertain," July 10, 2026. https://www.delawarepublic.org/politics-government/2026-07-10/fintech-growing-but-financial-expert-says-windfall-from-first-states-new-digital-banking-rules-uncertain

- Delaware Division of Corporations, 2024 Annual Report. https://corpfiles.delaware.gov/Annual-Reports/Division-of-Corporations-2024-Annual-Report.pdf

- Coinbase Global, Q3 2025 Shareholder Letter. https://investor.coinbase.com/files/doc_financials/2025/q3/Q3-25-Shareholder-Letter.pdf

- MarketBeat, Coinbase Global Q1 2026 Earnings Report, May 7, 2026. https://www.marketbeat.com/earnings/reports/2026-5-7-coinbase-global-stock/

- Investing.com, "Coinbase Q1 2026 slides: market share gains amid earnings miss," May 8, 2026. https://www.investing.com/news/company-news/coinbase-q1-2026-slides-market-share-gains-amid-earnings-miss-93CH-4671029

- Coinbase Global, FY2025 Form 10-K. https://materials.proxyvote.com/Approved/19260Q/20260421/10K_632568.PDF

- Office of the Comptroller of the Currency, Coinbase National Trust Company digital asset licensing filing. https://www.occ.treas.gov/topics/charters-and-licensing/digital-assets-licensing-applications/coinbase-national-trust-company.pdf

- Arnold & Porter, "What You Need To Know About the New Stablecoin Legislation," July 21, 2025. https://www.arnoldporter.com/en/perspectives/advisories/2025/07/new-stablecoin-legislation-analyzing-the-genius-act

- MarketBeat, Coinbase Global (COIN) Stock Chart and Price History, accessed July 13, 2026. https://www.marketbeat.com/stocks/NASDAQ/COIN/chart/

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.