Britain Just Moved the Wall Around Its Biggest Banks. It Didn't Tear It Down.

HM Treasury's ring-fencing reform hands NatWest and its peers a capped growth lever, not the abolition banks asked for

On May 18, 2026, HM Treasury published the outcome of a review that Britain's biggest banks had spent more than a year lobbying to win outright, and did not get.¹ Five banking groups, Lloyds, NatWest, HSBC UK, Barclays UK and Santander UK, have operated under the UK's ring-fencing regime since January 1, 2019, legally walling off retail deposits from investment banking risk in the wake of the 2008 crisis.² In April 2025, the chief executives of HSBC, Lloyds, NatWest and Santander UK wrote jointly to the Chancellor calling the regime "obsolete" and asking for its elimination.³ What they got instead was narrower: a capped allowance to redeploy a slice of their balance sheets, more flexibility to share back-office costs, and a promise that Parliament would eventually touch the underlying law.⁴ The size of the win determines the size of the trade.

The Mechanism, Not the Press Release

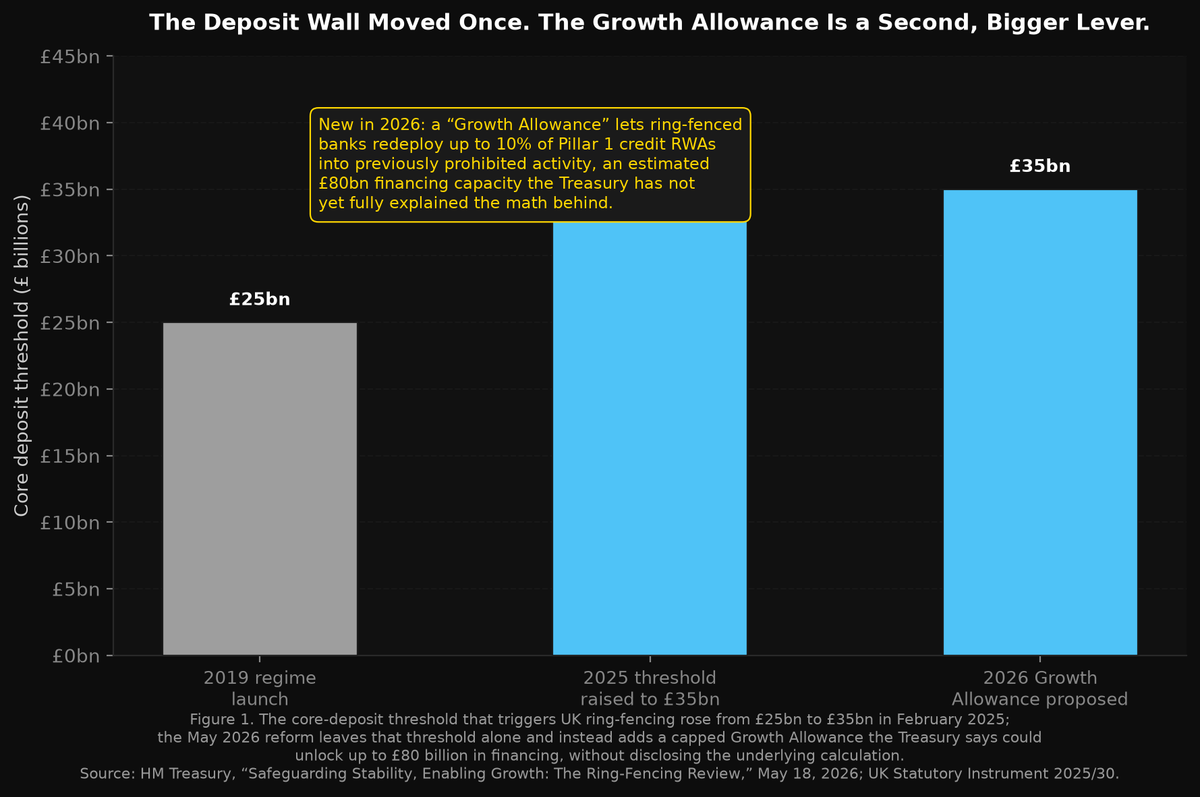

Start with what actually changed on May 18. The core-deposit threshold that determines which banks are ring-fenced in the first place did not move. It already rose once, from £25 billion to £35 billion, under a statutory instrument that came into force February 4, 2025.⁵ The 2026 package leaves that £35 billion line in place and instead introduces a "Growth Allowance" that would let ring-fenced banks undertake activities currently prohibited inside the fence, up to a limit of 10% of their Pillar 1 credit risk-weighted assets.⁶ The Treasury's own document says this could unlock up to £80 billion of additional financing for UK businesses and infrastructure.⁷ The Treasury has not published how it arrived at that number. Bloomberg's coverage of the announcement noted the figure was released "without saying how that figure was calculated."⁸ That is not a reason to dismiss the reform. It is a reason to treat £80 billion as a ceiling, not a forecast.

The Prudential Regulation Authority moved in parallel. The same day, the Bank of England said the PRA would consult this summer on letting ring-fenced and non-ring-fenced entities inside the same banking group share operational services, including data processing, IT, and back-office functions, currently walled off from each other by law.⁹ Separately, the Financial Policy Committee recommended lowering the aggregate capital-requirement benchmark for UK banks from 14% to 13%, a parallel loosening that compounds the ring-fencing package.¹⁰

Here is the part that gets lost in the "deregulation" framing: the government explicitly said no to the thing banks wanted most. PwC's regulatory analysis is direct about this. The government rejected proposals to allow greater sharing of funding and liquidity across the ring-fence without additional safeguards, concluding such changes could undermine depositor protection and financial stability.¹¹ Banks can share an IT department. They cannot yet share a balance sheet. That gap, between "banks asked for X" and "banks got a bounded version of X," is where mispricing tends to live.

Legislative Reality: A Bill, Not Yet a Law

None of this takes effect by fiat. The primary legislative vehicle, the Financial Services and Markets Bill, was introduced in the House of Lords on May 19, 2026, with no confirmed date for its second reading as of early June.¹² Most substantive changes, including the Growth Allowance's detail, require secondary legislation after enactment, and consultation on the Allowance's scope will not begin until summer 2026.¹³ Deloitte's own read is that full implementation will likely take at least two years.¹⁴ This is a multi-year regulatory unlock announced on a single afternoon, and the market's reaction window and the policy's delivery window are not the same window.

Who Actually Benefits

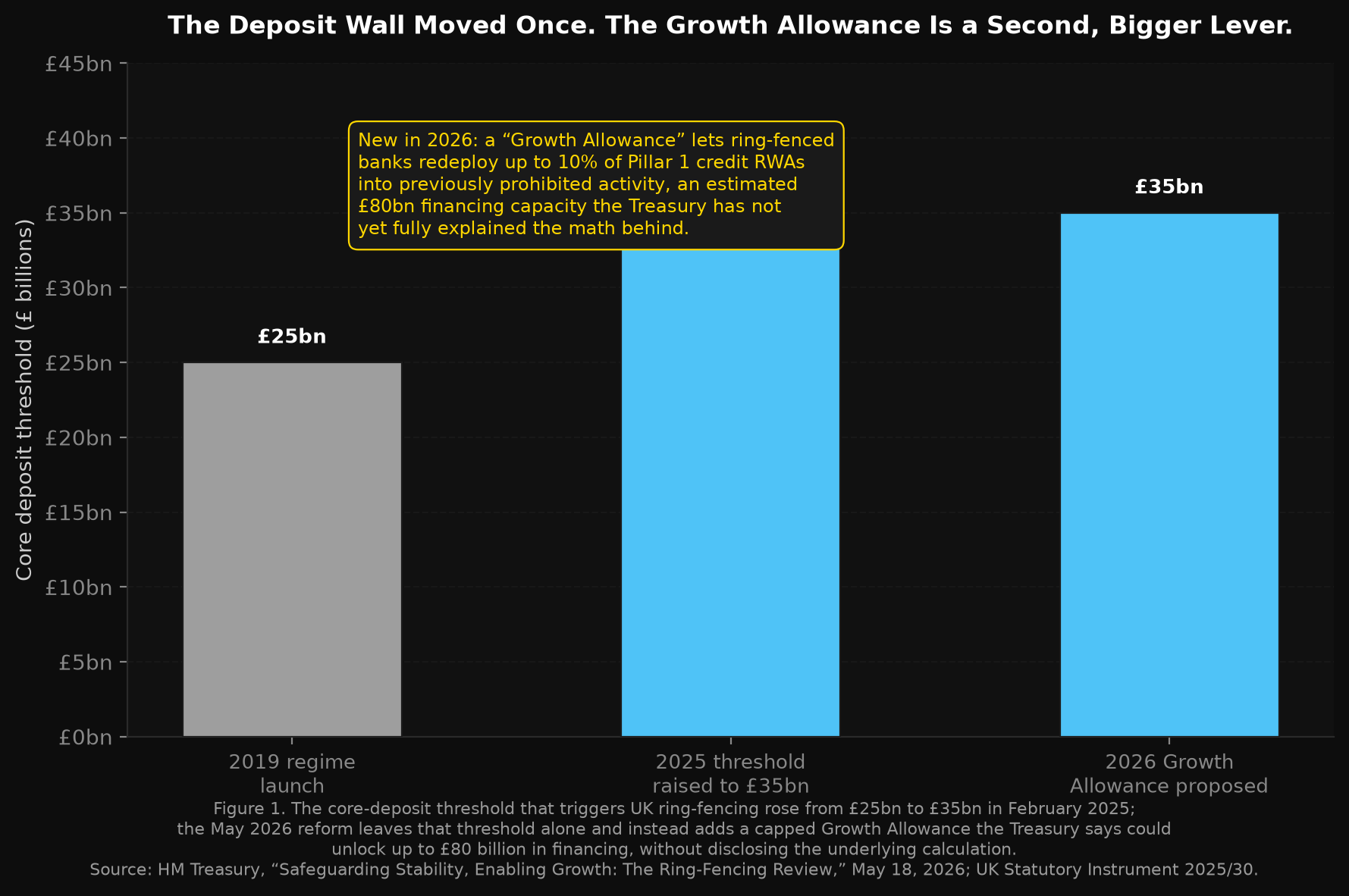

The five banks inside the ring-fence are the direct beneficiaries of both the cost-sharing consultation and the Growth Allowance, if and when it clears Parliament and consultation.¹⁵ But not every ring-fenced bank is equally positioned to use new balance-sheet flexibility the moment it becomes available, and that is the non-obvious part of the thesis. A bank sitting exactly at its regulatory capital floor gains little from a permission slip to redeploy capital: it has none spare. A bank generating capital faster than its own guided target can absorb is the one for whom "up to 10% of Pillar 1 credit RWAs" is unused capacity waiting for a rule change.

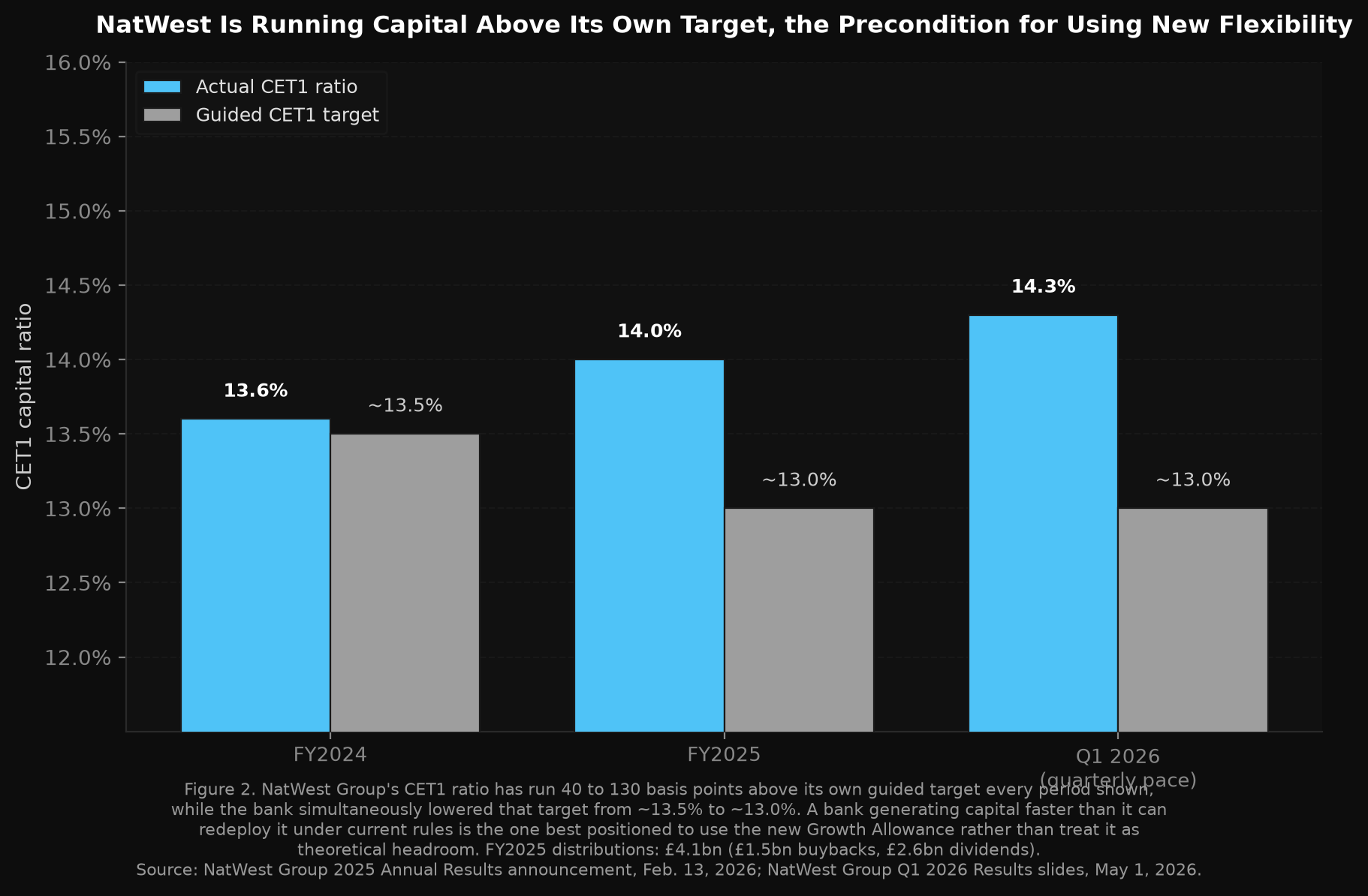

NatWest Group (NYSE: NWG) is that second kind of bank. In its 2025 annual results, NatWest reported a CET1 capital ratio of 14.0% at year-end, up roughly 40 basis points during the year, while lowering its own long-run CET1 target to around 13.0%.¹⁶ By the first quarter of 2026, that ratio had climbed further, to 14.3%, again against a guided target of roughly 13.0%.¹⁷ NatWest generated £10.9 billion of risk-weighted-asset management actions during 2025 alone, part of what the bank calls "capital velocity."¹⁸ Full-year 2025 total income excluding notable items was £16.4 billion, operating profit before tax was £7.7 billion, and Return on Tangible Equity was 19.2%.¹⁹ NatWest returned £4.1 billion to shareholders in 2025, split between £1.5 billion of buybacks and £2.6 billion of dividends, and announced a further £750 million buyback for the first half of 2026.²⁰ The UK government, once NatWest's majority owner after the 2008 bailout, had reduced its stake to below 29% by the first quarter of 2026, en route to a full exit.²¹ NatWest's ADR traded at $17.99 with a market capitalization of approximately $72.2 billion as of a late-June 2026 data pull, compared with Lloyds Banking Group's ADR market capitalization of approximately $88.8 billion as of a July 2, 2026 fetch, the two largest ring-fenced banks with U.S.-listed shares.²²

None of that capital-return activity required ring-fencing reform. What the reform potentially changes is the menu of things NatWest can do with excess capital inside the fence, rather than exclusively through dividends and buybacks. That is a capital-allocation optionality story, not a "the stock is cheap because of a new law" story.

The Bear Case

The strongest argument against this thesis is that the catalyst is smaller, slower, and less certain than the "deregulation" label implies.

First, the £80 billion figure is a government estimate attached to a policy not yet calibrated; the Growth Allowance's actual size will not be set until the summer 2026 consultation concludes, and consultations can shrink proposals as often as they preserve them. Second, the timeline risk is not cosmetic. The Financial Services and Markets Bill had no confirmed second-reading date as of early June 2026, and Deloitte's independent estimate is that full implementation runs at least two years.²³ The falsification condition: if the Bill fails to advance past a first reading by the end of 2026, or if the summer 2026 consultation produces an Allowance materially smaller than the 10% RWA ceiling, this thesis is meaningfully weakened. Third, this is precisely the outcome the industry did not want. Bank chief executives asked for ring-fencing's elimination and received bounded, consultation-gated flexibility instead, with funding and liquidity sharing across the fence explicitly refused.²⁴ If the market has already priced in something closer to full abolition, the actual delivered policy could disappoint that expectation even though it is, on its own terms, a genuine loosening.

Investment Idea

INVESTMENT IDEA: NatWest Group (NYSE: NWG) Thesis type: Primary beneficiary, capital-allocation optionality angle Deregulatory catalyst: HM Treasury and PRA's May 18, 2026 ring-fencing reform, specifically the proposed Growth Allowance (up to 10% of Pillar 1 credit RWAs) and the PRA's summer 2026 consultation on shared operational services across the ring-fence.²⁵ Current price: NWG ADR traded at $17.99 with a market capitalization of approximately $72.2 billion as of a late-June 2026 data pull.²⁶ Key financial data: FY2025 total income excluding notable items of £16.4 billion, operating profit before tax of £7.7 billion, Return on Tangible Equity of 19.2%, CET1 ratio of 14.0% against a guided target of approximately 13.0%; Q1 2026 CET1 ratio of 14.3%, Return on Tangible Equity of 18.2%.²⁷ Regulatory constraint removed: None yet, formally. What exists today is a capped, consultation-gated permission to redeploy ring-fenced balance-sheet capacity into currently prohibited activity, plus a parallel path to share back-office costs. Both require further consultation and, for the primary legislative change, passage of the Financial Services and Markets Bill.²⁸ Bull case: NatWest is already generating capital faster than its own guided target can absorb under current rules, evidenced by a CET1 ratio running 40 to 130 basis points above target across the last three reported periods, a bank structurally positioned to use new flexibility the moment it clears Parliament and consultation. Bear case: The financing unlock is a government estimate, not a calibrated rule; the legislative and consultation timeline extends past 2026 into 2027 or 2028; and the reform delivered is explicitly smaller than what bank leadership requested. What to watch: The PRA's summer 2026 consultation document on shared operational services, and the Financial Services and Markets Bill's progress to a second reading in the House of Lords. Time horizon: 18 to 36 months, contingent on legislative and consultation milestones.

The Principle

Deregulation is not binary. It arrives in Britain, as it does in Washington or in any statehouse, as a negotiated distance between what an industry asked for and what a government was willing to give. The headline said the UK loosened bank regulation. The primary documents say something more specific: a five-bank regime survives intact, a capped allowance is proposed but not yet calibrated, funding and liquidity sharing was refused outright, and the legislative clock runs past this year regardless of how the announcement was covered. The investor who reads the review document, not just the press release, is the one who can tell the difference between a bank that benefits from a headline and a bank structurally positioned to benefit from the mechanism underneath it.

Read the primary source. Find the gap between the ask and the answer. That gap is where the mispricing lives.

Michael A. Gayed, CFA

Footnotes

- HM Treasury, "Safeguarding Stability, Enabling Growth: The Ring-Fencing Review," GOV.UK, May 18, 2026. https://www.gov.uk/government/publications/safeguarding-stability-enabling-growth-the-ring-fencing-review

- Bank of England, "Ring-fencing," Prudential Regulation key initiatives page. https://www.bankofengland.co.uk/prudential-regulation/key-initiatives/ring-fencing

- Reuters, "Top British bank chiefs urge finance minister to scrap ring-fencing in letter," April 26, 2025. https://www.reuters.com/business/finance/top-british-bank-chiefs-urge-chancellor-scrap-ring-fencing-letter-sky-news-2025-04-26/

- HM Treasury, "Safeguarding Stability, Enabling Growth" (PDF). https://assets.publishing.service.gov.uk/media/6a0ae2c5279ebb7d24f8f39b/Safeguarding_Stability__Enabling_Growth.pdf

- The Financial Services and Markets Act 2000 (Ring-fenced Bodies, Core Activities, Excluded Activities and Prohibitions) (Amendment) Order 2025, legislation.gov.uk. https://www.legislation.gov.uk/uksi/2025/30/made

- HM Treasury, "Safeguarding Stability, Enabling Growth" (PDF), Chapter 3. https://assets.publishing.service.gov.uk/media/6a0ae2c5279ebb7d24f8f39b/Safeguarding_Stability__Enabling_Growth.pdf

- Ibid.

- Bloomberg (Joe Mayes), "UK to Scrap Parts of Ring-Fencing Rules to Boost Lending," May 18, 2026. https://www.bloomberg.com/news/articles/2026-05-18/uk-plans-to-scrap-parts-of-ring-fencing-regime-to-boost-lending

- Bank of England, "PRA announces ring-fence change to reduce costs," May 18, 2026. https://www.bankofengland.co.uk/news/2026/may/pra-announces-ring-fence-change-to-reduce-costs

- Ibid.

- PwC UK, "HMT sets out Ring-Fencing Review findings," May 20, 2026. https://www.pwc.co.uk/industries/financial-services/understanding-regulatory-developments/hmt-sets-out-ring-fencing-review-findings.html

- Simmons & Simmons, "The Financial Services and Markets Bill 2026-27: key reforms," June 4, 2026. https://www.simmons-simmons.com/en/publications/cmpzcp1yl008kv6xk30l6igas/the-financial-services-and-markets-bill-2026-27-key-reforms

- HM Treasury, "Safeguarding Stability, Enabling Growth" (PDF), Next Steps table. https://assets.publishing.service.gov.uk/media/6a0ae2c5279ebb7d24f8f39b/Safeguarding_Stability__Enabling_Growth.pdf

- Deloitte UK, "King's Speech 2026 and the Financial Services and Markets Bill," May 14, 2026. https://www.deloitte.com/uk/en/blogs/ecrs/kings-speech-2026-what-does-it-mean-for-financial-services-regulation.html

- Reuters, "Bank of England to resist big changes to ring-fencing regime, sources say," November 18, 2025. https://www.reuters.com/sustainability/boards-policy-regulation/bank-england-resist-big-changes-ring-fencing-regime-sources-say-2025-11-18/

- NatWest Group, 2025 Annual Results announcement (PDF), February 13, 2026. https://investors.natwestgroup.com/~/media/Files/R/RBS-IR-V2/results-center/13022026/nwg-company-announcement.pdf

- NatWest Group, Q1 2026 Results slides (PDF), May 1, 2026. https://investors.natwestgroup.com/~/media/Files/R/RBS-IR-V2/results-center/01052026/nwg-q1-2026-slides.pdf

- NatWest Group, 2025 Annual Results announcement (PDF), February 13, 2026. https://investors.natwestgroup.com/~/media/Files/R/RBS-IR-V2/results-center/13022026/nwg-company-announcement.pdf

- Ibid.

- Ibid.

- Investing.com, "Earnings call: NatWest Group reports solid Q1 growth, eyes future returns," 2026. https://www.investing.com/news/stock-market-news/earnings-call-natwest-group-reports-solid-q1-growth-eyes-future-returns-93CH-3403834

- StockAnalysis.com, NatWest Group (NWG) and Lloyds Banking Group (LYG) overviews. https://stockanalysis.com/stocks/nwg/ ; https://stockanalysis.com/stocks/lyg/

- Deloitte UK, "King's Speech 2026 and the Financial Services and Markets Bill," May 14, 2026. https://www.deloitte.com/uk/en/blogs/ecrs/kings-speech-2026-what-does-it-mean-for-financial-services-regulation.html

- PwC UK, "HMT sets out Ring-Fencing Review findings," May 20, 2026. https://www.pwc.co.uk/industries/financial-services/understanding-regulatory-developments/hmt-sets-out-ring-fencing-review-findings.html

- Bank of England, "PRA announces ring-fence change to reduce costs," May 18, 2026. https://www.bankofengland.co.uk/news/2026/may/pra-announces-ring-fence-change-to-reduce-costs

- StockAnalysis.com, NatWest Group (NWG) overview. https://stockanalysis.com/stocks/nwg/

- NatWest Group, Q1 2026 Results slides (PDF), May 1, 2026. https://investors.natwestgroup.com/~/media/Files/R/RBS-IR-V2/results-center/01052026/nwg-q1-2026-slides.pdf

- HM Treasury, "Safeguarding Stability, Enabling Growth" (PDF). https://assets.publishing.service.gov.uk/media/6a0ae2c5279ebb7d24f8f39b/Safeguarding_Stability__Enabling_Growth.pdf

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.