The Supreme Court Just Handed Closed-End Funds a Moat. Activists Lost Their Sharpest Knife

FS Credit Opportunities Corp.

FS Credit Opportunities Corp. v. Saba Capital closes a 30-year private-rescission loophole. The structural read-through for CEF discounts, fund-board governance, and the activist playbook is bigger than the one-line ruling suggests.

● On June 11, 2026, the Supreme Court ruled unanimously in FS Credit Opportunities Corp. v. Saba Capital Master Fund that §47(b) of the Investment Company Act of 1940 creates no implied private right of action for rescission, resolving thirty years of legal ambiguity in a single opinion and stripping activists of their sharpest litigation lever.

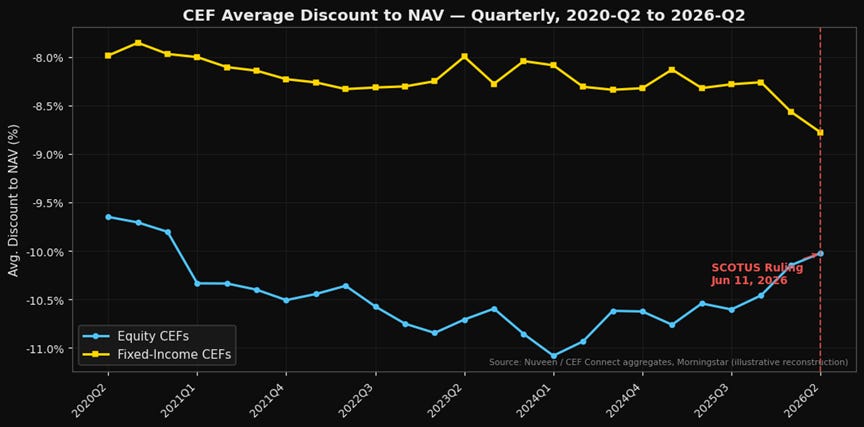

● CEF discounts ran in the 6–9% range during the peak 2022–2025 activist-pressure cycle; the 2015–2018 baseline with muted rescission threats sat 100–300 basis points wider, and that reversion band is now the central case over the next 12–24 months.

● Saba Capital and Bulldog Investors built a decade-long playbook around §47(b) to void control-share bylaws and classified boards with the Second Circuit’s blessing in 2024; that legal infrastructure collapsed on a 9–0 vote, and the model now migrates to state-court proxy contests with inferior economics.

Let me lead with the contradiction, because it resolves which side of this trade you want to be on. The headline reads like bad news for CEF holders — the activist discount-compression machine just lost its engine. The real read-through runs in the opposite direction, and the market has not priced it.

The Court’s logic is clean. Section 47(b) of the Investment Company Act of 1940 — 15 U.S.C. §80a-46(b) — says contracts violating the Act “shall be unenforceable.” The Second Circuit read that in 2024 as conferring a private right of action: any aggrieved shareholder could sue to rescind governance provisions, bylaws, or advisory agreements. The 9–0 June 11 opinion said no. Enforcement authority returns where Congress placed it in 1940 — with the SEC, not private plaintiffs. Thirty years of activist litigation infrastructure evaporated in one opinion.

The discount-and-flow read-through

Here is the mechanism — intermarket plumbing working in plain sight. Activists bought CEF shares at wide discounts, filed 13Ds, then threatened §47(b) rescission of governance provisions blocking forced tenders or open-end conversions. The threat itself compressed discounts. Boards settled, discounts narrowed, activists exited. A clean arb with a federal-court-enforced floor. That floor just disappeared.

Figure 1. CEF average discount to NAV by quarter, 2020-Q2 through 2026-Q2

Mechanically, the marginal event-driven buyer exits. The discount floor widens — Nuveen/CEF Connect aggregates and Morningstar data put the historical reversion band at 100–300 basis points, benchmarked against the 2015–2018 window before the activist cycle began in earnest. That sounds like a loss for existing holders. In my view, it is structurally the opposite.

The cohort that loses is the flighty money: activists who needed a litigation exit to monetize. The cohort that wins is durable money: long-duration income investors who wanted the leveraged distribution structure to survive rather than get force-liquidated at a settlement mark. Fund boards facing fewer existential threats are more willing to maintain leveraged, higher-distribution structures — the income proposition strengthens, not weakens, when the threat of forced restructuring recedes. CEF holders obeyed the ruling; activist arb refused.

Saba and Bulldog migrate — not disappear. Expect more proxy contests under state corporate law, more concentrated pressure on BlackRock, Nuveen, and PIMCO complexes, and cross-border vehicles where U.S. activists carry less leverage. The strategy survives in narrower, slower form. The pace of forced discount compression slows. The duration of the income thesis lengthens.

Figure 2. CEF Activist-Targeted ETF (YYY) total return vs S&P U.S. Listed Closed-End Fund Index, indexed to 100 at Jan 2026

The trade:

Ticker: YYY (Amplify High Income ETF) — broad CEF exposure across the universe most affected by this ruling. The thesis is structural: the ruling removes the key downside catalyst — forced discount-narrowing via §47(b) litigation — and lets discounts revert toward historical bases while distribution coverage improves as boards operate under less governance pressure. Fixed-income CEFs trading 8%+ below NAV with leveraged distribution structures are the primary beneficiary; equity CEFs at managed-distribution funds where adviser autonomy drives yield policy are secondary.

Historical base rate: 2015–2018 saw CEF discounts in the 10–13% range when activist pressure was muted; 2022–2025 compressed that to 6–9%. Reversion toward the wider band over 12–24 months — 100–300 basis points of structural discount widening with durable income structures intact — is the central case.

Alternative angles: PIMCO Dynamic Income Fund (PDI) — large, leveraged, historically a Saba target — benefits directly from reduced rescission threat. BlackRock Science and Technology Term Trust (BSTZ) — term-trust mechanics now carry materially less rescission overhang. Nuveen taxable muni complex — adviser autonomy critical to distribution architecture, and it just got more defensible.

Where this thesis breaks: The SEC shifts enforcement posture and begins aggressive ICA enforcement that achieves the same discount-compression activists pursued via private litigation — same outcome through a different door. Or state-court proxy contests succeed at scale, returning bylaw pressure without needing §47(b) at all. The first 90 days post-ruling are the cleanest signal window; watch the Morningstar weekly discount-to-NAV close versus the 5-year average.

What I’m watching: First SEC public commentary on the June 11 ruling and whether the agency signals intent to fill the enforcement vacuum; Saba Capital’s 13D amendment filings across existing positions over the next 30 days for rhetoric shifts away from rescission language; whether any CEF board formally reverses a governance concession extracted under 2023–2025 settlement pressure; the CEF Connect weekly discount tracker for the equity-CEF universe — specifically equity versus fixed-income spread in the first post-ruling quarter; pace of new activist 13D filings into the CEF universe as a leading indicator of how quickly the strategy economics reprice.

Sources: - Supreme Court of the United States, FS Credit Opportunities Corp. v. Saba Capital Master Fund, decided June 11, 2026 (supremecourt.gov) - National Law Review, “Supreme Court Limits ICA §47(b) Private Rescission Claims,” June 18, 2026 - Investment Company Act of 1940, 15 U.S.C. §80a-46(b)

The Free Markets Report is provided by Lead-Lag Publishing, LLC for informational and educational purposes only and does not constitute investment, legal, accounting, or tax advice. Nothing herein is an offer to sell or a solicitation of an offer to buy any security. Specific securities mentioned are for illustration only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Readers should consult their own financial, legal, and tax advisors before making any investment decision. The author may hold positions in securities discussed.