Regulation Cuts and Inflation Relief: Can Deregulation Subdue Price Pressures?

Inflation has proven sticky.

Inflation has proven sticky. Prices for energy, housing and food soared, even as interest rates went up. The latest policy push from Washington, though, takes a different playbook: deregulation as relief on prices. The argument goes like this: cut the red tape, reduce production costs, increase supply and let markets do their magic. This wave of deregulation could unlock disinflation and growth for investors in key sectors.

A Supply-Side Solution to Inflation

The White House report “The Economic Benefits of Current Deregulatory Efforts” says that easing regulations could reduce long-term inflation by four-tenths to six-tenths of a percentage point a year. Policymakers estimate that the cost to households of the previous burden from past regulations was close to $50,000 on average. By taking the edge off those costs, the administration hopes to free up private investment, increase productivity and moderate price pressures — while not having to rely solely on monetary tightening.

And recent steps have bolstered that message. Starting in September and October, the Environmental Protection Agency and a half-dozen other agencies sought to repeal or rewrite dozens of rules, from those on energy efficiency and wind blowing over small streams to water control in the desert. The objective is simple, more energy and food supply at lower prices; feeding directly into disinflationary dynamics.

Energy: The First Beneficiary

Energy deregulation is the most obvious and direct inflation-fighting lever. Most recently, the EPA rescinded its decades-old “Reactivation Policy” that had discouraged reopening idled coal and gas plants. With data centers and electrification from artificial intelligence stoking demand for power to record levels, restarting the capacity is crucial to avoid shortages - and spikes in electricity cost. Looser permitting also makes it easier for new oil and gas projects to be completed more quickly.

The move has been cheered by industry leaders. The American Petroleum Institute described it as a response to voters who demand “affordable, reliable and secure energy”. Should producers have the freedom to drill and refine, that added supply can help contain fuel costs — which make up a good part of headline inflation. For investors, that means upside for energy producers, midstream infrastructure and utilities—all of which enjoy less regulatory friction and improved margins.

Agriculture: Lower Costs, Higher Output

Farmers are also major winners. By redefining federal water protections, the government eliminated costly permits for many thousands of farm ponds and ditches. Fresh guidance adds eliminating “coercive climate rules” that elevate food and fertilizer costs to the mix. These changes translate into more planting flexibility and lower compliance costs, which could boost crop yields and moderate food inflation. Agribusiness companies, makers of equipment like Deere and fertilizer producers would benefit from lower regulatory hurdles and higher exports.

Banks: Credit Growth and Capital Productivity

We are also now witnessing one of the most significant deregulatory transformations in the financial sector. Regulators are poised to lower the Supplementary Leverage Ratio (SLR)—a critical capital constraint—from about 5% to roughly 3.5%. The change allows banks to unleash billions of dollars in capital that had been sitting idle, and that can be used to generate new lending, investment and profits.

And if the capital increases under Basel III were to be made “capital neutral,” firms could free up more than $200 billion in excess equity for loan growth or shareholder returns, say analysts at JPMorgan. Deregulation might also pare back the huge compliance burden: an estimated 425 million paperwork hours a year, roughly equivalent to 26,500 full-time employees, complying with financial reporting rules.

For investors, simply put: This is bullish. Less strict capital rules equal fatter net interest margins, greater lending and bigger buybacks. A looser banking system can also help drive disinflation by amplifying supply — allowing new housing and business projects to be funded rather than halting them in their tracks through a credit shortage.

Lodging: Trimming the 25% Regulation Excess

Few markets illustrate inflation’s doggedness more clearly than housing. According to federal estimates, regulatory costs make up about 25% of the price of a new home. Delays, zoning barriers, and energy-efficiency requirements create a four-layer cake of expenses that drive costs along.

This is the bull’s-eye of the administration’s deregulation plan. The directives ask agencies to make housing more affordable and increase supply by, for example, postponing a number of Department of Energy appliance rules and moving forward with permitting reform. If those measures shave even a piece of the regulatory premium, homebuilders such as D.R. Horton, Lennar and Toll Brothers could benefit from better margins — and consumers from more affordable homes.

More subdued shelter inflation would likely be a powerful tailwind for the Fed’s policy outlook. And when the supply of shelter increases, renter pressure eases and rates might go lower more quickly, which would be good for real estate and rate-sensitive stocks.

Transportation: Red Tape on the Open Road

Transportation costs are still a central driver of inflation, and new flexibility on regulation just may enable that to turn around. The Department of Transportation’s pilot programs expand hours-of-service rules for truckers, letting them work more flexible driving schedules. The shift could boost productivity and decrease shipping delays, making supply chains more efficient.

Lower freight prices are felt throughout the economy. Logistics giants such as J.B. Hunt and Knight-Swift might see a bump in utilization, for example, while manufacturers and retailers cash in on lower delivery costs. More encompassing permitting changes like faster approvals of rail and port projects would also help avert future bottlenecks that result in spikes in inflation.

The Reason Deregulation Is Bullish for Markets

Unlike tightening money, which slows down demand, deregulation is an attack on inflation from the supply side. By reducing the cost and time to make goods, produce energy and build homes, policymakers are aiming for structural inflation’s roots. The result — if achieved competently — should be more output and lower prices, a combination that markets adore.

Key beneficiaries include:

Energy — Producers benefit from fewer emissions constraints and expedited permits, boosting production and profit margins.

Financials – Reduced capital rules give us more lending, buybacks and dividends.

Housing & Industrials – Builders and manufacturers will face lower compliance costs and fewer delays.

Small Businesses – Reduction of paperwork and regulatory costs makes these businesses more profitable and supports job creation.

For investors in stocks, that backdrop positive: inflation pressures ease even as corporate profits widen. If that inflation comes down as anticipated, the Federal Reserve may cut rates further—providing some valuation support across risk markets.

The Road Ahead

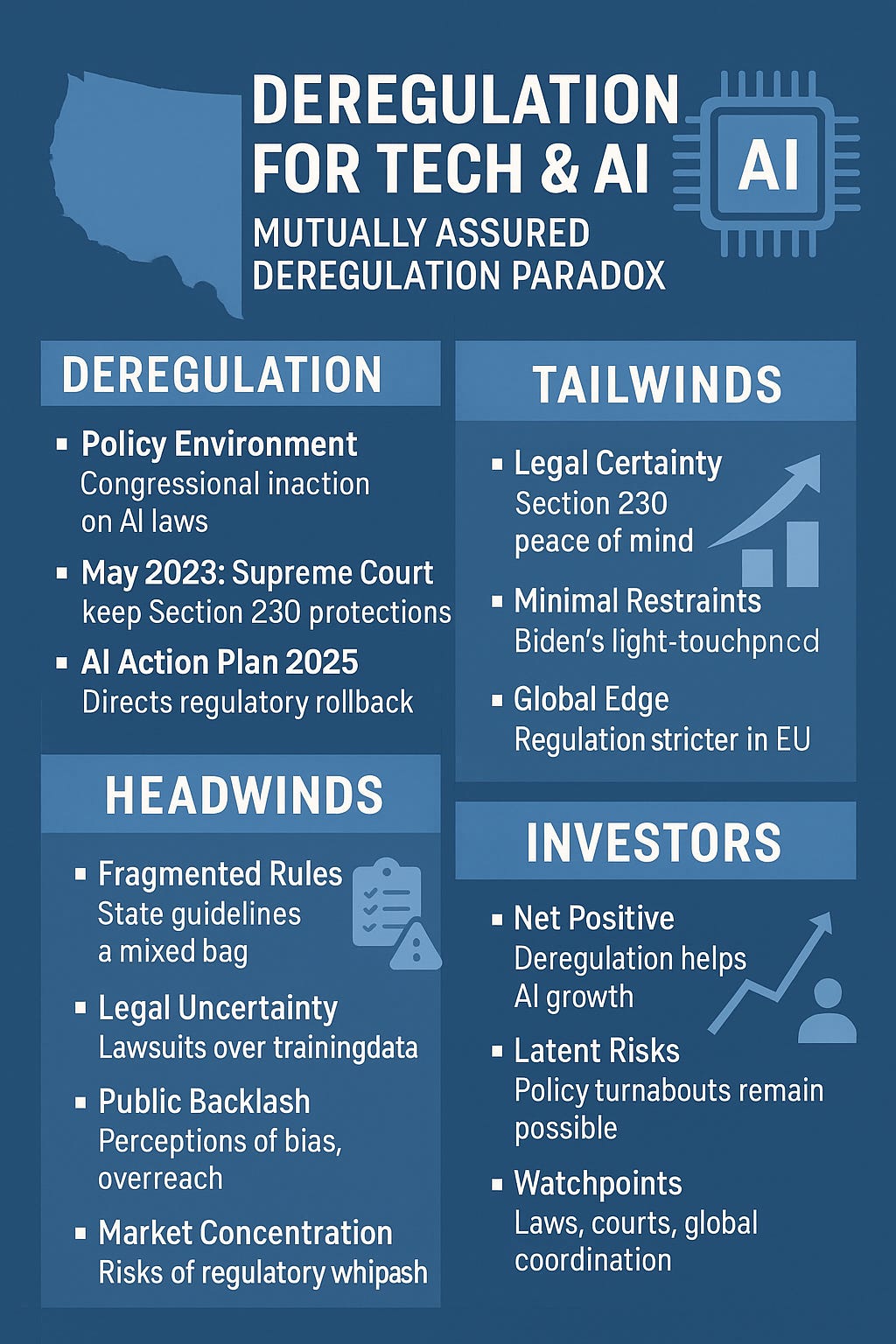

How fast these rollbacks are enacted are what investors should watch out for. Major moves — including the E.P.A. emissions revisions and bank-capital updates from the Fed — will play out through 2026, assuming court fights are likely. Also keep an eye out for additional areas: pricing reforms in healthcare, deregulation in tech and quicker approvals on infrastructure and artificial intelligence projects would represent further upside catalysts.

The takeaway is clear. Deregulation isn’t simply a political slogan — it’s also a macroeconomic accelerant. And by reducing structural costs and increasing supply, it is a way to fight inflation that monetary policy cannot achieve. The White House has said the reforms, if fully implemented, could save businesses and consumers almost $1 trillion over time.

For investors, that’s not just an efficiency gain — it’s an investment thesis. In a leaner, more unconstrained economy, after all, you get stronger earnings as well as higher valuations. After all, deregulation could easily become the missing ingredient of the next bull phase.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.