The Paradox of “Mutually Assured Deregulation”

Artificial intelligence has moved to the frontiers of economic power and political competition, and deregulation has been one of its most powerful tailwinds.

Artificial intelligence has moved to the frontiers of economic power and political competition, and deregulation has been one of its most powerful tailwinds. Policymakers in the United States have mostly refrained from enacting new, AI-specific laws that might prevent generative-AI developers, chipmakers and cloud providers from innovating. But the absence of guardrails that propels growth also magnifies legal, social and systemic risks. It’s an investment paradox; deregulation spurs the boom, but also creates volatility — or what analysts call “mutually assured deregulation.”

The Deregulatory Landscape, 2023–2025

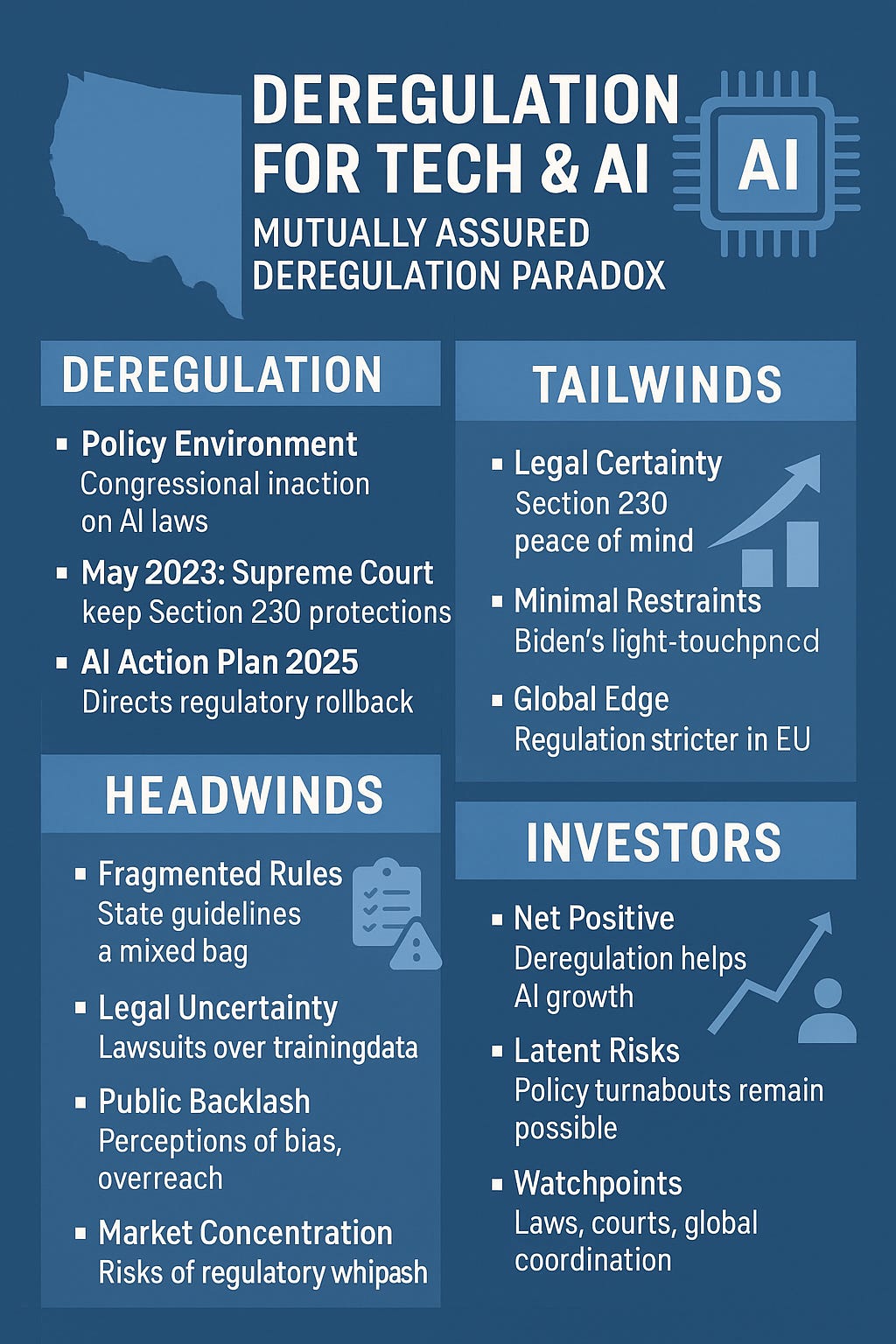

Regulatory swings have gone back and forth widely over the last two years. In 2023, the Supreme Court chose not to restrict Section 230 protections for platforms and upheld legal immunity around how algorithms recommend content. That ruling shielded a key protection for companies like Meta and Google reliant on AI-generated feeds. The same year, President Biden’s executive order on AI included voluntary standards for model safety and data transparency but shied away from enforcement.

The new administration instructed agencies to relax regulations identified as a “burden on AI innovation”. But efforts to ban states from writing their own AI laws failed in Congress, leaving instead a patchwork of local regulation. (Both Texas and Illinois have already imposed fines on Meta totalling more than $1 billion for biometric-privacy violations — a reminder that federal permissiveness doesn’t eliminate state-level risk.)

How Deregulation Powers Growth

Legal Certainty for Platforms - In failing to water down Section 230, courts preserved strong immunity for AI-generated or algorithmically presented content. This clarity reduced risk of litigation and spurred social-media and e-commerce platforms to double down on AI-driven personalization.

Minimal Federal Oversight - There is no U.S. law governing model size, use of compute or sources of data. Biden’s 2023 directive more emphasized research funding and voluntary standards than penalties. That lack of restraint aided and abetted generative-AI rollouts and capital formation. Venture investment in AI outstripped previous tech cycles, and cloud “hyperscalers” built infrastructure faster than at any time on record.

Explicit Policy Support - The 2025 AI Action Plan recast regulation as a barrier, directing the FTC and FCC to revisit previous judgments that “unnecessarily chill innovation”. Its message to markets was clear: Washington will prioritize speed over caution. Cloud providers and chipmakers got an immediate boost through looser permitting as well as expanded tax incentives for building data centers.

Competitive Advantage vs. Europe - And while the EU AI Act requires algorithmic transparency and risk assessments, the U.S. is still a relatively lax jurisdiction. Executives like Alphabet’s Sundar Pichai and OpenAI’s Sam Altman have contended that strict European regulations could drive investment to the United States. Vice President J.D. Vance’s 2025 statement that America had “AI innovation over EU bureaucracy” to thank, underscored the government position.

For investors, these dynamics mean powerful tailwinds — fatter margins for data-intensive companies, quicker product cycles and regulatory arbitrage in favor of U.S. listings.

When Deregulation Becomes a Headwind

Fragmented State Rules - Federal preemption’s defeat = 50 rulebooks. California and New York’s AI-ethics bills are a far cry from Texas’s emphasis on biometric data. Compliance costs are soaring, and lawsuits are multiplying. Uncoordinated regulation still bites, and Meta’s billion-dollar settlements are evidence.

Policy Whiplash - Within two years, American policy bounced from voluntary overview (Biden) to total deregulation (Trump). Such volatility complicates long-term planning. A future administration could re-impose restrictions, upending cost structures overnight. Investors must consider regulatory guidance as cyclical, not fixed.

Legal and IP Uncertainty - Because legislators have not defined limits on how data can be used, courts are now at the center. OpenAI, Microsoft and others are being sued by authors and artists in class actions for using copyrighted material without authorization as training data. Any unfavorable rulings could impose an expensive round of model retraining or licensing regimes — risks that are currently all but absent from valuations.

Public Backlash and Future Regulation - High-profile examples — from biased hiring algorithms to misbehaving chatbots — are driving demands for greater oversight. One AI-related tragedy or misinformation crisis could prompt the same kind of pendulum swing that followed the 2008 financial crash, when years of deregulation ceded to wholesale reform. Even the Federal Reserve’s Michael Barr has cautioned that “digital deregulation” could increase systemic risk.

Market Concentration - Lax antitrust enforcement may cement a few companies’ control of AI infrastructure. Short-term margins swell while long-term innovation can wither. Those political winds of change that blow when companies deemed too much like monopolies prompt regulation of a more aggressive sort are also just another repetitive headwind for investors.

The Global Feedback Loop: ‘Mutually Assured Deregulation’

The U.S. is not deregulating in a vacuum. China’s 2023 Interim Measures for Generative AI first introduced strict licensing, though those restrictions were loosened in an effort to “support tech development” and avoid falling behind the West. Britain has itself embraced the more “pro-innovation” regime, rather than the tighter approach taken by the EU.

This competitive calculus evokes Cold War deterrence — each country is terrified that if it squeezes down on regulations first, its rivals will gain an edge. Sam Altman and other executives here consistently cite the specter of “China 2030” — when many believe China will surpass the United States economically — as an argument against new regulation. The result is a race in which everyone gets faster — and no one becomes liable to slow.

The key takeaway for investors from this Mutually Assured Deregulation is twofold:

Tailwind, Long: Governments are likely to continue with their preference for growth and national advantage, further extending the AI boom. Anticipate continued subsidies, free export policies, and tolerance of data usage.

Increasing Systemic Risk: The lack of shared guardrails increases the probability of a major safety or geopolitical event — ranging from autonomous system failure to cross-border misinformation — that could prompt an abrupt regulatory crackdown and market correction.

Outlook for Investors

Deregulation is still a net-positive for short-term AI profitability. Cloud-service providers, chipmakers and software platforms derive benefits from less compliance friction and quickly scaling services. But investors should be aware that the policy risk is dormant, not gone.

The key here? Play the upside while hedging the regulatory downside. That could mean gravitating toward diversified tech conglomerates with the wherewithal to adjust compliance, or funds with exposure to both AI beneficiaries and defensive sectors that tend to perform during regulatory resets.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.