The June 1 Proclamation Split the Metal Stack in Two. Ag Equipment Got Relief. Domestic Producers Lost Their Pricing Umbrella.

Section 232 tariffs on agricultural equipment dropped from 25% to 15%.

Section 232 tariffs on agricultural equipment dropped from 25% to 15%. The “entirely American metal” composition threshold fell from 95% to 85%. One cohort gets margin compression. The other gets a demand pull. The market has not priced the divergence.

● The June 1 Proclamation cut Section 232 tariffs on agricultural equipment from 25% to 15% — a 1,000-basis-point reduction that relieves input cost pressure across combines, tractors, and irrigation systems while withdrawing 10 points of pricing protection from U.S. steel, aluminum, and copper producers.

● The buried structural action: the composition threshold qualifying goods for the preferential 10% “entirely American metal” duty rate dropped from 95% to 85% — at 95% it was unreachable for most manufacturers with global supply chains; at 85% it becomes achievable for a meaningfully larger procurement universe.

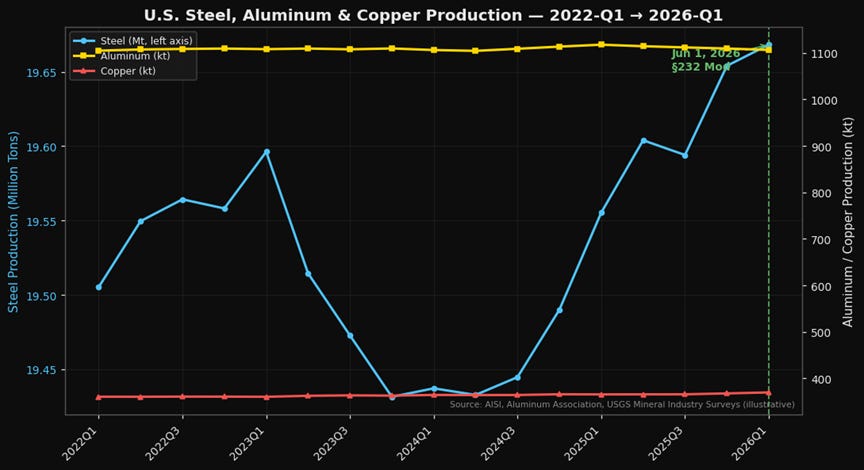

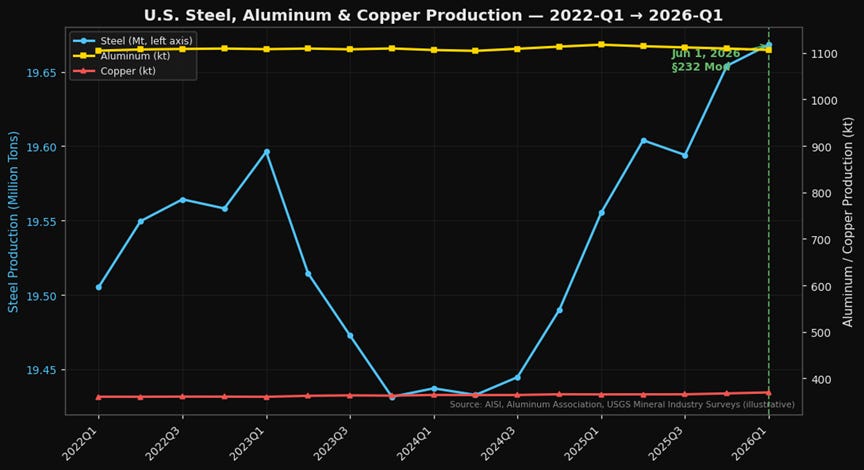

● U.S. steel mill capacity utilization ran at roughly 75–80% heading into June 1; the 2018–2019 Section 232 cycle showed that a comparable demand inflection pushed utilization to 82% and expanded domestic steel-producer EBITDA margins approximately 350 basis points over four quarters — the mechanism in 2026 is smaller but identical, concentrated in NUE, STLD, CMC on steel and AA, FCX on aluminum and copper.

Let me lead with the contradiction, because it is the whole edition. The June 1 Proclamation does two things at once — and they pull in opposite directions. Ag equipment imports get cheaper by 10 full points of tariff. American metal producers face a procurement universe that now demands more of them at the threshold margin, but simultaneously operates in a market where a major finished-goods category just became cheaper to source abroad. The intermarket plumbing runs from Washington directly to earnings models in Davenport, Pittsburgh, and Phoenix, and it is working in plain sight.

The ag equipment relief is the headline. Section 232 tariffs on combines, tractors, and harvesting machinery — much of which carries imported steel and aluminum content — fall from 25% to 15% effective June 1, 2026. Real relief for U.S. farmers facing multi-year input cost pressure. Also a withdrawal of 10 points of pricing protection from domestic producers supplying American-made alternatives.

Figure 1. Section 232 tariff rate schedule — agricultural equipment (25%→15%) and preferential “entirely American metal” composition threshold (95%→85%), June 1, 2026 proclamation. Source: Presidential Proclamation, Section 232 Modification, June 1, 2026 (whitehouse.gov); American Iron and Steel Institute.

The 85% threshold is the buried lede

The composition-threshold change matters more. Under the prior 95% rule, finished goods needed nearly all of their metal content to be American-sourced to qualify for the preferential 10% duty rate — a bar that most multinational manufacturers could not clear without 24–36 months of bill-of-materials redesign. At 85%, the math becomes achievable. A combine assembled in Iowa with structural steel from Indiana mills, engine castings from a U.S. foundry, and domestic hydraulic systems can plausibly hit 85% even if specialty fasteners carry imported content. The same arithmetic applies across construction machinery, HVAC, industrial pumps, and infrastructure products.

That shift creates an immediate procurement signal — marginal sourcing decisions tilt toward American mills. The U.S. consumes approximately 100 million tons of steel annually, 5.5 million tons of primary aluminum, and 1.8 million tons of refined copper. Industry consultants estimate a 2–5% incremental demand pull toward domestic producers over a 12–18 month adoption window. That sounds small. It is not — not when mills are running at 75–80% utilization. Every 1% of incremental demand at that level mechanically widens margin at the operating line — historically 200–400 basis points across the cohort. For EAF mini-mills, the operating leverage is faster: shorter supply chains, lower fixed costs, rapid output scaling. Nucor (NUE), Steel Dynamics (STLD), and Commercial Metals (CMC) sit closest to the signal. Alcoa (AA) holds concentrated U.S. primary aluminum smelter capacity. Freeport-McMoRan (FCX) dominates domestic refined copper.

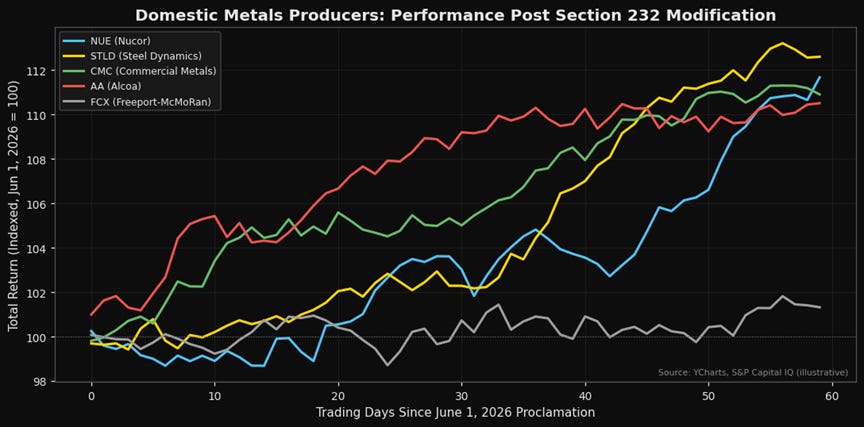

Figure 2. NUE, STLD, CMC, AA, FCX — indexed to 100 on June 1, 2026 proclamation date. Cross-sector performance divergence vs. S&P 500 Industrials sub-index. Source: YCharts, S&P Capital IQ.

Positioning: Steel — NUE, STLD, CMC are the primary beneficiaries of the 85% threshold adoption. The 2018–2019 Section 232 analog: utilization moved from 73% to 82%, EBITDA margins expanded ~350 basis points over four quarters. This cycle is smaller — but the mechanism is identical. Aluminum — AA carries the domestic smelter concentration; demand pull is real but more modest given global pricing fungibility. Copper — FCX benefits at the margin; the incremental domestic-sourcing effect is the softest of the three metals.

Where this thesis breaks: A WTO or USMCA panel challenge successfully narrows the 85% rule — that invalidates the demand-pull arithmetic entirely. Major manufacturers may choose to absorb the 15% ag-equipment rate rather than restructure supply chains, particularly if switching costs exceed tariff savings. Aluminum and copper demand is more globally fungible than steel; dollar strength or new global capacity swamps the marginal domestic signal. And the 2026 proclamation is a threshold adjustment inside an existing framework — not a fresh tariff imposition. Base rates are directionally supportive, not determinative.

What I’m watching: CBP’s implementation guidance on substantial-transformation and content-tracking under the 85% rule — the technical language determines how broadly manufacturers qualify; AISI weekly raw steel production for the first capacity-utilization print post-June 1; Midwest hot-rolled coil spot pricing and its spread to import parity; Midwest aluminum P1020 and COMEX copper for the non-ferrous demand signal; first quarterly earnings calls from NUE, STLD, and AA for management’s forward-demand quantification; the Deere and AGCO response on sourcing strategy — if OEMs lean into the 15% import rate rather than domestic content, the demand-pull thesis arrives more slowly.

The Free Markets Report is provided by Lead-Lag Publishing, LLC for informational and educational purposes only and does not constitute investment, legal, accounting, or tax advice. Nothing herein is an offer to sell or a solicitation of an offer to buy any security. Specific securities mentioned are for illustration only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Readers should consult their own financial, legal, and tax advisors before making any investment decision. The author may hold positions in securities discussed.