The CFPB Pulled the 2020 Advisory Opinion. Regional Banks Are Not All Equivalent Here.

Six paragraphs from the Bureau.

Six paragraphs from the Bureau. Five years of bank product development unwound. The divergence between large-balance-sheet regionals and thin-margin fintech competitors is the trade.

● On June 17, 2026, the CFPB rescinded its December 2020 advisory opinion on Reg B §1002.8 — the interpretation that authorized for-profit institutions to run protected-class-targeted Special Purpose Credit Programs under ECOA’s carve-out. Six paragraphs dissolved five years of bank product architecture.

● At peak in 2024, major U.S. banking institutions were originating an estimated $8–12 billion annually through SPCP pipelines across mortgage programs, minority small-business credit, and consumer products. Three pillars sustained that volume — regulatory safe harbor, CRA credit, reputational benefit. Only one remains fully intact.

● Prior CFPB rescissions under the current administration — the 1071 scale-back, payday lending guidance withdrawal, overdraft rule rescission — correlated with regional bank index outperformance versus the broader S&P 500 over the 60-day post-announcement window in 2025–2026. KBE and KRE are the sector read-through.

Let me frame this directly, because the compliance coverage misses what matters for positioning. The June 17 rescission is not primarily a social-policy event — it is a cost-structure event, and the impact is not symmetric across the regional bank cohort. Some institutions built SPCP programs as thin differentiation bets; others built them as compliance overhead dressed up as CRA credit generation. The rescission does not unwind them the same way. That asymmetry is the spine of this piece.

The mechanism

The Equal Credit Opportunity Act and Regulation B prohibit creditors from using race, color, national origin, sex, marital status, or age in credit decisions. Reg B §1002.8 carved out an exception — Special Purpose Credit Programs meeting statutory requirements and documented by a written plan. The December 2020 CFPB opinion extended that carve-out explicitly to for-profit organizations. Banks, fintechs, and CDFIs took it as a green light. From 2021 through 2025, dozens of institutions launched SPCPs: small-business programs aimed at minority-owned enterprises, mortgage products targeted at majority-minority census tracts, consumer credit lines built around protected-class eligibility criteria.

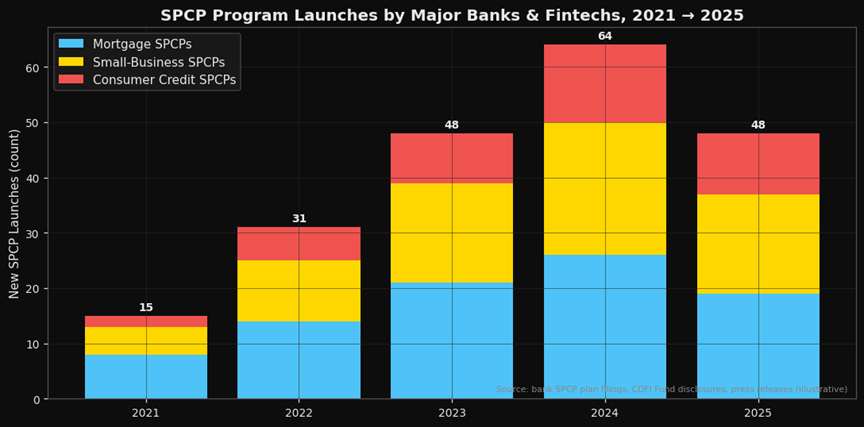

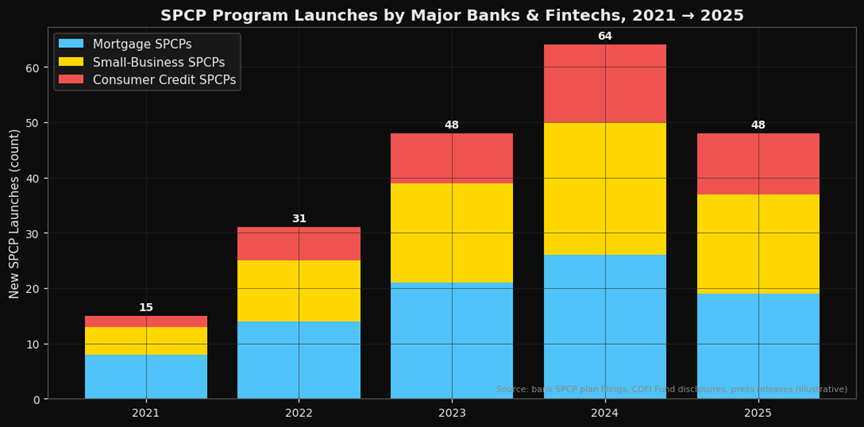

Figure 1. SPCP program launches by major banks and fintechs by year, 2021–2025. Stacked bar showing mortgage SPCPs, minority small-business SPCPs, and consumer credit SPCPs. Source: bank SPCP plan filings, CDFI Fund disclosures, press releases.

The June 17 notice does not repeal §1002.8 — the statutory carve-out survives. What the rescission removes is the interpretive safe harbor: the Bureau now states explicitly that programs using race, color, national origin, or sex as eligibility criteria do not align with ECOA “as currently interpreted.” Three consequences follow — and they land differently depending on where an institution sits in the market structure.

First, existing SPCPs lose their primary safe-harbor citation — programs can technically continue, but without the 2020 opinion’s examination cover. Second, the rescission is an enforcement-priority signal; consent orders in this category are no longer hypothetical tail risk. Third, this action is sequentially coherent: the 1071 small-business data-collection rule was scaled back in early 2026. The CFPB is methodically dismantling the Biden-era Reg B architecture — and SPCPs were the next piece.

The cross-cohort split

Large diversified banks — JPMorgan, Bank of America, Wells Fargo, Citigroup, the largest regionals — ran SPCPs where programs represented a small slice of total loan book. For them, SPCP compliance infrastructure was a cost center: legal review, written plan maintenance, fair-lending monitoring layered on top of programs that generated modest incremental revenue. The rescission removes that overhead. Net effect is modestly positive — deadweight compliance cost evaporates without a meaningful revenue hole.

The fintech consumer-lending cohort sits on the other side of that split. Lenders that built SPCP product lines as a differentiation mechanism — targeting protected-class addressable market as a growth thesis — lose the product’s legal foundation. Wind-downs will accelerate among fintechs running thinner compliance budgets. Where large banks quietly re-frame eligibility criteria around geographic and income-based proxies, fintechs face higher re-engineering costs relative to their revenue base. And plaintiff-side reverse-discrimination litigation gains traction now that the CFPB itself has destabilized the framework — that tail sits disproportionately on the fintech cohort.

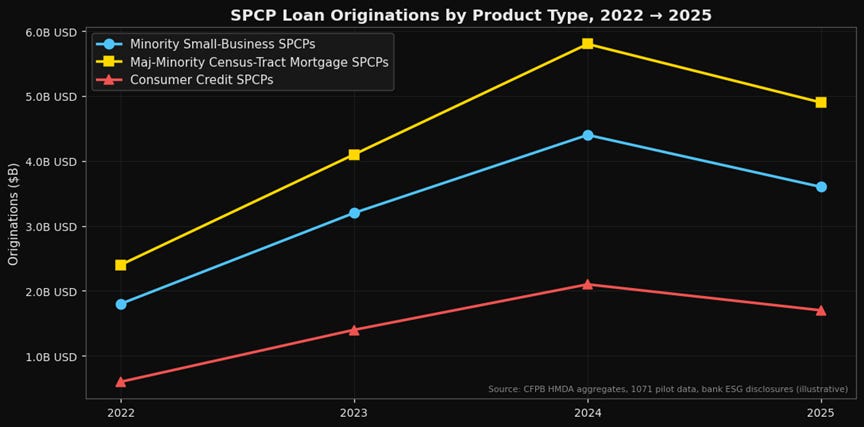

Figure 2. Estimated SPCP loan originations by product type, 2022–2025. Three lines: minority small-business SPCPs (light blue #4FC3F7), majority-minority census-tract mortgage SPCPs (gold #FFD700), consumer credit SPCPs (red #EF5350). Source: CFPB HMDA aggregates, 1071 pilot data, bank ESG disclosures.

Positioning

The trade: KBE (SPDR S&P Bank ETF) and KRE (SPDR S&P Regional Banking ETF) are the sector-level expression. The rescission removes a marginal cost-and-litigation overhang for large-bank SPCP operators and a marginal revenue base from fintech competitors that used SPCPs as a product differentiator — net directional pressure favors the large-balance-sheet cohort. The prior-rescission base rate in 2025–2026 supports a 60-day relative performance argument for KBE/KRE. Within the regional bank universe, the preference is balance-sheet-heavy regionals over lenders whose growth positioning leaned on SPCP origination volume.

Single-name angles: large universal banks with run-down SPCP programs — net positive; fintech consumer lenders with SPCP product lines — net negative; mortgage REITs with majority-minority census-tract loan exposure — neutral to slightly negative on origination volume.

Where this thesis breaks: State attorneys general fill the enforcement vacuum. California, New York, Illinois, and Massachusetts have signaled willingness to act under state-law parallels to ECOA. If a major state AG moves quickly, the federal safe-harbor removal gets replaced by fragmented state enforcement exposure — the compliance overhead does not disappear, it multiplies across jurisdictions. The large-bank cost-reduction thesis partially inverts in that scenario. Watch the first state AG action; it is the variable that most directly determines whether this is a clean deregulatory tailwind or a regulatory arbitrage problem.

What I’m watching: The first state AG enforcement action citing state-law ECOA parallels — that filing resets the entire cost calculus; the CFPB examination priority letter for H2 2026 — it will confirm whether SPCP examination pressure intensifies or redirects; any 8-K or public statement from a major bank modifying SPCP eligibility criteria — the clearest signal of how institutions are pricing residual litigation exposure; KBE and KRE 60-day relative performance versus S&P 500 financials — the prior-rescission base rate is the benchmark; fintech SPCP wind-down disclosures in Q3 2026 earnings calls — volume and tone reveal how deeply these programs were embedded in revenue models.

Compliance shifts are the slowest-moving high-conviction macro variable in markets — and the most consistently mispriced. A six-paragraph Bureau notice just moved through bank cost structures, fintech product lines, and litigation calendars simultaneously. The institutions that map that chain before the 60-day window closes are the ones positioned correctly.

Sources: - Consumer Financial Protection Bureau, Notice of Rescission, June 17, 2026 (consumerfinance.gov) - Compliance Alliance, “Equal Credit Opportunity (Regulation B); Special Purpose Credit Programs Rescission,” June 17, 2026 - Equal Credit Opportunity Act, 15 U.S.C. §1691 et seq. - 12 C.F.R. §1002.8

DISCLAIMER: The Free Markets Report is provided by Lead-Lag Publishing, LLC for informational and educational purposes only and does not constitute investment, legal, accounting, or tax advice. Nothing herein is an offer to sell or a solicitation of an offer to buy any security. Specific securities mentioned are for illustration only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Readers should consult their own financial, legal, and tax advisors before making any investment decision. The author may hold positions in securities discussed.