Interior Just Unlocked 92 Million Acres. The Outdoor Recreation Cohort Has Not Moved. That Divergence Is the Trade.

On June 19, 2026, the Department of the Interior proposed opening 1,450 new hunting and fishing access opportunities across 111 wildlife refuges and fish hatcheries — 92 million acres of federal land, one deregulatory stroke, and a cohort of public equities priced as if it never happened.

On June 19, 2026, the Department of the Interior proposed opening 1,450 new hunting and fishing access opportunities across 111 wildlife refuges and fish hatcheries — 92 million acres of federal land, one deregulatory stroke, and a cohort of public equities priced as if it never happened.

● The June 19, 2026 Interior proposed rule adds 1,450 new access opportunities — spanning 111 wildlife refuges and fish hatcheries — across 92 million acres of public land; the last time federal recreation access expanded at comparable scope, firearms and ammunition manufacturing output tripled within five years per Department of Commerce historical records.

● RGR, SWBI, and VSTO — the publicly traded firearms and ammunition manufacturers with direct exposure to hunting participation demand — have traded at a multi-year discount to the broader consumer discretionary universe through 2022–2025; the Interior rule is a structural participation tailwind that those multiples do not reflect.

● The U.S. Fish and Wildlife Service’s 2022 National Survey counted approximately 38 million Americans who hunted or fished that year; a 5–10% incremental participation rate over a multi-year window adds 2–4 million net new participants — and every new participant is a license sale, an ammunition purchase, and a capital goods decision.

Let me lead with the divergence, because it is the entire thesis. On June 19, 2026, the Department of the Interior announced a proposed rule that — if finalized — will open more than 1,450 new hunting and fishing access opportunities across 92 million acres of federal public land, spanning 111 wildlife refuges and fish hatcheries, while simultaneously simplifying more than 500 outdated regulations. That is a deregulatory access event of a scope this country has not seen in a generation. The publicly traded outdoor recreation cohort — RGR, SWBI, VSTO, JOUT, PII, ASO — has not moved in a way that prices it. The market is reading the headline. It is not reading the flywheel.

The 1953 analog and why it matters now

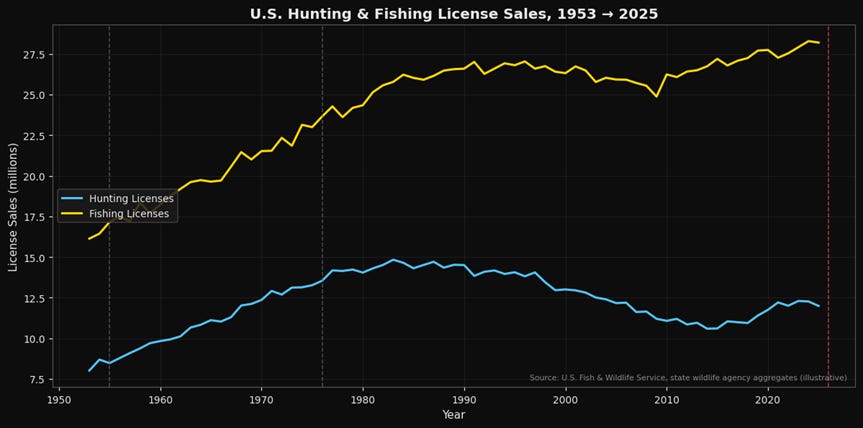

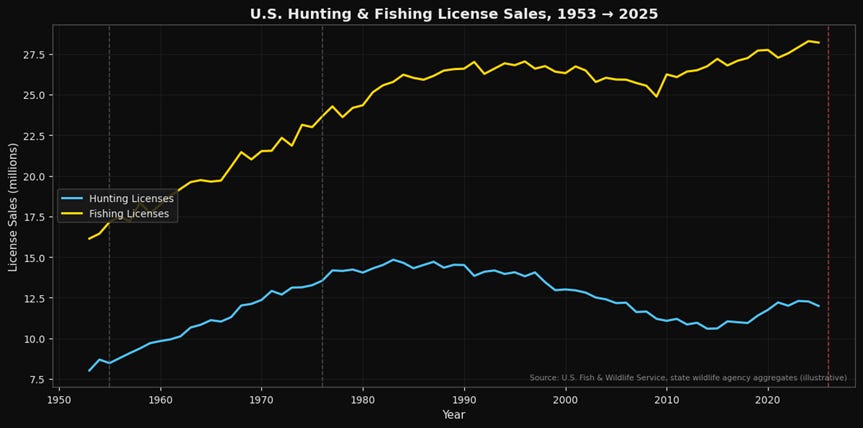

The structural template is 1953. The Eisenhower administration’s posture toward public lands access — combined with the Pittman-Robertson Act’s excise-tax-into-conservation flywheel and the Dingell-Johnson Act of 1950 channeling fishing-equipment taxes back into state agency infrastructure — created the conditions for the modern American outdoor industry. Federal land managers expanded hunting and fishing access across the National Wildlife Refuge System. State agencies built infrastructure on Pittman-Robertson and Dingell-Johnson revenues tied directly to participation. The economic compounding ran for three decades — hunting license sales tripled between 1953 and 1983; fishing license sales quadrupled; the precursors to what is now Federal Premium and the Remington Ammunition franchise were scaled entirely in that window.

The 2026 Interior rule is not 1953 in scope. There is no parallel highway buildout, no post-war demographic surge, no cold-start for the industry. In my view, that framing misses the point — because the 2026 cohort of public equities is dramatically more concentrated and more efficiently levered to incremental participation than the fragmented cottage industry of 1953 was. The operating leverage on marginal demand is higher now, not lower. A 5% participation lift hits RGR’s and SWBI’s capacity utilization in a way it simply could not have hit Winchester in 1955.

The rule implements President Trump’s January 2025 Executive Order 14192, “Unleashing Prosperity Through Deregulation,” and Secretary Doug Burgum’s January 2026 directive ordering the Interior Department to remove barriers to hunting and fishing access. The regulatory direction is clear, and it is durable.

The mechanism — three channels, one flywheel

Figure 1. Annual U.S. hunting and fishing license sales, 1953–2025 — two-line chart (hunting: light blue #4FC3F7; fishing: gold #FFD700), with vertical annotations marking the 1953–55 access expansion, the 1970s land management acts, and the June 19, 2026 Interior proposed rule date. Source: U.S. Fish and Wildlife Service, state wildlife agency aggregates.

Channel one is direct participation. Expanded access drives license sales — the leading indicator every equipment manufacturer watches before setting production targets. License revenues fund state agency infrastructure that compounds participation further. The USFWS 2022 baseline is 38 million hunters and anglers. A 5–10% multi-year increment is not optimistic — it is roughly what the 1953–58 expansion delivered in its first cycle.

Channel two is destination travel. Newly accessible refuges and hatcheries become trip destinations — outdoor travel spend flows toward the Mountain West, Upper Midwest, and Gulf Coast states where the 1,450 new opportunities are concentrated. Wyoming, Montana, Idaho, Alaska, Mississippi, Louisiana, and Alabama capture the largest share.

Channel three is equipment refresh. Access expansion pulls forward replacement demand and lifts per-participant spend. An angler newly accessing a federal refuge is not neutral on electronics. That is a Minn Kota or Humminbird decision — a JOUT revenue event.

Three channels, one flywheel. The market is pricing channel one at the margin and ignoring channels two and three.

The cohort

The publicly traded outdoor equipment cohort is small, concentrated, and — in my view — mispriced relative to the regulatory tailwind now in front of it.

RGR (Sturm, Ruger & Co.) is the pure-play publicly traded firearms manufacturer — conservative balance sheet, high free cash flow conversion, hunting rifle exposure that maps directly to incremental participation demand. SWBI (Smith & Wesson Brands) carries hunting and sporting rifle positioning. VSTO (Vista Outdoor) — restructured through its 2024–2025 split — holds the dominant U.S. ammunition franchise: Federal Premium, Remington Ammunition, CCI, Speer. Ammunition is the consumable. Every incremental hunter is a recurring VSTO revenue unit, not a one-time capital event. JOUT (Johnson Outdoors) operates Minn Kota and Humminbird — the dominant fishing electronics franchise. PII (Polaris) is the off-road vehicle category; the access expansion drives ATV and side-by-side demand among hunters reaching newly opened terrain. ASO (Academy Sports & Outdoors) is the largest publicly traded outdoor specialty retailer — the channel through which most of the equipment spend flows.

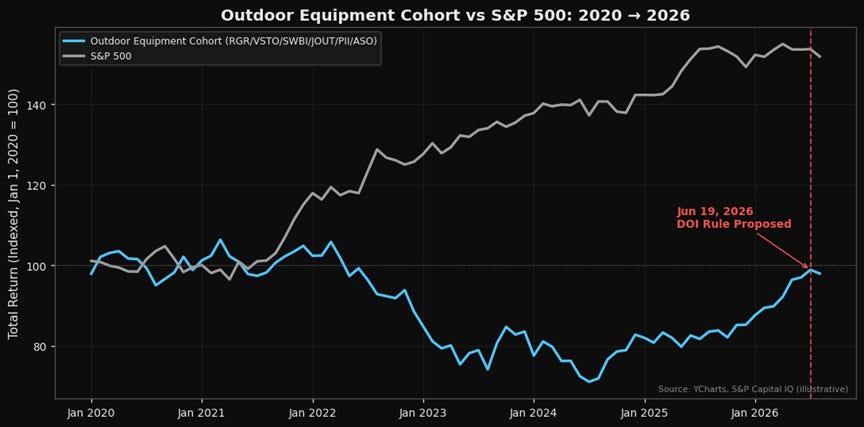

Figure 2. Indexed total return of the public-equity hunting and fishing equipment cohort (RGR, SWBI, VSTO, JOUT, PII, ASO equal-weighted) vs. S&P 500 Consumer Discretionary Select Sector (XLY), January 2020–June 2026. Vertical annotation at June 19, 2026 Interior rule proposal date. Source: YCharts, S&P Capital IQ.

The cohort traded at a persistent discount to broader consumer discretionary from 2022 through 2025 — a combination of ESG-driven institutional aversion, post-COVID inventory normalization, and softer younger-demographic recruitment trends. That discount has not closed. The Interior rule introduces a structural participation tailwind that is categorically different from the post-COVID demand normalization the market is still pricing. The cohort’s operating leverage on incremental demand is high. The multiples do not reflect it.

Positioning

The trade: The primary beneficiary tier is firearms and ammunition — RGR, SWBI, VSTO. These three companies hold the most direct, highest-margin operating leverage to incremental hunting participation: a new hunter is an ammunition buyer first, a capital goods buyer second, and a recurring customer thereafter. The secondary tier is outdoor electronics, off-road vehicles, and retail channel — JOUT, PII, ASO — where the access expansion is a tailwind but the demand path is less direct and the timeline is longer. Historically, the 1953–58 access expansion correlated with a roughly 3x increase in U.S. firearms and ammunition manufacturing output over a five-year window per Department of Commerce historical data. The 2026 expansion is smaller in scope, but the cohort response function is structurally similar — operating leverage on incremental demand is higher now than it was then.

There is no clean sector ETF for this exposure. The Consumer Discretionary SPDR (XLY) holds the outdoor cohort as a small, diffuse component — direct single-name positioning is cleaner. A long basket weighted toward RGR and VSTO as primary positions, with JOUT and ASO as secondary positions, captures both the direct demand pull and the channel distribution.

Where this thesis breaks: Federal court injunction during the comment and finalization period eliminates the near-term participation catalyst — and litigation risk here is not theoretical. Demographic headwinds are real: hunting participation among adults under 35 has been structurally negative since the mid-2000s, and access expansion alone does not reverse that without state agency outreach investment. State wildlife agencies that lack capital for refuge and hatchery infrastructure fail to operationalize what the federal rule opens — the regulation opens the door; the states have to build the path. Broader consumer discretionary pressure — credit contraction, a hard landing — compresses available multiple expansion regardless of the fundamental tailwind.

What I’m watching:

The Interior rule’s comment period schedule and any early signals from federal court on injunction filings; state wildlife agency budget allocations in Wyoming, Montana, Idaho, Alaska, Mississippi, Louisiana, and Alabama — the access expansion is only as durable as the infrastructure spending behind it; USFWS quarterly license-sale data — leading indicator, not lagging; RGR and SWBI forward production guidance in the next earnings cycles; ASO comparable-store sales for the hunting and fishing category in the back half of 2026; any legislative reinforcement of EO 14192 that would insulate the rule from court challenge; JOUT’s fishing electronics order book — the first place new-participant demand shows up in reported numbers.

The 1953–58 access expansion created the modern outdoor recreation industry from structural conditions that rhyme — not replicate — with 2026. The cohort is smaller, more concentrated, and more efficiently levered to incremental demand than anything that existed in 1953. The market priced the headline on June 19. It has not priced the five-year flywheel. That gap — in my view — is where the durable money will eventually find its grip.

The Free Markets Report is provided by Lead-Lag Publishing, LLC for informational and educational purposes only and does not constitute investment, legal, accounting, or tax advice. Nothing herein is an offer to sell or a solicitation of an offer to buy any security. Specific securities mentioned are for illustrative purposes only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Readers should consult their own financial, legal, and tax advisors before making any investment decision. The author may hold positions in securities discussed.