FMCSA Killed a Decades-Old CDL Compliance Burden. The Tech-Enabled Fleet Wins. The Legacy Compliance Moat Doesn't.

The Federal Register publishes the final rule June 22, amending 49 CFR Parts 383 and 384.

The Federal Register publishes the final rule June 22, amending 49 CFR Parts 383 and 384. The administrative saving is modest. The compounding signal to the trucking technology investment thesis is not.

● FMCSA final rule effective July 22, 2026 removes the 30-day CDL self-reporting requirement — a pre-electronic-era administrative layer that electronic SDLA data-exchange has made redundant since 2024; FMCSA classified the action under E.O. 14192 and determined total costs are “less than zero.”

● Six FMCSA deregulatory actions in 14 months — ELD recordkeeping, HOS flexibility, medical certification, clearinghouse query costs, electronic pre-employment vetting, and now CDL self-reporting — each one systematically retiring a paper-era compliance layer and shifting the regime toward the electronic infrastructure that IOT, PWFL, and TRMB already own.

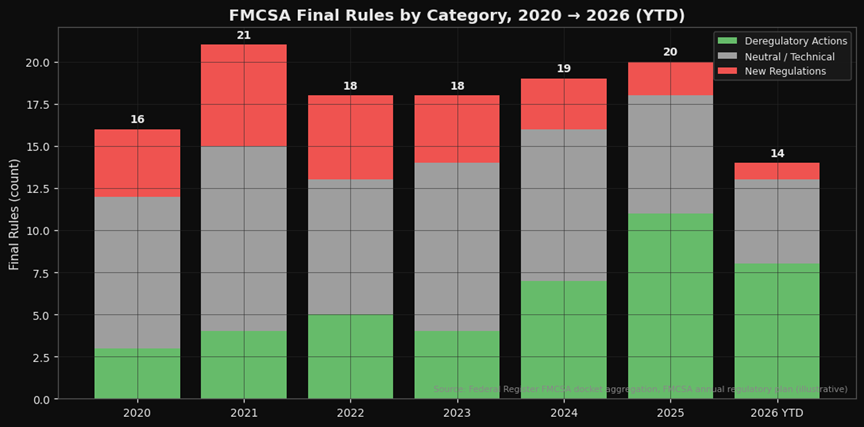

● The 2017–2020 ELD mandate window saw fleet management per-truck pricing expand approximately 18% and category installed-base grow from ~40% penetration to over 90%; the current FMCSA deregulatory pattern is the second inflection, and the market is pricing fundamentals — not the regulatory accelerant.

The divergence worth tracking is not between carriers. It is between two businesses sharing a truck — one hauls freight, the other runs the compliance and telematics infrastructure that determines whether moving is legal. When FMCSA retires paper-era compliance layers, the carrier’s administrative burden compresses — but the platform’s irreplaceability expands. That asymmetry is the cross-cohort tension the June 22 rule is signaling.

The final rule amending 49 CFR Parts 383 and 384 publishes June 22, 2026, effective July 22. FMCSA eliminates the requirement that CDL holders self-report traffic convictions to their state licensing agency within 30 days — the same data already moves automatically between State Driver Licensing Agencies under an integrated electronic system fully operational since 2024. The redundant attestation step is removed. Per Federal Register docket FMCSA-2025-0111 (RIN 2126-AC85), the action produces net savings to the regulated industry. Total costs: less than zero.

Figure 1. FMCSA deregulatory actions by category, 2020–2026 — stacked bar chart showing the acceleration of paper-to-electronic compliance transitions, with the six 2025–2026 deregulatory rules highlighted. Source: Federal Register FMCSA docket aggregation; FMCSA Unified Agenda.

The rule itself does not move a stock. The pattern behind it does. Six FMCSA deregulatory actions in 14 months — ELD recordkeeping streamlining (April 2025), hours-of-service flexibility (June 2025), medical certification simplification (September 2025), clearinghouse query-cost reduction (December 2025), electronic pre-employment vetting (February 2026), CDL self-reporting removal (June 2026) — each following the same mechanical logic: retire the paper attestation layer, recognize the electronic system as sufficient, reduce incremental administrative cost per truck. Every rule that retires a paper step mechanically lowers compliance cost per truck — and simultaneously raises the switching cost of the platform that replaced it.

The trucking technology thesis has always rested on regulatory stickiness. ELD mandates forced adoption. Supply chain disruption accelerated penetration. The 2025–2026 FMCSA sequence does something more durable — it makes the electronic platform the regulatory baseline itself, the mechanism through which compliance now legally occurs. That is a moat being written into the CFR.

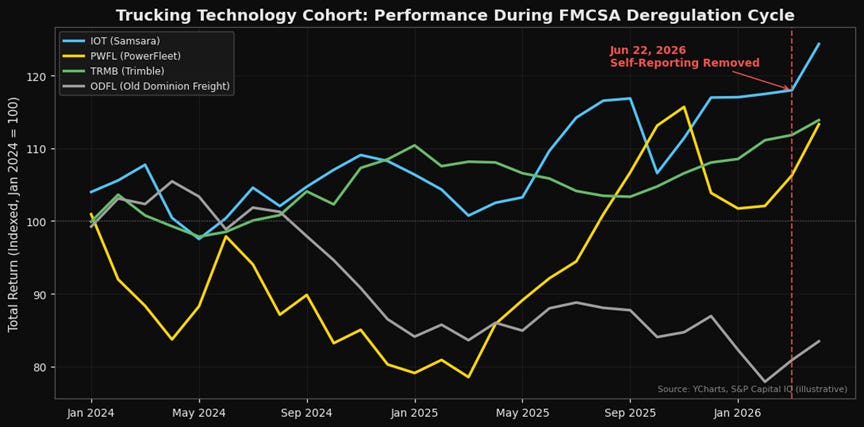

The trade: Long the tech-enabled fleet management cohort — Samsara (IOT) as the dominant pure-play, PowerFleet (PWFL) as the telematics second position, Trimble (TRMB) on its Transportation segment. Old Dominion (ODFL) sits in a different column — best-in-class carrier already running an electronic-first compliance stack, capturing margin relief directly rather than collecting subscription fees. Pair trade: long IOT and PWFL against spot-market-sensitive legacy carriers carrying heavy paper-era compliance infrastructure and weak balance sheets. Historical base rate: the 2017–2020 ELD mandate window saw per-truck pricing expand ~18% and installed-base nearly double from 40% to over 90% penetration. The current FMCSA deregulatory sequence is a second-order version of that same dynamic, compounding into an already-penetrated base.

Figure 2. Indexed total return — trucking technology cohort (IOT, PWFL, TRMB) vs. S&P 500 and Dow Jones Transportation Average, 2020–2026. Source: YCharts, S&P Capital IQ.

Where this thesis breaks: Regulatory deference to electronic systems assumes those systems stay reliable and interoperable — a material SDLA data-exchange failure, or a successful legal challenge to E.O. 14192, stalls the sequence. Samsara’s valuation is rich on standard SaaS metrics; the thesis requires sustained per-truck pricing momentum and fleet-count growth. Trucking volume weakness compresses subscription growth faster than the regulatory tailwind can offset. And legacy carriers do not simply disappear — some will modernize fast enough to rebuild the moat on their own terms.

What I’m watching: The July 22 petition-for-reconsideration window — any organized carrier-industry challenge is the first signal the deregulatory sequence stalls; Samsara’s next earnings call for ARR per customer and net revenue retention; FMCSA’s 2026 annual regulatory plan release for the next actions in the pipeline; trucking spot and contract rate progression as the fleet-size leading indicator; ODFL’s next operating ratio as a read on whether compliance-cost compression is reaching carrier margins.

The Free Markets Report is provided by Lead-Lag Publishing, LLC for informational and educational purposes only and does not constitute investment, legal, accounting, or tax advice. Nothing herein is an offer to sell or a solicitation of an offer to buy any security. Specific securities mentioned are for illustrative purposes only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Readers should consult their own financial, legal, and tax advisors before making any investment decision. The author may hold positions in securities discussed.