EO 14411 Is a Customs Enforcement Earthquake. The Importer of Record Just Became a Strict-Liability Position.

Trump’s June 3 executive order strengthens CBP enforcement penalties, expands disclosure requirements, and prioritizes forced-labor, misclassification, undervaluation, and transshipment cases.

Trump’s June 3 executive order strengthens CBP enforcement penalties, expands disclosure requirements, and prioritizes forced-labor, misclassification, undervaluation, and transshipment cases. The cost stack for U.S.-bound imports just got steeper — and the customs broker, trade compliance, and bonded warehouse universe just became a structural growth story.

● EO 14411, signed June 3, 2026, gives CBP a 90-to-180-day mandate to raise penalty multipliers, tighten importer-of-record oversight, and prioritize forced-labor and transshipment enforcement — the compliance-software TAM is estimated to expand 18-25% inside that window alone.

● Pre-EO, all-in customs compliance cost ran $14-22 per $1,000 of declared value for mid-size importers; for a $500 million annual import program, the incremental compliance drag over the next 12 months could reach $1-3 million — that cost transfers directly to the services layer.

● Descartes Systems Group (DSGX) saw revenue-per-importer-customer expand approximately 14% across the 2018-2020 Section 301 implementation cycle; EO 14411 represents a deeper regulatory shift, and the comparable lift this cycle is likely larger.

Let me lead with the contradiction, because it is the entire thesis. EO 14411 — “Strengthening Customs Enforcement,” signed June 3, 2026 — comes from the same administration that has cut regulations across energy, finance, and permitting at a rate unseen in recent memory. And yet here is an executive order that materially raises the regulatory burden on every importer of record in the United States. That is not cognitive dissonance — it is the enforcement logic of the tariff regime the administration has spent 18 months building. The tariff schedule sets the price. EO 14411 makes evasion expensive enough that the price actually holds. What looks like a deregulatory contradiction is in fact the load-bearing wall of the entire trade architecture — and the supply chain plumbing that moves goods through that architecture just became a different business.

Five Levers, One Direction

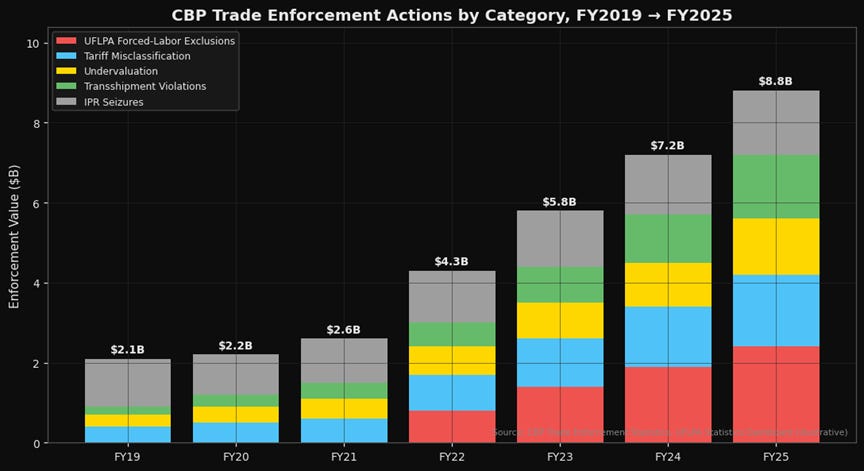

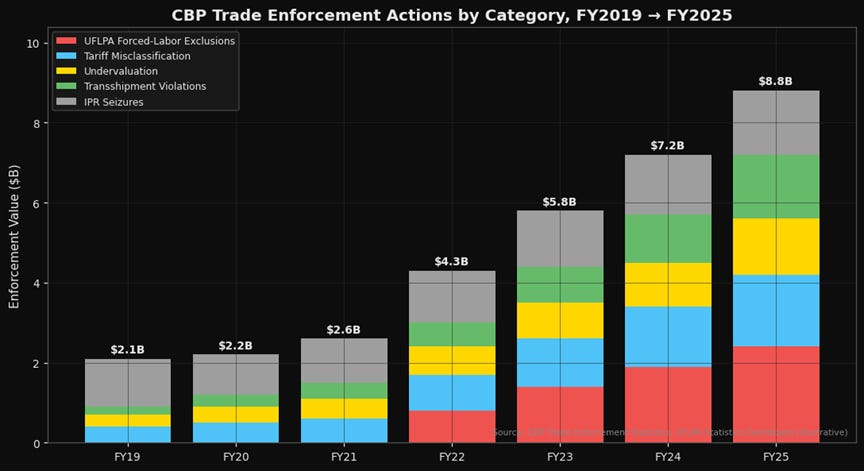

Figure 1. Annual CBP enforcement actions by category, FY2019–FY2025 — stacked bar: forced labor exclusions (UFLPA), tariff misclassification cases, undervaluation cases, transshipment violations, IPR seizures, total enforcement value annotated per bar. Source: CBP Trade Enforcement Statistics, UFLPA Statistics Dashboard.

The order operates through five enforcement levers — each aimed at a different point of leakage in the current import system.

Forced labor exclusions. The Uyghur Forced Labor Prevention Act has been on the books since 2022, creating a rebuttable presumption that Xinjiang-origin goods are produced with forced labor and barred from entry. CBP has detained roughly $4 billion in shipments under UFLPA since enactment. EO 14411 directs active prioritization — which translates, operationally, to an expanded entity list and a materially lower threshold for shipment detention. Every shipment with Xinjiang-adjacent supply chain exposure now runs a higher clock risk.

Tariff misclassification. Section 232, Section 301, and IEEPA tariffs are now stacked across steel, aluminum, copper, semiconductors, EVs, and a long tail of consumer goods. The incentive to misclassify imports under lower-duty HTS codes has never been higher — and CBP’s prior response, post-entry audits with negotiated settlements, was effectively a cost of doing business. EO 14411 changes the arithmetic: higher penalty multipliers, expanded summary forfeiture authority, and IOR personal liability for systematic misclassification. This is not a marginal change in enforcement tone. It is a structural shift in who bears the liability.

Undervaluation. Particularly relevant for de minimis shipments — those under the $800 threshold — and for related-party transactions where transfer pricing compresses declared customs value. EO 14411 directs CBP to expand value-verification authority. The de minimis loophole that powered the Shein and Temu logistics model was already partially closed by congressional action; EO 14411 eliminates the operational backstop that remained.

Transshipment. Goods routed through Mexico, Vietnam, Malaysia, or Thailand to evade Chinese-origin tariffs are the single largest category of duty-evasion enforcement growth. EO 14411 directs origin-verification audits at scale and tightens country-of-origin-marking enforcement — with aggressive expansion of substantial-transformation tests. The country-of-origin arbitrage that drove much of the post-2018 supply-chain rerouting just became dramatically more expensive to run.

IOR oversight. The importer of record is the legal entity responsible for paying duties and meeting all customs obligations. EO 14411 explicitly calls for tighter IOR oversight — which signals higher bonding requirements, stricter ACE portal compliance, and what is likely a CBP-published high-risk IOR list subject to enhanced scrutiny. The importer of record just became a strict-liability position in a way it has not been since pre-2001.

The Cost-Stack Arithmetic

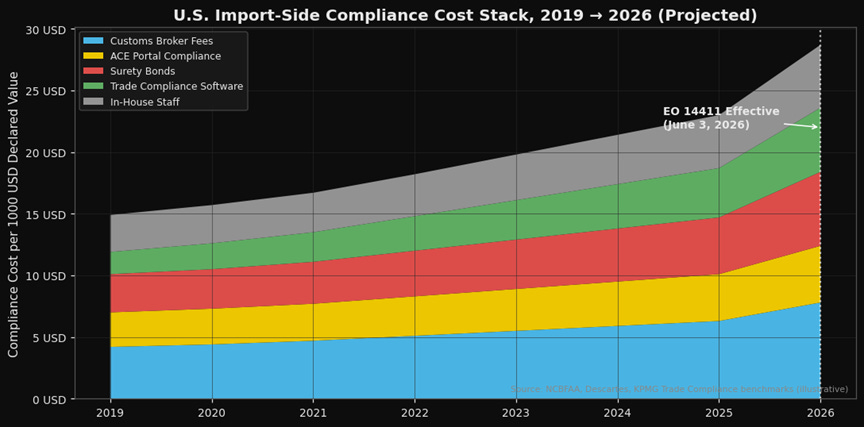

Figure 2. U.S. import-side compliance cost per $1,000 of declared customs value, 2019–2025, with EO 14411 implementation projection — line chart, components labeled: customs broker fees, ACE portal compliance, surety bonds, trade compliance software, in-house staff. Source: NCBFAA annual surveys, Descartes, KPMG Trade Compliance benchmarks.

The numbers are not speculative — they are compounding. Before EO 14411, all-in customs compliance cost ran $14-22 per $1,000 of declared value for mid-size importers, and $8-12 for the largest enterprise importers. The 90-to-180-day implementation window is estimated to push surety bond requirements for high-risk IORs up 25-40%. Broker fees rise as the work content per entry expands. Compliance software spend accelerates as importers race to automate the new disclosure requirements.

For a $500 million annual import program — the scale of a mid-market consumer goods importer — the incremental compliance cost over 12 months runs $1-3 million. For the largest importers running $10-50 billion annually, the incremental drag lands in the tens of millions. That cost does not disappear. It lands somewhere — passed through to consumers as margin-defending price increases, absorbed as margin compression, or converted into capex on supply-chain restructuring. In every scenario, the services and infrastructure layer collecting that spend wins.

The lesson supply chains are teaching this week is the oldest one in trade: when the regulatory toll rises, the toll-booth operators do well.

Tech-Enabled vs. Traditional — The Clean Divergence

This is where the investment thesis sharpens. The customs and logistics universe is not a monolith — it bifurcates cleanly between tech-enabled compliance infrastructure and traditional broker-forwarder generalists, and EO 14411 widens the gap between them.

Trade compliance software is the purest expression of the structural tailwind. Descartes Systems Group (DSGX) runs the leading global trade content and compliance platform — and DSGX is not a speculative beneficiary here. It is the literal database layer that importers use to classify HTS codes, screen UFLPA entity lists, verify country-of-origin rules, and automate the ACE portal disclosures that EO 14411 is expanding. Compliance-software TAM is estimated to grow 18-25% inside the implementation window per industry analyst frameworks. The 2018-2020 Section 301 cycle expanded DSGX’s revenue per importer customer approximately 14%; EO 14411 is a deeper, more comprehensive regulatory shift.

Expeditors International (EXPD) is the largest pure-play publicly traded customs broker and freight forwarder. EXPD does not compete on price — it competes on brokerage precision and compliance quality — which means a rising compliance burden is, mechanically, a rising-revenue environment for EXPD. The volume and price-per-entry tailwind is direct. EXPD’s margin structure rewards complexity.

C.H. Robinson (CHRW) is the more mixed picture — and the divergence within the divergence. CHRW carries material customs brokerage exposure that benefits from EO 14411, but its spot trucking business operates on a different clock entirely, decoupled from compliance-cycle dynamics. CHRW is not the clean long here. It is a managed position: brokerage segment benefits, freight segment neutral-to-negative on domestic demand softness.

On the other side — the direct-to-consumer cross-border e-commerce platforms built around de minimis shipment volumes face accelerating structural pressure. The administration explicitly views the Shein and Temu model as a dual risk vector — duty evasion and forced-labor exposure. EO 14411’s IOR oversight provisions are not written around these platforms, but they land on them directly.

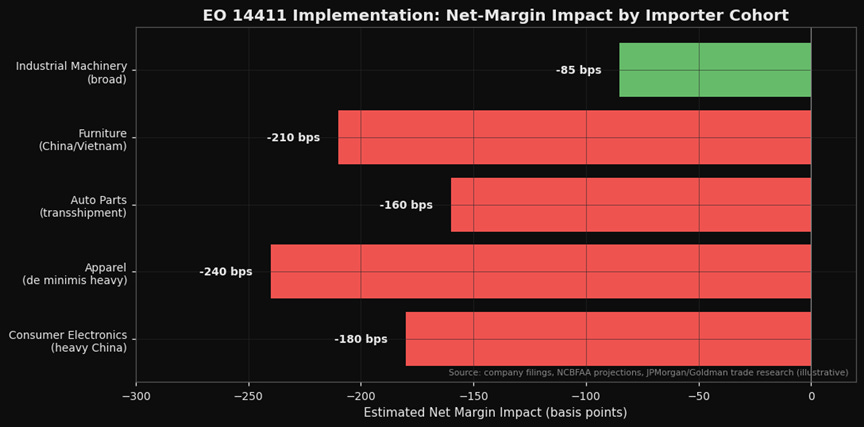

Figure 3. Estimated EO 14411 impact on net margin of representative importer cohorts — horizontal bar chart: consumer electronics (heavy China exposure), apparel (heavy de minimis exposure), automotive parts (heavy transshipment exposure), furniture (mixed China-Vietnam exposure), industrial machinery (broad exposure). Source: company filings, NCBFAA cost projections, JPMorgan and Goldman trade-compliance research.

Consumer electronics retailers with concentrated China exposure face the steepest margin mark-up. Apparel and footwear importers that depend on de minimis shipments lose volume and absorb higher per-unit compliance costs simultaneously. Automotive parts distributors with Vietnam and Mexico transshipment exposure face origin-verification audits at scale. Furniture importers with mixed China-Vietnam supply chains face substantial-transformation litigation. These are not tail risks — they are the direct mechanical output of the five enforcement levers above.

The Macro Read-Through

EO 14411 is the operational backbone of the tariff regime — the enforcement teeth that make the 2025-2026 tariff schedule something other than a revenue paper tiger. The net effect raises effective duty collection per dollar of declared customs value. That is incrementally inflationary on affected imported consumer goods — not dramatically, but persistently. It is structurally bullish for U.S.-based manufacturing where the duty differential is now harder to arbitrage around. And it is a clean multi-year tailwind for the trade compliance infrastructure layer that the market has not yet fully repriced into 2026-2027 consensus estimates.

The market is still trading the headline tariff numbers. It has not yet absorbed the implementation arithmetic.

Positioning:

Long — Trade compliance infrastructure: - DSGX (Descartes Systems Group): The purest direct beneficiary — HTS classification, UFLPA screening, ACE portal automation, country-of-origin rules-of-origin databases. Revenue per importer customer expanded ~14% in the 2018-2020 Section 301 cycle. EO 14411 is a more comprehensive shift; the comparable lift this cycle is likely larger. Historical base rate supports a multi-year revenue expansion story. - EXPD (Expeditors International): Large customs brokerage and freight forwarder with a high-margin, compliance-quality business model. Volume and price-per-entry tailwind is direct. Rising complexity is EXPD’s revenue engine. - CHRW (C.H. Robinson): Mixed thesis — customs brokerage segment benefits from the compliance tailwind; spot trucking segment operates on a different and less favorable clock. Position in CHRW is sized smaller; it is the blended-exposure name in the basket, not the clean long.

Pair trade: Long DSGX / Short cross-border e-commerce platforms with de minimis dependence. The compliance-cost spread between sophisticated importers using tech-enabled brokerage and de minimis-dependent platforms widens materially under EO 14411. DSGX’s revenue expands as the compliance regime deepens; de minimis-dependent platform economics compress on the same timeline. The divergence has not been priced.

Risk paragraph: CBP under-implements the EO during the 90-180 day window — enforcement language does not translate into actual audit volume expansion. Congress passes legislation that softens specific IOR liability provisions. The IOR oversight framework gets enjoined in litigation by an importer coalition. Watch CBP’s implementation guidance, expected July-August 2026; watch NCBFAA member alerts; watch DSGX’s first earnings call post-implementation for forward guidance commentary on customer acquisition rates.

Where this thesis breaks:

Implementation risk is real — the history of executive orders directing CBP enforcement upgrades is a history of partial follow-through. If the 90-to-180-day guidance memoranda from DHS land with softer penalty language than the EO text suggests, the DSGX and EXPD compliance tailwind compresses. If a federal court enjoins the IOR oversight framework on due-process grounds — not unlikely given the personal-liability language — the bonding and disclosure requirements stall. The wildcard is a negotiated trade deal that modifies the Section 301 tariff stack materially: a lower underlying duty rate reduces the misclassification incentive, which reduces the enforcement activity, which reduces the compliance TAM expansion. These are not base-case scenarios — in my view, CBP’s institutional posture and the administration’s stated commitment to enforcement make significant under-implementation unlikely — but they are the scenarios worth monitoring before sizing the trade.

What I’m watching:

CBP’s first implementation memorandum — expected July-August 2026 — for the specificity of penalty multiplier guidance and IOR high-risk list criteria; NCBFAA member alerts for early signals on broker fee repricing and entry-work-content expansion; any major retailer 8-K disclosing incremental compliance cost guidance, which would be the first market-visible signal of how large the importer cost stack actually shifts; the first UFLPA entity-list expansion under the new EO 14411 prioritization framework, which will signal how aggressively CBP is operationalizing the forced-labor lever; DSGX’s next earnings call for forward revenue-per-customer commentary and customer acquisition velocity post-EO; litigation filings by importer trade associations challenging the IOR personal-liability provisions; and the pace of FTZ and bonded warehouse utilization data from CBP’s monthly port statistics — the FTZ activation rate is the supply-chain community’s revealed preference on how seriously importers are taking EO 14411’s implementation risk.

The administration built the tariff schedule in 2025. EO 14411 builds the enforcement layer that makes the schedule real — and the compliance-services infrastructure that helps importers navigate that layer is sitting on a revenue expansion that has not yet been priced. The market is watching the tariff headlines. The structural trade is in the plumbing.

The Free Markets Report is provided by Lead-Lag Publishing, LLC for informational and educational purposes only and does not constitute investment, legal, accounting, or tax advice. Nothing herein is an offer to sell or a solicitation of an offer to buy any security. Specific securities mentioned are for illustration only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Readers should consult their own financial, legal, and tax advisors before making any investment decision. The author may hold positions in securities discussed.