Deregulation Meets Private Credit: How Looser Rules Could Fan the Flames of Non-Bank Lending

When Wall Street lenders descended on Miami Beach for the ABS East structured-finance conference, the mood was euphoric.

When Wall Street lenders descended on Miami Beach for the ABS East structured-finance conference, the mood was euphoric. Ballrooms and cabanas overflowed with dealmakers as private-credit managers negotiated loans late into the night¹. The boom in non-bank lending has become one of the defining financial stories of the decade—and deregulation may now pour even more fuel on the fire. The question is whether this fuel will keep the engine running or make it overheat.

Looser Rules and a Shifting Landscape

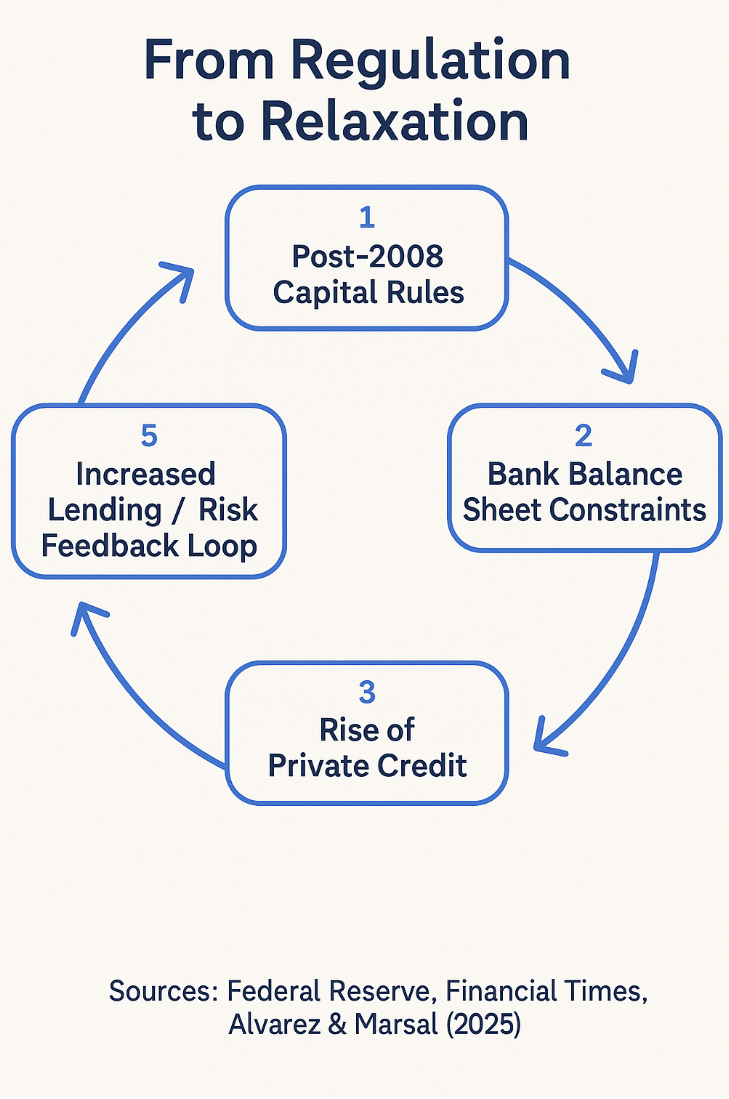

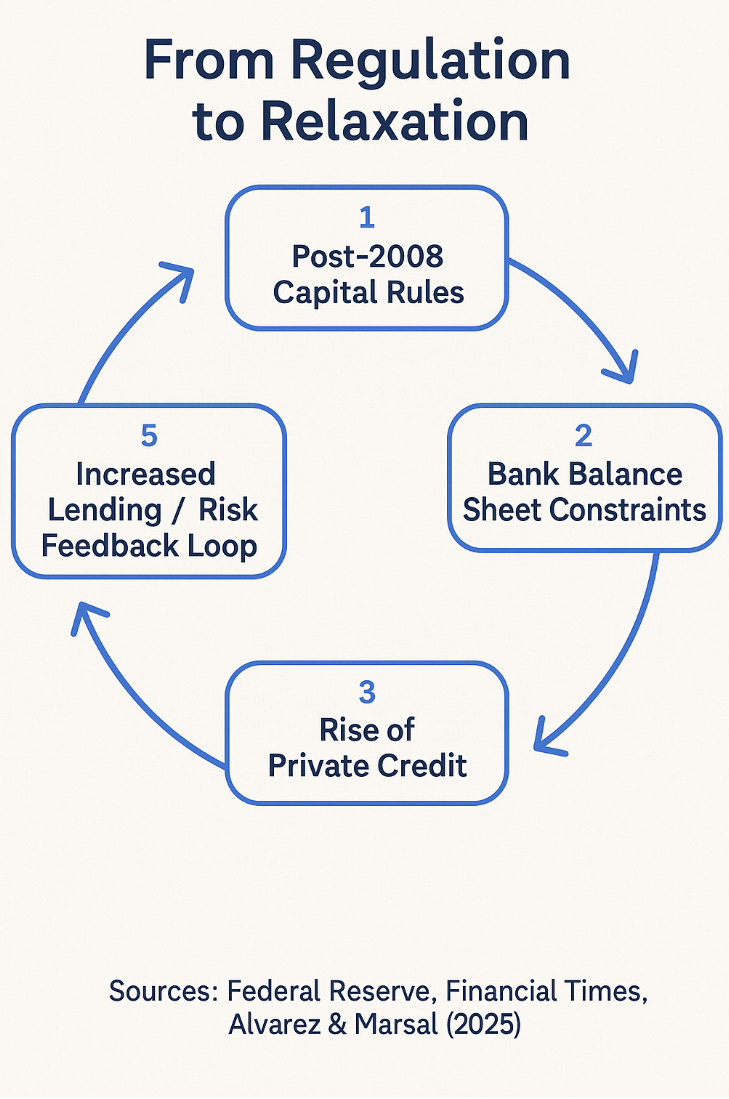

After more than a decade of tight post-crisis oversight, the regulatory pendulum is swinging back. In the United States, officials are easing capital and lending constraints on banks, potentially unlocking an estimated $2.6 trillion in additional lending capacity². Proponents say freeing that capital will stimulate growth—from infrastructure to technology—and help traditional banks compete with the private-credit funds that have eaten into their turf³.

Federal Reserve Vice Chair for Supervision Michelle Bowman has argued that excessive capital rules pushed lending into the shadows, discouraging banks from serving middle-market borrowers⁴. The hope is that lighter requirements will draw some activity back into the regulated sector.

Critics hear echoes of pre-2008 complacency. European Central Bank president Christine Lagarde has warned that dismantling post-crisis safeguards could jeopardize financial stability⁵. Bank of England governor Andrew Bailey likewise cautioned against a return to “slicing and dicing and tranching” debt structures reminiscent of the last credit bubble⁶. Deregulation may stimulate lending, but it also risks rekindling behaviors that end badly when confidence fades.

The divergence between jurisdictions sharpens the stakes. U.S. regulators are relaxing capital ratios and stress-testing rules⁷, while Europe remains cautious. Bailey fears policymakers may “throw out the baby with the bathwater” in the rush to ease constraints⁵. The result is a live experiment: will looser rules enhance competitiveness and growth—or ignite another cycle of excess?

The Bonfire of Private Credit

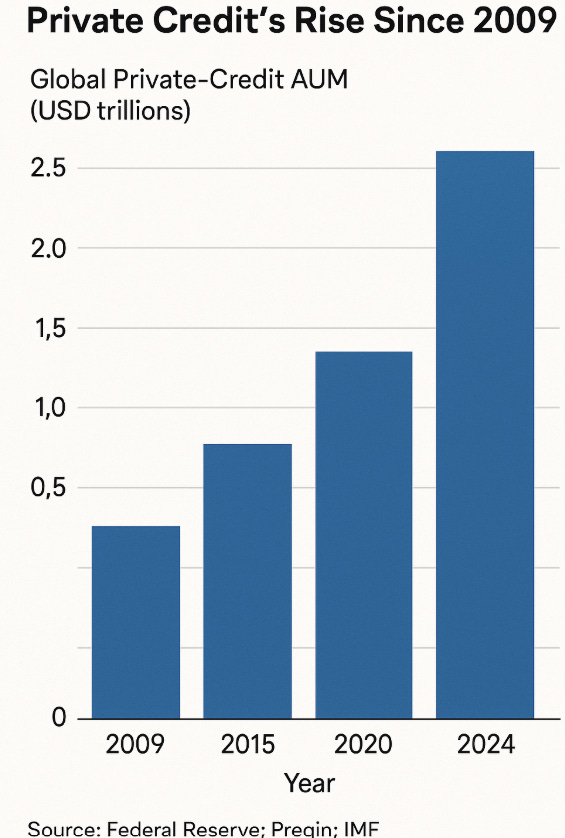

In the years after 2008, banks pulled back from riskier borrowers, leaving a void that private funds eagerly filled. What began as a niche now rivals parts of the banking system itself. By mid-2024, private credit had grown to roughly $1.3 trillion in the U.S. and nearly $2 trillion worldwide⁸—about five times its 2009 size. Yield-hungry investors and companies seeking flexible financing fueled the ascent.

Private loans appeal for their speed, customization, and discretion. To win business, lenders increasingly offered borrower-friendly “covenant-light” terms, stripping traditional protections. Houlihan Lokey data show such cov-lite deals surging as competition intensified⁹. Leverage also crept higher as funds stretched for returns. Many loans now reside inside collateralized-loan obligations or on the books of publicly traded Business Development Companies—keeping vast volumes of sub-investment-grade debt outside the banking perimeter.

This shadow ecosystem has benefited borrowers and private-equity sponsors, delivering equity-like returns with bond-like regularity. Yet history suggests such euphoria rarely lasts.

Cockroaches in the Shadows

When losses began surfacing in 2025, JPMorgan CEO Jamie Dimon sounded an ominous note. After two private-credit-backed failures—a subprime auto lender and a leveraged auto-parts maker—Dimon warned, “When you see one cockroach, there are probably more.”¹⁰ He cautioned that banks remain exposed through loans to private funds and shared borrowers¹¹.

Federal Reserve Chair Jerome Powell downplayed the systemic threat, saying he did “not see at this point a broader credit issue.”¹² Even so, regulators acknowledge opacity is a problem. Without disclosure requirements akin to public markets, no one knows how many more weak credits lurk beneath the surface. Bailey’s concern about “slicing and dicing” resonates here⁶. The International Monetary Fund recently estimated that banks hold roughly $4.5 trillion of indirect exposure to hedge funds, private-credit vehicles, and other non-bank intermediaries¹³—ample connective tissue for contagion.

The Bank of England has already launched a stress test of private-credit exposures¹⁴. Bailey asked whether the U.S. bankruptcies might be “the canary in the coal mine.” Some analysts note that in 2007, subprime risks were likewise dismissed as isolated. Today’s private-credit market is far larger, and its rapid deterioration, they warn, “should not be ignored.”¹⁵ The flames in non-bank lending are rising—and deregulation could fan them higher.

A Balancing Act for Investors

For investors, the intersection of deregulation and private credit is both promising and perilous. Easing rules may extend the cycle by spurring more lending and liquidity. Banks could regain share, financing mid-market firms more cheaply and supporting mergers and acquisitions. Non-bank lenders, often partners in syndicated deals, might also benefit from the broader credit expansion.

Yet exuberance carries a cost. Looser oversight can encourage the same leverage and leniency that magnify losses when growth slows. As banks edge into riskier territory—or channel funds to shadow lenders—the line between regulated and unregulated finance blurs. A setback in one corner could reverberate quickly through the rest. Investors enticed by private-credit yields must weigh illiquidity and opacity against potential reward. Rigorous due diligence on managers, structures, and covenants is essential when easy money flows freely.

Still, private credit itself is not inherently malign. It provides vital funding to businesses underserved by banks, and even regulators concede its value in diversifying credit supply¹⁶. The challenge lies in vigilance. While Powell’s tone remains calm, Federal Reserve researchers are actively mapping bank exposures and running stress simulations¹⁷. Complacency, not leverage alone, is what often turns a credit boom into a crisis.

Ultimately, the dance between deregulation and private credit demands careful choreography. Done right, easing rules could bring shadow lending into daylight without unleashing systemic risk. Done wrong, it may nurture the next generation of “cockroaches.” For investors, the takeaway is straightforward: high yields always carry hidden trade-offs. In a market where the lights are dimming, skepticism—and homework—remain the best defenses.

Footnotes

- Brooke Masters, “Deregulation Will Pour Extra Fuel on the Private Credit Bonfire,” Financial Times, October 2025.

- Martin Arnold, “Bank Deregulation Set to Unlock $2.6 Trillion of Wall Street Lending Capacity,” Financial Times, October 11, 2025.

- Ibid.

- Ibid.

- Andrew Bailey quoted in “Bank of England Chief Warns of ‘Worrying Echoes’ of 2008 Crisis,” The Guardian, October 21, 2025.

- Andrew Stanton, “U.S. Echoing ‘Alarm Bells’ of 2008 Crisis,” Newsweek, October 22, 2025.

- Ibid.

- José Berrospide et al., “Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications,” FEDS Notes, Board of Governors of the Federal Reserve System, May 23, 2025.

- Christopher Faille, “Houlihan Lokey: Borrowers Hold the Cards in Private Credit,” Private Debt Investor, August 19, 2025.

- Kalyeena Makortoff, “JP Morgan Boss Says More ‘Cockroaches’ Will Emerge After Private Credit Sector Failures,” The Guardian, October 14, 2025.

- Ibid.

- Jennifer Schonberger, “Fed’s Powell: No ‘Broader’ Credit Issue in Sight,” Yahoo Finance, October 2025.

- Financial Times, “Andrew Bailey Warns ‘Alarm Bells’ Ringing Over Private Credit Market,” October 2025.

- The Guardian, “Bank of England Chief Warns of ‘Worrying Echoes’ of 2008 Financial Crisis,” October 21, 2025.

- Newsweek, October 22, 2025.

- FEDS Notes, May 23, 2025.

- Ibid.

The Free Markets Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions, and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by The Free Markets Report are independent of other services provided by Lead-Lag Publishing, LLC, or its affiliates, and the positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors, and employees expressly disclaim all liability with respect to actions taken based on any or all of the information in this writing.